The U.S. Court of Appeals for the Fifth Circuit has granted a stay pending appeal of a recent district court order that preliminarily enjoined enforcement of the Corporate Transparency Act (CTA).[1]

The stay renders the district court’s order ineffective while the government appeals it. FinCEN responded the same day providing an extension of the reporting deadline for most reporting companies until January 13, 2025.[2] Therefore, the CTA is enforceable but with new timelines, more fully set out below. Please note that certain reporting deadlines were not explicitly extended, and in parsing FinCEN’s release it appears that the filing deadline for entities newly created or registered between September 24 and December 2, 2024 remains set at 90 days from such entity’s formation.

An update on case developments since our December 16, 2024 Client Alert can be found immediately below. For additional background information, please refer to the remainder of this Client Alert or our Client Alerts issued on December 5, December 9, and December 16, 2024.

On December 13, the Department of Justice, on behalf of the Financial Crimes Enforcement Network (FinCEN), filed a motion in the Fifth Circuit asking that court to stay the district court’s nationwide preliminary injunction against enforcement of the CTA, pending appeal of that order.[3]

On December 23, the Fifth Circuit granted the government’s request and stayed the district court’s order pending appeal.[4] The Fifth Circuit panel consisted of Judges Stewart, Haynes, and Higginson. Judge Haynes joined the order in part and disagreed in part, noting her agreement that a nationwide injunction was inappropriate but that she would deny the stay pending appeal with respect to the parties.[5]

The panel agreed with the government that it was likely to succeed on the merits of its appeal because, in its view, the CTA falls within the scope of Congress’s power under the Commerce Clause: The CTA “regulates anonymous ownership and operation of businesses”—”‘part of an economic class of activities that have a substantial effect on interstate commerce.’”[6] Moreover, the court credited the government’s argument that a facial challenge to the CTA was unlikely to succeed because the Act “at least operates constitutionally when it requires that corporations engaged in business operations affecting interstate commerce disclose their beneficial owner and applicant information.”[7]

Turning to the other factors that courts consider when evaluating stay requests, the panel concluded that the government demonstrated irreparable harm because it was enjoined from effectuating a statute enacted by Congress, and the equities weighed in favor of a stay because companies’ reporting costs would be minimal compared to the government’s interest in combatting financial crime and protecting national security.[8] It also noted that although the injunction would be lifted shortly before the January 1, 2025 reporting deadline, businesses have had nearly four years since the CTA’s enactment and one year since FinCEN announced the reporting deadline to prepare.[9]

Late on December 23, 2024, FinCEN announced that it “recognizes that reporting companies may need additional time to comply given the period when the preliminary injunction had been in effect” and so has extended the reporting deadlines for most companies to January 13, 2025.

Additionally, on December 24, 2024, the plaintiffs filed an emergency petition for rehearing en banc, which is currently pending.[10] The plaintiffs are asking the en banc Fifth Circuit to act on that petition by January 6, 2024, and the plaintiffs indicated that they may also seek relief in the U.S. Supreme Court prior to January 13, 2024.[11]

What the Stay Means for Entities Subject to the CTA

Now that the district court’s order has been stayed, the CTA and FinCEN’s beneficial ownership information (BOI) Reporting Rule are enforceable again. Based on FinCEN’s reporting extensions on December 23, the following are the operative Reporting Rule deadlines for non-exempt reporting companies as noted in the FinCEN announcement[12]:

|

Category |

New Reporting Deadline |

Original Reporting Deadline |

|

Entities created or registered prior to 2024 |

January 13, 2025 |

January 1, 2025 |

|

Entities created or registered between January 1 and September 3, 2024 |

The original 90-day reporting deadline for these entities had already passed as of the district court’s December 3, 2024 stay order. FinCEN did not extend the original reporting deadline for these entities. |

|

|

Entities created or registered between September 4 and 24, 2024 (referred to by FinCEN as entities created or registered “on or after September 4, 2024 that had a filing deadline between December 3, 2024 and December 23, 2024”) |

January 13, 2025 |

90 days from creation or registration |

|

Entities created or registered between September 24 and December 2, 2024[13] |

90 days from creation or registration (no extension provided) |

90 days from creation or registration |

|

Entities created or registered between December 3 and 23, 2024 |

21 days after the original reporting deadline |

90 days from creation or registration |

|

Entities created or registered between December 24 and 31, 2024 |

90 days from creation or registration (no extension provided) |

90 days from creation or registration |

|

Entities created or registered on or after January 1, 2025 |

30 days from creation or registration (no extension provided) |

30 days from creation or registration |

|

Entities that qualify for disaster relief extensions |

For any entity that qualifies for a disaster relief extension, FinCEN has provided that the later of January 13, 2025 and the original reporting deadline (as extended pursuant to disaster relief) will apply. |

|

blank space

Entities that believe they may be subject to the Reporting Rule should closely monitor this matter, and consult with their CTA advisors as necessary, to understand their obligations under the CTA and the Reporting Rule under the new reporting deadlines set out above.

Additional Background

The CTA, enacted in 2021, requires corporations, limited liability companies, and certain other entities created (or, as to non-U.S. entities, registered to do business) in any U.S. state or tribal jurisdiction to file a “BOI” report with FinCEN identifying, among other information, the natural persons who are beneficial owners of the entity.[14] A regulation, the Reporting Rule, helps implement the CTA by specifying compliance deadlines—including the original January 1, 2025 deadline for companies created or registered to do business in the United States before January 1, 2024—and detailing what information must be reported to FinCEN.[15]

The December 3, 2024 Ruling

On December 3, 2024, in ruling on a lawsuit challenging the constitutionality of the CTA and Reporting Rule on various grounds, Judge Amos L. Mazzant of the U.S. District Court for the Eastern District of Texas granted plaintiffs’ motion for a preliminary injunction.[16] Unlike another court that had held the CTA unconstitutional,[17] Judge Mazzant preliminarily enjoined enforcement of the CTA and Reporting Rule nationwide.[18] Moreover, the court invoked its power under the Administrative Procedure Act’s stay provision, 5 U.S.C. § 705, to “postpone the effective date of” the Reporting Rule.[19]

Government’s Initial Response[20]

On December 5, the Department of Justice, on behalf of the Department of the Treasury, filed a notice of appeal from the court’s opinion and order to the U.S. Court of Appeals for the Fifth Circuit.[21]

FinCEN also posted a statement to its website.[22] In sum, FinCEN noted that, because of the court’s order, “reporting companies are not currently required to file their beneficial ownership information with FinCEN and will not be subject to liability if they fail to do so while the preliminary injunction remains in effect. Nevertheless, reporting companies may continue to voluntarily submit beneficial ownership information reports.” FinCEN also noted the appeal filed by the Department of Justice.

[1] A prior alert by Gibson Dunn explaining the district court’s ruling is available at https://www.gibsondunn.com/corporate-transparency-act-enforcement-preliminarily-enjoined-nationwide. See Texas Top Cop Shop, Inc. et al. v. Garland et al., No. 4:24-CV-478, Dkt. 30 (E.D. Tex. Dec. 3, 2024).

[2] https://www.fincen.gov/boi.

[3] Texas Top Cop Shop, Inc. v. Garland, No. 24-40792, Dkt. 21 (5th Cir. Dec. 13, 2024).

[4] Texas Top Cop Shop, Inc. v. Garland, No. 24-40792, Dkt. 140-2 (5th Cir. Dec. 23, 2024).

[5] Id. at 2 n.1.

[6] Id. at 3 (quoting Gonzales v. Raich, 545 U.S. 1, 17 (2005)).

[7] Id. at 5.

[8] Id. at 5–7.

[9] Id. at 7 n.7.

[10] Texas Top Cop Shop, Inc. v. Garland, No. 24-40792, Dkt. 143 (5th Cir. Dec. 24, 2024).

[11] Texas Top Cop Shop, Inc. v. Garland, No. 24-40792, Dkt. 142 (5th Cir. Dec. 24, 2024).

[12] https://www.fincen.gov/boi.

[13] FinCEN’s notice did not expressly address or provide an extension for entities created or registered between these dates.

[14] See William M. (Mac) Thornberry National Defense Authorization Act for Fiscal Year 2021, Pub. L. 116-283, Div. F., § 6403 (adding 31 U.S.C. § 5336). Prior alerts by Gibson Dunn explaining the Corporate Transparency Act are available at: https://www.gibsondunn.com/top-12-developments-in-anti-money-laundering-enforcement-in-2023; https://www.gibsondunn.com/the-impact-of-fincens-beneficial-ownership-regulation-on-investment-funds; https://www.gibsondunn.com/the-corporate-transparency-act-reminders-and-key-updates-including-fincen-october-3-faqs.

[15] 31 C.F.R. § 1010.380.

[16] Texas Top Cop Shop, Inc. et al. v. Garland et al., No. 4:24-CV-478, Dkt. 30 (E.D. Tex. Dec. 3, 2024).

[17] Nat’l Small Business United v. Yellen, 721 F. Supp. 3d 1260 (N.D. Ala. 2024); see https://www.gibsondunn.com/corporate-transparency-act-declared-unconstitutional-what-it-means-for-you.

[18] Id. at 77.

[19] Id. at 78.

[20] See Gibson Dunn’s December 9 Client Alert describing the government’s initial response to the district court ruling, available at https://www.gibsondunn.com/us-government-appeals-and-fincen-issues-guidance-about-nationwide-preliminary-injunction-of-corporate-transparency-act-enforcement.

[21] Texas Top Cop Shop, Inc. et al. v. Garland et al., No. 4:24-CV-478, Dkts. 32, 34 (E.D. Tex. Dec. 6, 2024).

Gibson Dunn has deep experience with issues relating to the Bank Secrecy Act, the Corporate Transparency Act, other AML and sanctions laws and regulations, and challenges to Congressional statutes and administrative regulations.

For assistance navigating white collar or regulatory enforcement issues, please contact the authors, the Gibson Dunn lawyer with whom you usually work, or any leader or member of the firm’s Anti-Money Laundering, Administrative Law & Regulatory, Investment Funds, Real Estate, or White Collar Defense & Investigations practice groups.

Please also feel free to contact any of the following practice group leaders and members and key CTA contacts:

Anti-Money Laundering:

Stephanie Brooker – Washington, D.C. (+1 202.887.3502, [email protected])

M. Kendall Day – Washington, D.C. (+1 202.955.8220, [email protected])

David Ware – Washington, D.C. (+1 202-887-3652, [email protected])

Ella Capone – Washington, D.C. (+1 202.887.3511, [email protected])

Sam Raymond – New York (+1 212.351.2499, [email protected])

Chris Jones – Los Angeles (+1 213.229.7786, [email protected])

Administrative Law and Regulatory:

Stuart F. Delery – Washington, D.C. (+1 202.955.8515, [email protected])

Eugene Scalia – Washington, D.C. (+1 202.955.8673, [email protected])

Helgi C. Walker – Washington, D.C. (+1 202.887.3599, [email protected])

Matt Gregory – Washington, D.C. (+1 202.887.3635, [email protected])

Investment Funds:

Kevin Bettsteller – Los Angeles (+1 310.552.8566, [email protected])

Shannon Errico – New York (+1 212.351.2448, [email protected])

Greg Merz – Washington, D.C. (+1 202.887.3637, [email protected])

Real Estate:

Eric M. Feuerstein – New York (+1 212.351.2323, [email protected])

Jesse Sharf – Los Angeles (+1 310.552.8512, [email protected])

Lesley V. Davis – Orange County (+1 949.451.3848, [email protected])

Anna Korbakis – Orange County (+1 949.451.3808, [email protected])

White Collar Defense and Investigations:

Stephanie Brooker – Washington, D.C. (+1 202.887.3502, [email protected])

Winston Y. Chan – San Francisco (+1 415.393.8362, [email protected])

Nicola T. Hanna – Los Angeles (+1 213.229.7269, [email protected])

F. Joseph Warin – Washington, D.C. (+1 202.887.3609, [email protected])

© 2024 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

From the Derivatives Practice Group: The CFTC approved a final rule regarding safeguarding and investment of customer funds by FCMs and DCOs and another final rule codifying the no-action position in CFTC staff letter 19-17 regarding separate account treatment by FCMs. The CFTC also has suggestions on your New Year’s resolution.

New Developments

- Customer Advisory: Avoiding Fraud May be Your Best Resolution. A new CFTC customer advisory suggests adding “spotting scams” to your list of New Year’s resolutions. The Office of Customer Education and Outreach’s Avoiding Fraud May be Your Best Resolution says that with scammers robbing billions of dollars from Americans through relationship investment scams, resolving to be careful about who you trust online, staying informed, and learning all you can about trading risks are admirable 2025 resolutions. [NEW]

- CFTC Approves Final Rule on Margin Adequacy, Treatment of Separate Accounts of a Customer by Futures Commission Merchants. On December 20, 2024, the CFTC announced a final rule to implement requirements for futures commission merchants related to margin adequacy and the treatment of separate accounts of a customer. The rule finalizes the Commission’s proposal, published in the Federal Register in March, to codify the no-action position in CFTC staff letter 19-17 regarding separate account treatment. [NEW]

- CFTC Approves Final Rule Regarding Safeguarding and Investment of Customer Funds. On December 17, the CFTC announced that it approved a final rule amending the CFTC’s regulations that govern how futures commission merchants and derivatives clearing organizations safeguard and invest customer funds held for the benefit of customers engaging in futures, foreign futures, and cleared swaps transactions. The amendments revise the list of permitted investments in CFTC Regulation 1.25 and make other related changes and specifications. The amendments also eliminate the CFTC requirement that an FCM deposit customer funds with depositories that provide the CFTC with read-only electronic access to such accounts. The compliance date for the revisions is 30 days after the final rule is published in the Federal Register, except for the revisions to the Segregation Investment Detail Reports (“SIDR”) specified in CFTC Regulations 1.32, 22.2(g)(5), and 30.7(l)(5), and the revisions to the customer risk disclosure statement required under CFTC Regulation 1.55. The compliance date for the revisions to the SIDR and the risk disclosure statement is March 31, 2025. [NEW]

- CFTC Commissioner Kristin N. Johnson Announces Reports and Recommendations Advanced by MRAC in 2024. The Market Risk Advisory Committee (“MRAC”) held a public meeting Dec. 10 during which the MRAC adopted three sets of recommendations for the CFTC’s consideration. The reports and accompanying recommendations address (i) U.S. Treasury markets with a focus on effective risk management practices for the cash-futures basis trade, (ii) modernization of regulation governing cyber resilience and critical third-party service providers for central counterparties, and (iii) the potential benefits and limitations of formally adopting obligations to employ legal entity identifiers for beneficial account holders of certain intermediaries. Commissioner Johnson also announced that Danielle Abada, Christopher Lamb and Nita Somasundaram have joined her staff [NEW]

- CFTC Grants QC Clearing LLC DCO Registration. On December 17, 2024, the CFTC announced that it issued QC Clearing LLC an Order of Registration as a derivatives clearing organization under the Commodity Exchange Act. QC Clearing LLC permitted to clear, in its capacity as a DCO, fully collateralized positions in futures contracts, options on futures contracts, and swaps. [NEW]

- CFTC Staff Issues Advisory Regarding Form 304 Submission Format Beginning January 15, 2025. On December 12, the CFTC Division of Market Oversight issued an advisory notifying all merchants and dealers of cotton holding or controlling positions for future delivery in cotton (traders) that beginning next year they must submit the regulatory filing identified as “Form 304” through the CFTC’s online filings portal. The advisory notes that all traders who are subject to CFTC Regulation 17 CFR 19.00(a) beginning January 15, 2025, Form 304 must be submitted through the CFTC’s online filings portal, which has been updated for traders’ use. Form 304 should continue to be submitted via email through January 14, 2025.

- CFTC Staff Issues Advisory Related to the Use of Artificial Intelligence by CFTC-Registered Entities and Registrants. On December 5, the CFTC’s Divisions of Clearing and Risk, Data, Market Oversight, and Market Participants issued a staff advisory on the use of artificial intelligence in CFTC-regulated markets by registered entities and registrants. The advisory is intended to remind CFTC-regulated entities of their obligations under the Commodity Exchange Act and the CFTC’s regulations as these entities begin to implement AI. CFTC staff noted that it is closely tracking the development of AI technology and AI’s potential benefits and risks and that it values its ongoing dialogue with CFTC-regulated entities and intends to monitor these entities’ use of AI as part of the agency’s routine oversight activities. According to the CFTC, the advisory is informed, in part, by public comments received in response to the staff’s January 25, 2024 Request for Comment on AI.

- CFTC Releases FY 2024 Enforcement Results. On December 4, the CFTC announced record monetary relief of over $17.1 billion for fiscal year 2024. With the resolution of digital asset cases that resulted in the agency’s largest recovery ever, this record amount included $2.6 billion in civil monetary penalties and $14.5 billion in disgorgement and restitution. In FY 2024, the agency brought 58 new actions including, in the CFTC’s words, precedent-setting digital asset commodities cases, its first actions addressing fraud in voluntary carbon credit markets, complex manipulation cases in various markets, and significant compliance cases – including its largest compliance case ever. The CFTC also said that it continued to vigorously litigate pending actions, resulting in significant litigation victories and recoveries.

New Developments Outside the U.S.

- ESMA Consults on the Internal Control Framework for Some of its Supervised Entities. On December 19, ESMA launched a consultation on draft Guidelines related to the Internal Control Framework for some of its supervised entities. ESMA said that the proposed draft Guidelines build on the Internal Control Guidelines currently in place for Credit Rating Agencies and extend them to include also Benchmark Administrators, and Market Transparency Infrastructures (Trade Repositories, Data Reporting Services Providers and Securitization Repositories). The draft Guidelines outline ESMA’s expectations for the components and characteristics of an effective internal control system, intended to ensure: a strong framework, detailing the internal control environment and informational aspects, and effective internal control functions, including compliance, risk management, and internal audit. The draft Guidelines also explain how ESMA applies proportionality in its expectations regarding the internal controls for a supervised entity. According to ESMA, the consultation is primarily aimed at ESMA supervised entities and prospective applicants for ESMA supervision. [NEW]

- ESMA Releases Last Policy Documents to Get Ready for MiCA. On December 17, ESMA published its last package of final reports containing Regulatory Technical Standards and guidelines ahead of the full entry into application of the Markets in Crypto Assets Regulation. Specifically, the package includes Regulatory Technical Standards on market abuse and guidelines on reverse solicitation, suitability, crypto-asset transfer services, qualification of crypto-assets as financial instruments and maintenance of systems and security access protocols. [NEW]

- ESMA Consults on Proposals to Digitalize Sustainability and Financial Disclosures. On December 13, ESMA published a Consultation Paper seeking stakeholders’ views on how the European Single Electronic Format can be applied to sustainability reporting. The proposals also aim to ease the burden associated with financial reporting. Interested stakeholders are invited to submit their feedback by March 31, 2025.

- ESMA Consults on Open-Ended Loan Originating Alternative Investment Funds. On December 12, ESMA published a consultation paper on draft regulatory technical standards on open-ended loan originating Alternative Investment Funds (“AIFs”) under the revised Alternative Investment Fund Managers Directive (“AIFMD”). AIFMD review has introduced some harmonized rules on loan originating funds. The goal of these rules is to provide a common implementing framework by determining the elements and factors that Alternative Investment Fund Managers need to consider when making the demonstration to their Competent Authorities that the loan originated AIFs they manage can be open-ended.

- ESMA Consults on Technical Advice on Listing Act Implications. On December 12, ESMA launched a consultation to gather feedback following changes to the Market Abuse Regulation (“MAR”) and Market in Financial Instruments Directive II (“MiFID II”) introduced by the Listing Act. Regarding MAR, ESMA is inviting feedback on: a non-exhaustive list of the protracted process and the relevant moment of disclosure of the relevant inside information (together with some principles to identify the moment of disclosure for protracted not listed processes); a non-exhaustive list of examples where there is a contrast between the inside information to be delayed and the latest public announcement by the issuer; and a methodology and preliminary results for identifying trading venues with a significant cross-border dimension, for the purposes of establishing a Cross Market Order Book Mechanism. Regarding MiFID II, ESMA’s proposals cover: a systematic review of the relevant provisions in Commission Delegated Regulation 2017/565 to ensure that a Multilateral Trading Facility (“MTF”) (or a segment of it) to be registered as small and medium-sized enterprises growth market complies with the relevant requirements in the revised MiFID II; and some conditions to meet the registration requirements for a segment of an MTF, as specified in the revised MiFID II.

- ESAs Provide Guidelines to Facilitate Consistency in the Regulatory Classification of Crypto-Assets by Industry and Supervisors. On December 10, the European Supervisory Authorities (the “ESAs”) published joint Guidelines intended to facilitate consistency in the regulatory classification of crypto-assets under Markets in Crypto Asset Regulation. The Guidelines include a standardized test to promote a common approach to classification as well as templates market participants should use when communicating to supervisors the regulatory classification of a crypto-asset.

- IOSCO Publishes Final Report on Regulatory Implications and Good Practices on the Evolution of Market Structures. On November 29, IOSCO published its Final Report on the Evolution in the Operation, Governance, and Business Models of Exchanges. According to IOSCO, the Final Report addresses significant changes in exchange business models and market structures, highlighting the impact of increased competition, technological advancements, and cross-border activity on exchanges. Additionally, it outlines a set of six good practices for regulators to consider in the supervision of exchanges that cover three key areas: (1) Organization of Exchanges and Exchange Groups (2) Supervision of Exchanges and Trading Venues within Exchange Groups and (3) Supervision of Multinational Exchange Groups.

New Industry-Led Developments

- FRTB Implementation Challenges: Capitalization of Funds. On December 13, ISDA published a second whitepaper on the capitalization of equity investment in funds (“EIIFs”) under the Fundamental Review of the Trading Book (“FRTB”) framework. This paper builds upon an earlier ISDA publication in 2022 that highlighted the overly conservative capital requirements and operational complexities resulting from the proposed Basel III framework associated with EIIFs. Since then, several jurisdictions have implemented the FRTB (Canada and Japan), while others have finalized their FRTB rules (the EU and the UK) or are consulting on the final rules (the US). This topic continues to be a globally important issue for the industry, with many unresolved concerns related to the treatment of EIIFs.

- ISDA Responds to HM Treasury on Financial Services Growth and Competitiveness Strategy. On December 12, ISDA submitted its response to HM Treasury’s call for evidence on its financial services growth and competitiveness strategy. In the response, ISDA focused on innovation, technology, international partnerships and trade and sustainable finance. ISDA also urged the UK government to progress its review of markets and infrastructure regulation and retain its focus as a world leading host for central counterparties. [NEW]

- Joint Associations Send Letter on UK CCP Equivalence and Recognition. On December 12, ISDA and eleven other trade associations representing a broad group of market participants sent a letter to Commissioner Albuquerque requiring that the European Commission extends the equivalence decision for UK Central Counterparties in a non-time-limited manner and well in advance of March 31, 2025. The current time-limited equivalence decision is set to expire on June 30, 2025.

- ISDA Publishes Paper on Compliance Requirements under MIFIR. On December 9, ISDA published a paper that maps out an approach to post-trade transparency under the revised Markets in Financial Instruments Regulation for reporting single-name credit default swaps referenced to global systemically important banks, supporting meaningful transparency and implementation practicability.

The following Gibson Dunn attorneys assisted in preparing this update: Jeffrey Steiner, Adam Lapidus, Marc Aaron Takagaki, Hayden McGovern, and Karin Thrasher.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s Derivatives practice group, or the following practice leaders and authors:

Jeffrey L. Steiner, Washington, D.C. (202.887.3632, [email protected])

Michael D. Bopp, Washington, D.C. (202.955.8256, [email protected])

Michelle M. Kirschner, London (+44 (0)20 7071.4212, [email protected])

Darius Mehraban, New York (212.351.2428, [email protected])

Jason J. Cabral, New York (212.351.6267, [email protected])

Adam Lapidus – New York (212.351.3869, [email protected] )

Stephanie L. Brooker, Washington, D.C. (202.887.3502, [email protected])

William R. Hallatt , Hong Kong (+852 2214 3836, [email protected] )

David P. Burns, Washington, D.C. (202.887.3786, [email protected])

Marc Aaron Takagaki , New York (212.351.4028, [email protected] )

Hayden K. McGovern, Dallas (214.698.3142, [email protected])

Karin Thrasher, Washington, D.C. (202.887.3712, [email protected])

© 2024 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

An annual update of observations on new developments and highlights of considerations for calendar-year filers preparing their Annual Reports on Form 10-K for 2024 and proxy statements for annual meetings in 2025.

Each year we offer our observations on new developments and highlight select considerations for calendar-year filers as they prepare their Annual Reports on Form 10-K. This year, we are also including a discussion of select proxy statement considerations. This alert touches upon recent rulemaking from the U.S. Securities and Exchange Commission (the “SEC” or “Commission”), emerging trends among reporting companies, recent comment letters issued by the staff of the SEC’s Division of Corporation Finance (the “Staff”) and developments in the securities litigation and SEC enforcement landscape.

Despite the forthcoming changes in presidential administration and Commission leadership, public companies continue to be subject to rules adopted and guidance issued during Gary Gensler’s chairmanship. While we anticipate that changes in Commission leadership will likely result in shifts in the SEC’s disclosure review focus and enforcement priorities, we believe public companies are wise to stay the course and react to changes in policy or practice with respect to SEC and investor disclosures only after such changes are implemented.

An index of the topics described in this alert is provided below.

I. New Disclosure Requirements for 2024 Form 10-Ks and 2025 Proxy Statements

A. New Form 10-K Disclosure Requirements

1. Discuss Insider Trading Policies and Procedures in the Form 10-K (and Proxy

Statement)

2. File Insider Trading Policies and Procedures with the Form 10-K

3. iXBRL Tagging for Cybersecurity Disclosures

B. New Proxy Statement Disclosure Requirements

1. Option Award Grant Timing Disclosures

2. Discuss Insider Trading Policies and Procedures in the Proxy Statement (and

Form 10-K)

II. Disclosure Trends and Considerations for the 2024 Form 10-K

A. Cybersecurity

B. Human Capital

C. Climate Change and ESG

D. Generative Artificial Intelligence

E. Geopolitical Conflict

F. Issues for China-based Companies

G. Inflation and Interest Rate Concerns

III. Disclosure Trends and Considerations for the 2025 Proxy Statement

A. Officer Exculpation

B. Director Time Commitments (Overboarding)

C. Director Independence Determinations

D. Pay vs. Performance

E. Continued SEC Scrutiny of Perquisites

F. Nasdaq Board Diversity Rules

IV. SEC Comment Letter Trends

A. Management’s Discussion and Analysis

B. Non-GAAP Financial Measures

C. Segment Reporting

V. Securities Litigation

VI. SEC Enforcement

A. Defense Against Cybersecurity Risks

B. Use of Emerging Technologies

C. Internal Controls

D. Enforcement Priorities in 2025

VII. Other Reminders and Considerations

A. EDGAR Next

B. Disclosure of Significant Segment Expenses in Notes to Financials

C. Clawback Policies and Checkboxes

D. Filing Requirement for “Glossy” Annual Report

E. Cover Page XBRL Disclosures

VIII. Looking Forward

I. New Disclosure Requirements for 2024 Form 10-Ks and 2025 Proxy Statements

The pace of SEC rulemaking regarding public company disclosures slowed in 2024 compared to prior years, particularly the period of breakneck rulemaking that began when Chair Gensler became the Chair of the Commission in 2021 and continued through the end of 2023. The main disclosure requirements that became effective in 2024 resulted from final rules adopted by the SEC in December 2022.

While the SEC’s Regulatory Flexibility Agendas for Spring and Fall 2024 continued to include a bevy of new rulemaking projects, only a few impacting the disclosure obligations of public companies made it to the proposed or final rule stage. When the Trump-appointed Chair, currently expected to be former SEC Commissioner Paul Atkins, takes over at the SEC, several of the rulemaking projects that currently remain under consideration (e.g., board diversity, human capital) are likely to be relegated to the back burner or abandoned altogether.

Set forth below are discussions of the most significant new disclosure requirements that public companies need to consider heading into 2025.

1. Discuss Insider Trading Policies and Procedures in the Form 10-K (and Proxy Statement)

Pursuant to Item 408(b) of Regulation S-K, companies with a December 31 fiscal year end will be required to disclose whether they have adopted insider trading policies and procedures governing the purchase, sale, and other dispositions of their securities by directors, officers, and employees, or the company itself, that are reasonably designed to promote compliance with insider trading laws, rules, and regulations, and any listing standards applicable to the company. If a company has not adopted such insider trading policies and procedures, it must explain why it has not done so.

Form 10-K vs. Proxy Statement

The information required by Item 408(b) must be included in Part III, Item 10 of Form 10-K[1] every year (either directly or by forward incorporation by reference to the proxy statement) and in the proxy statement for any meeting involving the election of directors.

Because companies are permitted to forward incorporate Form 10-K Part III information by reference to a proxy statement filed within 120 days of the end of the year covered by the Form 10-K, companies may decide to simply include the disclosure in the proxy statement as is commonly done with other Part III information. Companies that decide to go this route should make sure that the insider trading disclosure in the proxy statement is adequately covered by the incorporation by reference language included in Item 10 of Form 10-K. To comply with Exchange Act Rule 12b-23, companies should identify in the Form 10-K the information intended to be incorporated as well as the section of the proxy statement in which that information can be found.

Based on a review of the 95 S&P 500 companies that had filed an insider trading policy as of November 22, 2024, we compiled several observations that are set forth in this alert. For information about the results of an earlier survey based on our review of the insider trading policies filed by S&P 500 companies as of June 30, 2024, see our client alert “Early Insights from Insider Trading Policies Filed by S&P 500 Companies under the SEC’s New Exhibit Requirement“ (the “September 2024 Insider Trading Policy Survey”).[2]

Out of the above-mentioned 95 companies, 56 have filed both their proxy statement and their Form 10-K.[3] Of these 56 companies, 95% included the disclosure in their proxy statement, with 57% including the disclosure only in the proxy statement (and incorporating by reference in the Form 10-K); 32% including the disclosure in the proxy statement and Form 10-K; and 9% having a deficient Form 10-K because they did not include or incorporate by reference the disclosure. The remaining 5% of the 56 companies had a deficient proxy statement because they included the disclosure only in the Form 10-K.

Content of Item 408(b) Disclosure

Companies seem to take varying approaches to the content of their Item 408(b) disclosure. While some of the companies that included the disclosure in both the Form 10-K and the proxy statement had the same or virtually the same disclosure in both filings, others varied it, with some companies largely tracking the language provided in Item 408(b) in the Form 10-K, referring readers to the policies and procedures filed as exhibits to the Form 10-K, but providing more detailed disclosure in their proxy statement, and other companies including more detailed disclosure in the Form 10-K than the proxy statement. A majority of the companies that included the disclosure only in the proxy statement included more detailed disclosure than the language provided in Item 408(b), in many cases by including the key terms of the policy and weaving into the discussion the hedging policy disclosure required by Item 407(i).

“Policies and procedures governing … the registrant itself”

As mentioned above, Item 408(b) requires a company to disclose whether it has adopted insider trading policies and procedures governing transactions in company securities by the company itself, and, if so, to file the policies and procedures, or, if not, to explain why.

Of the 95 S&P 500 companies that had filed their insider trading policy as of November 22, 2024, a majority (69%) did not address insider trading policies or procedures governing companies’ transactions in their own securities.[4] Twenty-six percent of the surveyed companies addressed this requirement by including in their primary insider trading policy a brief sentence or two about the company’s policy of complying with applicable laws when trading in its own securities. Four percent of the surveyed companies filed a separate company repurchase policy, either as a separate exhibit (3%) or with the company’s primary insider trading policy as a single exhibit (1%).

Comparing these findings to the results of our survey of insider trading policies as of June 30, 2024 shows that more companies are complying with the requirement to file policies applicable to company transactions. In fact, almost half of the companies that filed their insider trading policy exhibits after August 30, 2024 complied with the requirement, as compared with 22% of companies that had filed as of June 30, 2024.

2. File Insider Trading Policies and Procedures with the Form 10-K

Pursuant to the exhibit requirements in Item 601(b)(19) of Regulation S-K and the new insider trading rule in Item 408(b)(2), calendar year-end companies are required to file with their 2024 Form 10-K “[a]ny” “insider trading policies and procedures governing the purchase, sale, and/or other dispositions of the registrant’s securities by directors, officers and employees, or the registrant itself, that are reasonably designed to promote compliance with insider trading laws, rules and regulations, and any listing standards applicable to the registrant.”

In September 2024, we published our September 2024 Insider Trading Policy Survey. The discussion below covers some of the questions raised by the new exhibit requirement and looks at how some filers handled these issues.

Ancillary Materials to Primary Insider Trading Policy

For many companies, there is not simply one document setting forth every policy applicable to directors, officers and employees that is “reasonably designed to promote compliance with insider trading laws, rules and regulations, and [applicable] listing standards.” A company’s primary insider trading policy is frequently accompanied by:

- appendices or other ancillary documents setting forth additional details, such as a schedule listing the people subject to additional trading windows or preclearance procedures, additional guidelines applicable to Rule 10b5-1 trading arrangements, or frequently asked questions;

- training materials used to promote compliance with insider trading laws, rules, regulations, and listing standards by directors, officers, and employees; and/or

- specific instructions for how directors, officers, and employees can obtain preclearance or any other approvals referenced in the policy (e.g., who to contact, what systems to use).

Similarly, for the convenience of its users, historically some policies hyperlinked to other information relevant to the policy, such as applicable definitions, examples of what constitutes material non-public information (“MNPI”), and a routinely updated schedule of quarterly trading blackout windows.

When preparing to file Exhibit 19 to Form 10-K, companies will want to consider whether any of these ancillary materials should be filed with the company’s primary insider trading policy. In the absence of guidance from the SEC, one reasonable approach would be to file any ancillary materials that impose additional substantive requirements on directors, officers, and employees, but omit ancillary materials that simply repeat or provide examples or interpretations of the requirements set forth in the main policy.

Based on the insider trading policies filed as of November 22, 2024, a significant majority (86%) of the companies filed only a single insider trading policy and no other related policies or documents (even where the insider trading policy referenced other related policies).[5] In the small number of cases where multiple policies were filed, the additional policies were often supplemental guidelines or policies covering topics typically not applicable to all employees at larger companies (e.g., trading windows, preclearance procedures, 10b5-1 plans).

Unwritten Procedures

Item 408(b)(2) seems to presume the policies and procedures are in writing, but nowhere has the SEC addressed what is to be done to comply with the exhibit requirement in Item 601(b)(19) if the policy or, more likely, procedures are not written. In the absence of guidance from the SEC, to the extent companies have policies or procedures that are not written, they will need to decide whether to (1) memorialize their previously unwritten policies or procedures in writing (either through a detailed description or a more high-level summary) so they can be filed or (2) leave the policies or procedures unwritten and forego filing.

Personal Information in Policies

Many insider trading policies have historically included the names and contact information for the individuals responsible for administering the policy. In anticipation of the filing requirement, many companies have removed that information from the policy altogether. We also believe it is reasonable to retain the information in the internal, non-public facing policy but to redact the information from the exhibit filed with the Form 10-K pursuant to Item 601(a)(6), which allows companies to redact information “if disclosure of such information would constitute a clearly unwarranted invasion of personal privacy (e.g., disclosure of bank account numbers, social security numbers, home addresses, and similar information).”

Beginning with the 2024 Form 10-K, the required cybersecurity disclosures that calendar year-end companies first began including in their 2023 Forms 10-K pursuant to Item 106 of Regulation S-K will need to be tagged in Inline XBRL (“iXBRL”), including by block text tagging narrative disclosures and detail tagging quantitative amounts.[6] The SEC has stated that companies must use the “Cybersecurity Disclosure (CYD)” taxonomy tags within iXBRL to tag these disclosures.[7] Companies need to be aware that significant judgment will be required to apply these tags. Not only will companies be required to determine the provision of Item 106 to which each part of the narrative disclosure is responsive, but companies will also need to determine which flags to mark as “true” or “false.”

Importantly, under the CYD taxonomy, there is a flag for “Cybersecurity Risk Materially Affected or Reasonably Likely to Materially Affect Registrant,” and it is our understanding that to properly apply the flag, each company must select “true” or “false.” As discussed in Section II.A. (Cybersecurity) below, the requirement to describe whether any risks from cybersecurity threats have materially affected or are reasonably likely to materially affect the registrant caused consternation among many companies and resulted in wide variety of responses during the first year of compliance. With the iXBRL requirement going into effect, companies that have addressed Item 106(b)(2) by including slightly vague or ambiguous disclosure in Item 1C or by cross-referencing their risk factors will need to carefully consider how they will handle these new tagging requirements.

The SEC adopted new rules requiring companies to disclose their policies and practices related to the timing of granting option awards (including stock appreciation rights) and the relationship between grants and the release of MNPI. Specifically, pursuant to Item 402(x) of Regulation S-K, companies must explain how the board decides when to grant these awards (e.g., whether they follow a set schedule), whether the board or compensation committee considers MNPI when deciding the timing and terms of such awards (and if so, how they consider such MNPI) and whether the company has timed the release of MNPI to influence the value of executive compensation. In addition, a new table is required to be included for option awards granted during the last fiscal year to a named executive officer within four business days before or one business day after the filing of a Form 10-Q or Form 10-K, or the filing or furnishing of a Form 8-K that discloses MNPI. Companies are required to include the narrative policies and practices disclosure regardless of whether the company has actually made grants of option awards close in time to the release of MNPI. Although these rules apply only to options and similar awards, we expect many companies to include, or expand on existing, narrative disclosures regarding their policies and practices related to the timing of full value awards as well (i.e., restricted stock units, restricted stock, and performance stock units).

2. Discuss Insider Trading Policies and Procedures in the Proxy Statement (and Form 10-K)

As a result of the overlapping obligations, this proxy statement requirement is discussed above in the section titled “New Form 10-K Disclosure Requirements.”

II. Disclosure Trends and Considerations for the 2024 Form 10-K

As previously discussed in our client alert “SEC Adopts New Rules on Cybersecurity Disclosure for Public Companies,” on July 26, 2023, the SEC adopted a final rule requiring public companies to provide current disclosure of material cybersecurity incidents and annual disclosure regarding cybersecurity risk management, strategy, and governance.

Under new Item 106, which is required to be addressed in new Item 1C of Form 10-K, public companies must include disclosures in their annual reports regarding their (1) cybersecurity risk management and strategy, including with respect to their processes for identifying, assessing, and managing cybersecurity threats and whether risks from cybersecurity threats have materially affected them; and (2) cybersecurity governance, including with respect to oversight by their boards and management.[8]

The new rule first applied to annual reports on Form 10-K for fiscal years ending on or after December 15, 2023, so most companies provided the required disclosure for the first time in 2024. Gibson Dunn surveyed disclosures made by 97 S&P 100 companies in response to Item 106 requirements as of November 30, 2024.[9] Set forth below is a summary of key trends and insights based on our analysis of these filings. The full results of this survey are included in our alert titled “Cybersecurity Disclosure Overview: A Survey of Form 10-K Cybersecurity Disclosures by the S&P 100 Companies.”

While certain disclosure trends have emerged under Item 106, we note that there is significant variation among companies’ cybersecurity disclosures, reflecting the reality that effective cybersecurity programs must be tailored to each company’s specific circumstances, such as its size and complexity of operations, the nature and scope of its activities, industry, regulatory requirements, the sensitivity of data maintained, and risk profile. Companies must strike a careful balance in their disclosures, providing sufficient decision-useful information for investors, while taking care not to reveal sensitive information that could be exploited by threat actors.[10] We expect company disclosures to continue to evolve as their practices change in response to the ever-evolving cybersecurity threat landscape and as common disclosure practices emerge among public companies.

The key disclosure trends we observed include the following:

- Materiality. The phrasing used by companies for this disclosure requirement varies widely. Specifically, in response to the requirement to describe whether any risks from cybersecurity threats have materially affected or are reasonably likely to materially affect the company, the largest group of companies (40%) include disclosure in Item 1C largely tracking Item 106(b)(2) language (at times, subject to various qualifiers); 38% vary their disclosure from the Item 106(b)(2) requirement in how they address the forward-looking risks; and 22% of companies do not include disclosure specifically responsive to Item 106(b)(2) directly in Item 1C, although a substantial majority of these companies cross-reference to a discussion in Item 1A “Risk Factors.”

- Board Oversight. Most companies delegate specific responsibility for cybersecurity risk oversight to a board committee and describe the process by which such committee is informed about such risks. Ultimately, however, the majority of surveyed companies report that the full board is responsible for enterprise-wide risk oversight, which includes cybersecurity.

- Cybersecurity Program. Companies commonly reference their program alignment with one or more external frameworks or standards, with the National Institute of Standards and Technology (NIST) Cybersecurity Framework being cited most often. Companies also frequently discuss specific administrative and technical components of their cybersecurity programs, as well as their high-level approach to responding to cybersecurity incidents.

- Assessors, Consultants, Auditors or Other Third Parties. As required by Item 106(b)(1)(ii), nearly all companies discuss retention of assessors, consultants, auditors or other third parties, as part of their processes for oversight, identification, and management of material risks from cybersecurity threats.

- Risks Associated with Third-Party Service Providers and Vendors. In line with the requirements of Item 106(b)(1)(iii), all companies outline processes for overseeing risks associated with third-party service providers and vendors.

- Drafting Considerations.

- Most companies organize their disclosure into two sections, generally tracking the organization of Item 106, with one section dedicated to cybersecurity risk management and strategy and another section focused on cybersecurity governance. Companies typically include disclosures responsive to the requirement to address material impacts of cybersecurity risks, threats and incidents in the section on risk management and strategy.

- The average length of disclosure among surveyed companies is 980 words, with the shortest disclosure at 368 words and the longest disclosure at 2,023 words. The average disclosure runs about a page and a half.

- Risk Factors. A substantial majority of companies include a cross-reference to their cybersecurity-related risk factor(s) in Item 1A “Risk Factors” or to risk factors included in Item 1A more generally.

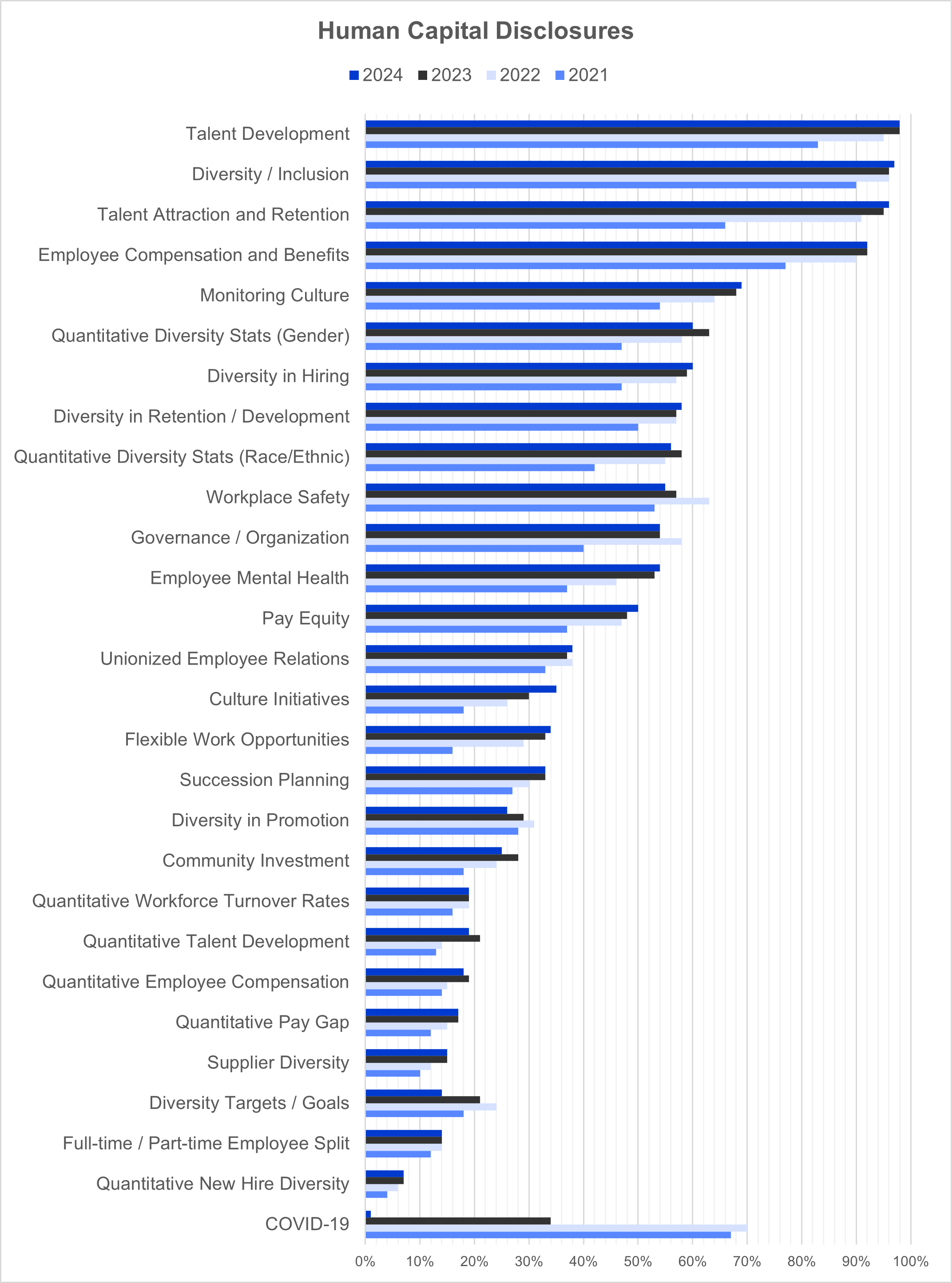

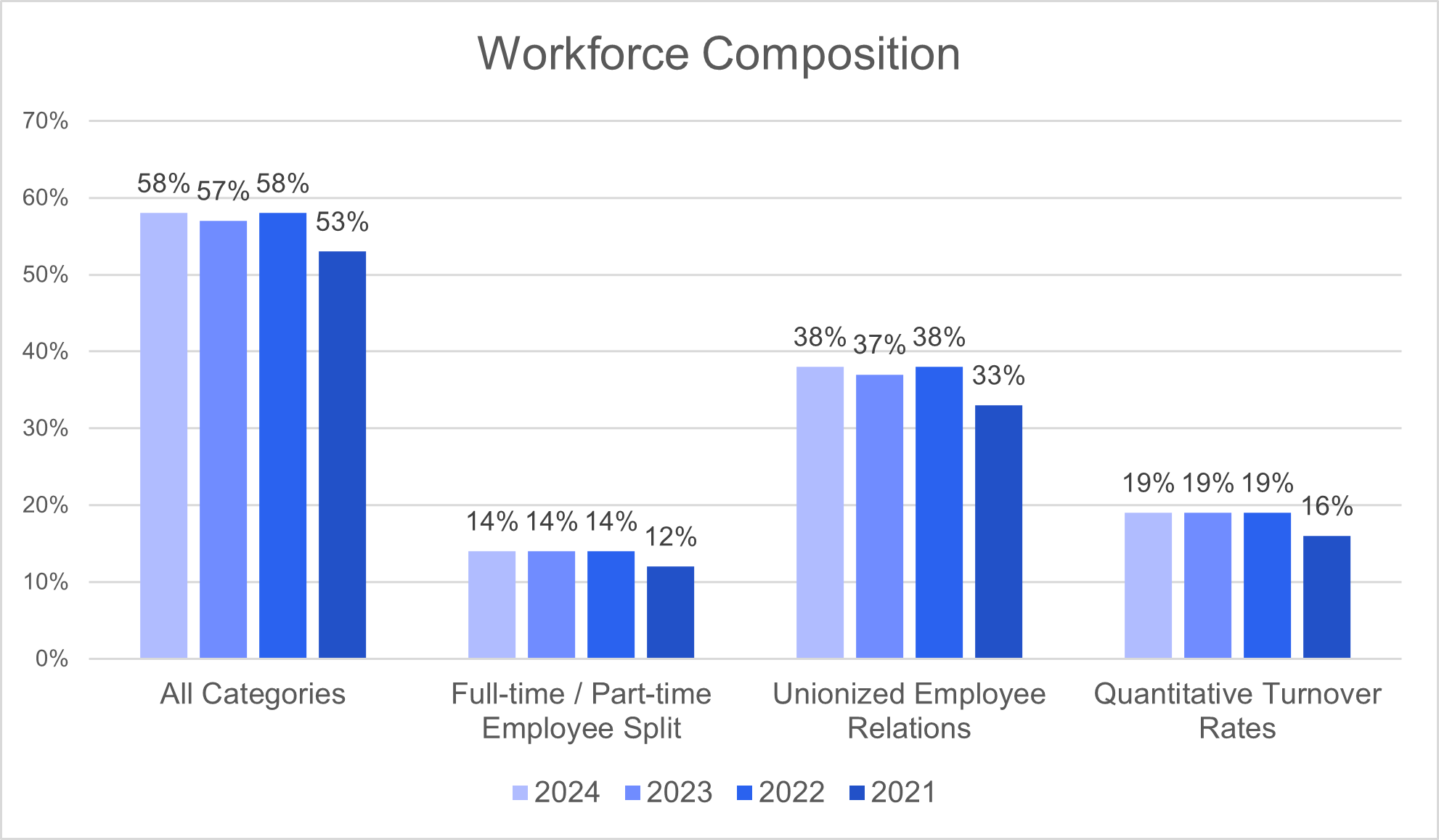

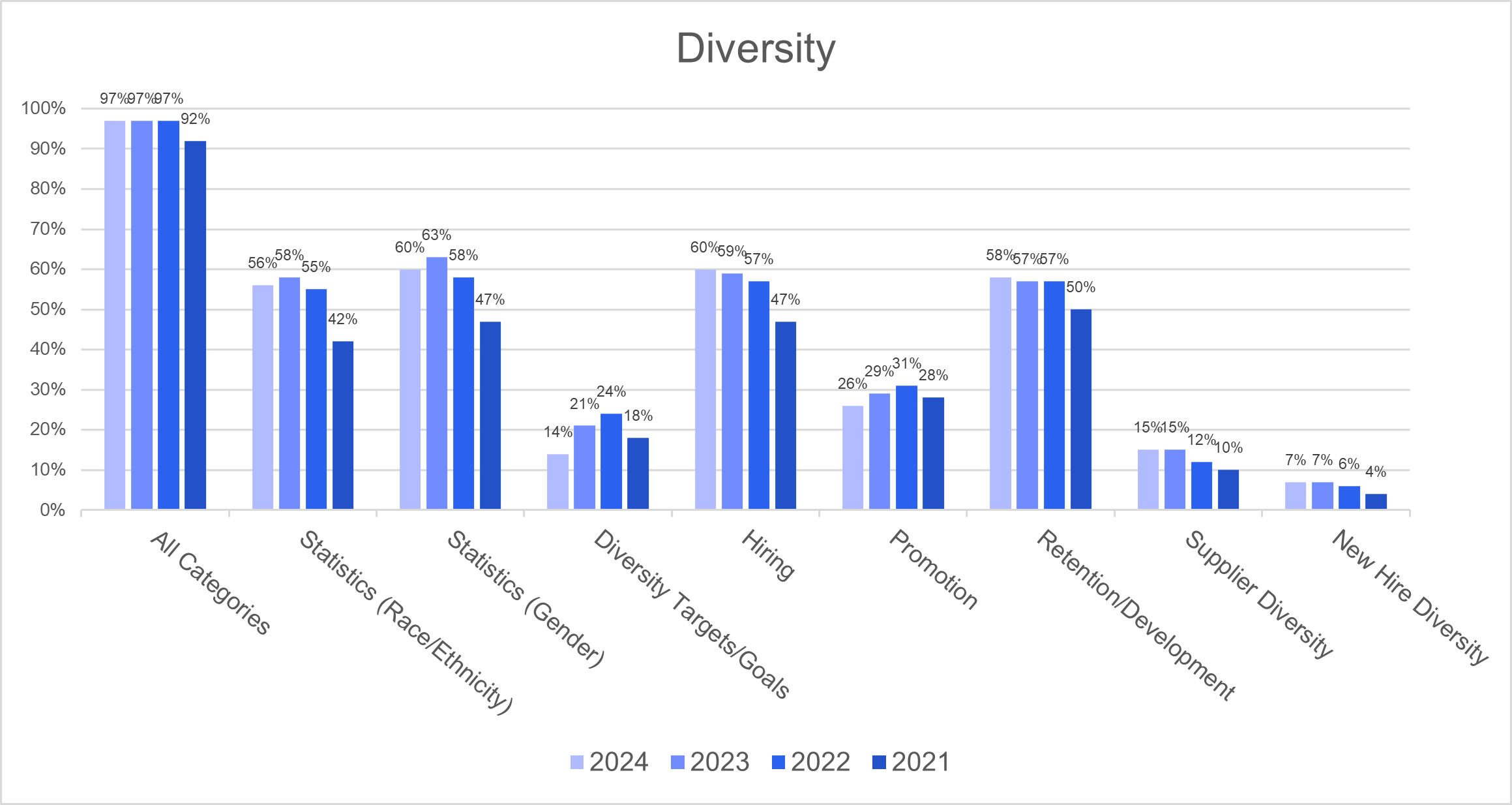

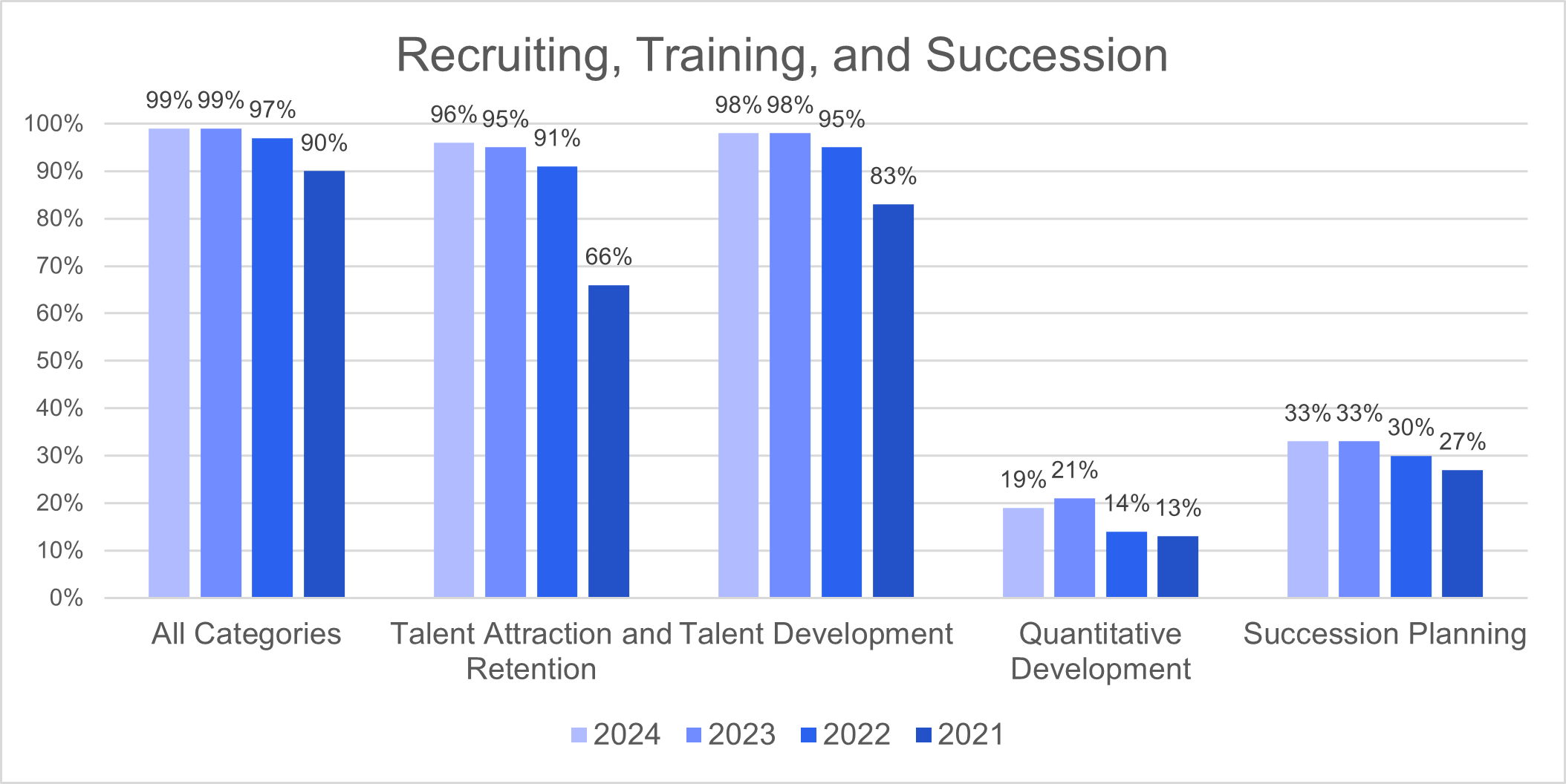

Human capital resource disclosures by public companies have continued to be a focus since the SEC adopted the new rules in 2020, not only for companies making the disclosures, but employees, investors, and other stakeholders reading them. As we have done for the past several years, we recently published a survey of the human capital resource disclosures from the S&P 100, available in our client alert titled “Four Years of Evolving Form 10-K Human Capital Disclosures.” The alert also provides practical considerations for companies as we head into 2025.

Overall, our findings indicate that companies are generally making only minor changes to their disclosures year over year, and these minor changes generally included shortening of company disclosures, maintaining or decreasing the number of topics covered, and including slightly less quantitative information in some areas.[11] Specifically, we identified the following trends regarding the S&P 100 companies’ human capital disclosures compared to the previous year:

- Length of disclosure. Fifty-seven percent of surveyed companies decreased the length of their disclosures, 34% increased the length of their disclosures, and the length of the remaining 9% remained the same.

- Number of topics covered. Forty-one percent of surveyed companies decreased the number of topics covered, 13% increased the number of topics covered, and the remaining 46% covered the same number of topics.

- Breadth of topics covered. Across all companies, the prevalence of 10 topics increased, nine topics decreased, and nine topics remained the same.

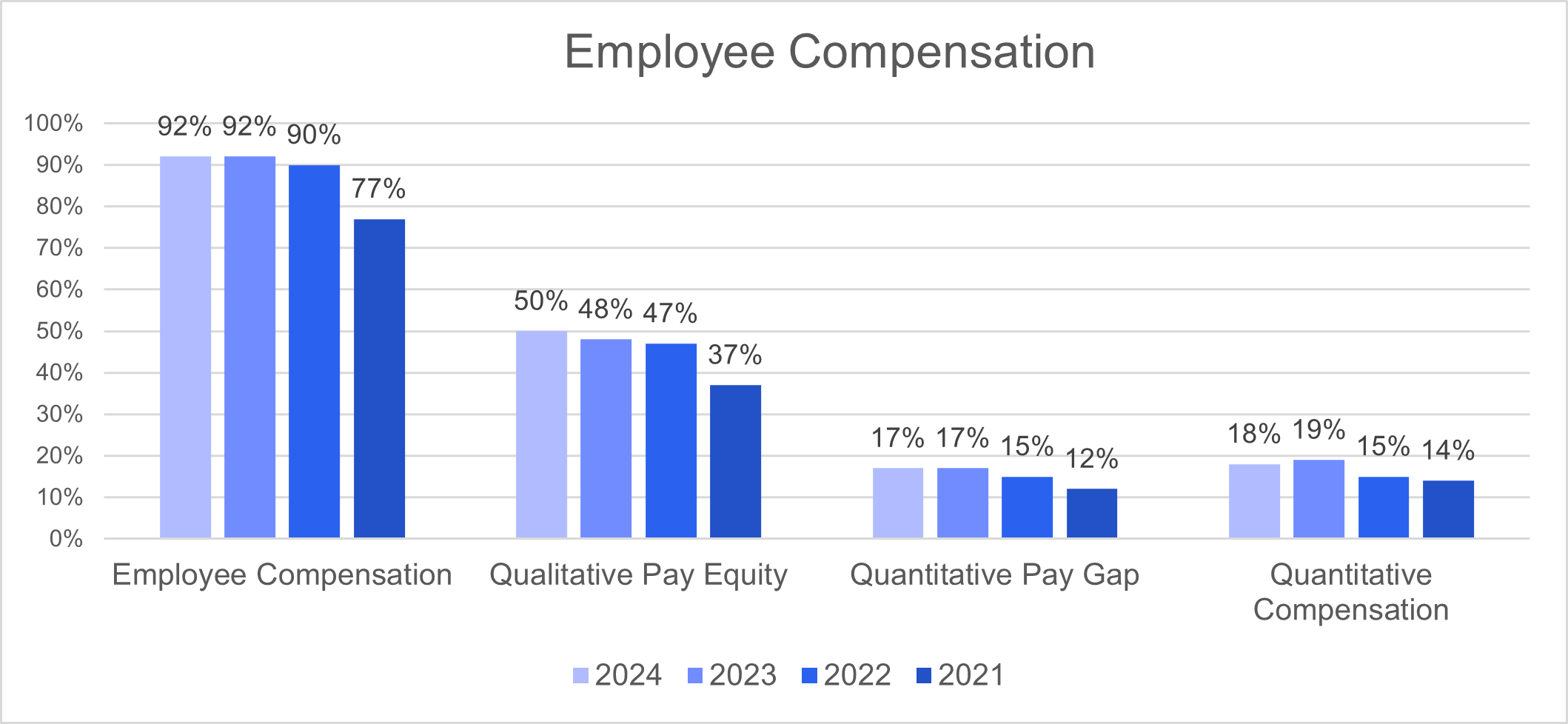

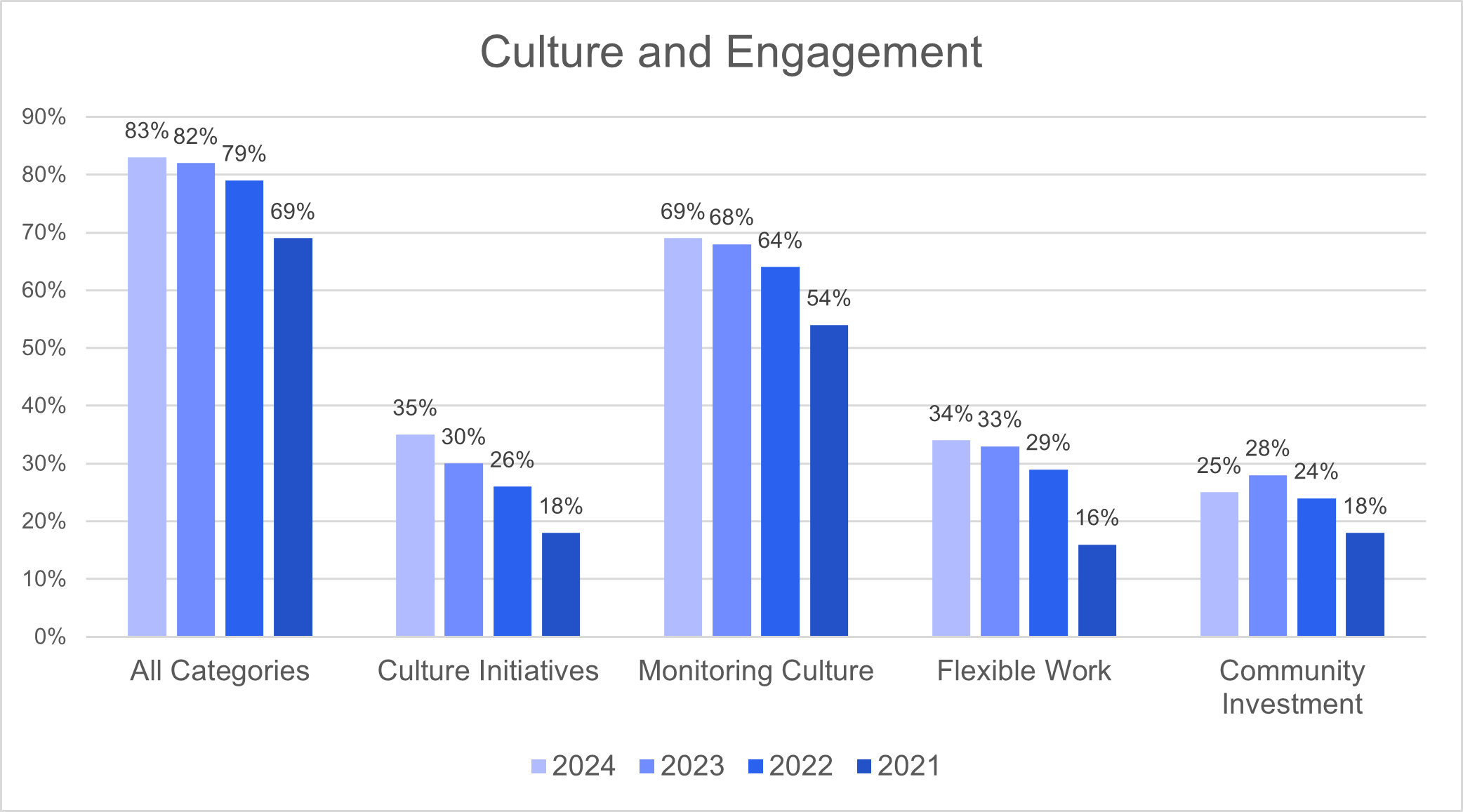

- The most significant year-over-year increases in frequency involved Culture Initiatives (30% to 35%) and Pay Equity (48% to 50%) disclosures.

- The most significant year-over-year decrease involved COVID-19 disclosures, which declined in frequency from 34% to 1%. Other year-over-year decreases related to disclosures addressing Diversity Targets and Goals (21% to 14%), Diversity in Promotion (29% to 26%), Quantitative Diversity Statistics regarding Gender (63% to 60%), and Community Investment (28% to 25%).

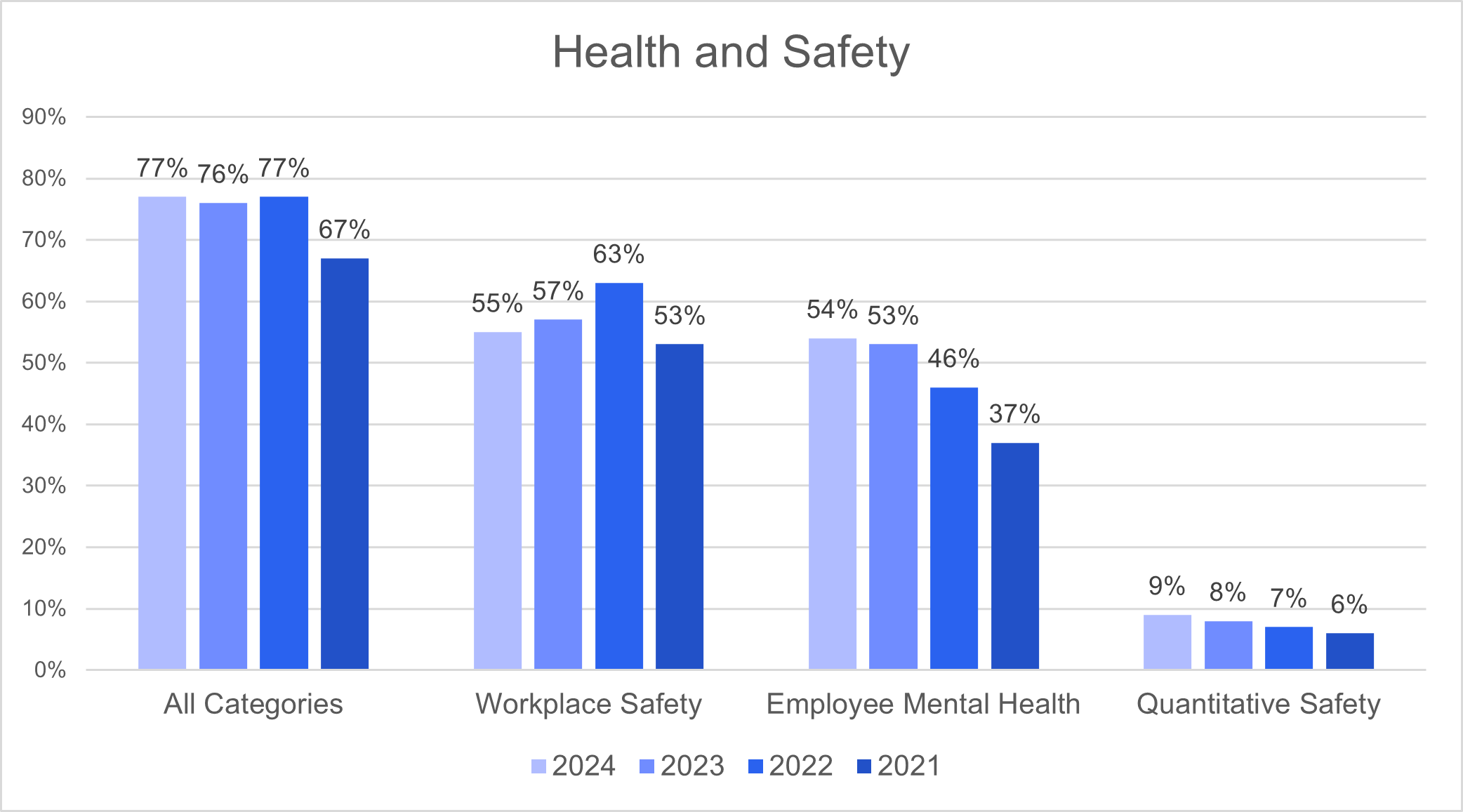

- Most common topics covered. This year, the topics most commonly discussed generally remained consistent with the previous two years. For example, Talent Development, Diversity and Inclusion, Talent Attraction and Retention, Employee Compensation and Benefits, and Monitoring Culture remained the five most frequently discussed topics. The topics least discussed this most recent year, however, changed slightly from that of the previous year as COVID-19 disclosures, and Diversity Targets and Goals dropped into the five least frequently covered topics.

- Industry trends. Within the technology and finance industries, the trends that we saw in the previous year regarding the frequency of topics disclosed generally remained the same.

The SEC adopted final climate disclosure rules in March 2024.[12] The rules established new disclosure requirements under Regulation S-K related to climate-related risks, governance, and strategy and greenhouse gas emissions (for certain large filers), as well as new financial statement reporting requirements in Regulation S-X related to severe weather events, carbon or energy products, and climate-related targets or transition plans.[13] Following the consolidation of several legal challenges in the Eighth Circuit, the SEC voluntarily stayed the rules in April 2024 pending the litigation’s outcome.[14]

While the litigation is ongoing and the rules do not apply to the upcoming Form 10-K, reporting companies should remain thoughtful about how existing SEC rules may nonetheless require disclosure on many of these topics, including in the risk factors section (related to material climate-related risks), the business section (related to, for example, material climate-related regulatory developments or changes to business strategy), and management’s discussion and analysis (“MD&A”) section (related to, for example, material costs incurred from unique events or invested in climate-related research and development).[15] It can also be prudent to assess the consistency of any sustainability-related disclosure in the Form 10-K with current or anticipated reporting on these topics in non-U.S. or voluntary filings, as mandatory sustainability reporting regulations continue to be adopted outside the United States and may create new areas of legal risk. In particular, companies that are preparing to report under the European Union’s Corporate Sustainability Reporting Directive should consider whether the results of their double materiality assessment or other analyses also require an update to the Form 10-K, including the risk factors discussion.[16]

The Division of Enforcement has also maintained its focus on sustainability-related disclosures and practices despite the dissolution of the standalone ESG Task Force earlier this year.[17] In September 2024, a multinational beverage company agreed to pay a $1.5 million civil penalty to settle SEC claims regarding past Form 10-K statements on testing of the recyclability of the company’s single-use beverage pods. The SEC alleged that statements concerning the successful testing of the recyclability of the pods incomplete and inaccurate by not including that two of the largest recycling companies had expressed concerns about the commercial feasibility of curbside recycling of small format materials and had indicated that at that time they did not intend to accept the pods at their facilities. Notably, the SEC asserted violations of only Section 13(a) of the Securities Exchange Act of 1934 and Rule 13a-1. This standard does not require that the disclosures be material or misleading, or that they be made with any intent—only that the disclosures included in an issuer’s SEC filings be complete and accurate. This enforcement action reinforces that even voluntary or immaterial disclosure on these and other topics may be the subject of regulatory scrutiny and should be appropriately vetted for completeness before filing.

As artificial intelligence (“AI”), including generative AI, becomes increasingly prevalent in the marketplace and incorporated into business operations, companies should assess whether they have adequate AI-related disclosure. Specifically, companies should consider the ways in which the company’s strategy, productivity, market competition and demand for the company’s products, investments and the company’s reputation, as well as legal and regulatory risks, could be affected by AI. To the extent material, disclosure about how the company uses AI and the risks related to its use should be provided in the description of business section, risk factors, MD&A, and the financial statements (as well as the discussion of the board’s role in risk oversight in the proxy statement), as applicable.

When making AI-related disclosures, companies should be careful of general language that could be interpreted as “AI Washing.”[18] As noted by Director Erik Gerding in the Division of Corporation Finance’s announcement in June, the Staff will consider how companies are describing AI-related opportunities and risks, including, to the extent material, whether or not the company: (1) clearly defines what it means by AI and how the technology could improve the company’s results of operations, financial condition and future prospects; (2) provides tailored, rather than boilerplate, disclosure about material risks related to AI; (3) focuses on the company’s current or proposed use of AI; and (4) has a reasonable basis for its claims when discussing AI prospects.[19]

In recent comment letters, the Staff has asked companies to provide additional context to their AI-related disclosure, including to explain the basis of AI-related performance claims and to provide specific descriptions of the AI technology being used by the company, such as the development, implementation and source of the technology, and risks related to such use.[20]

Public companies should continue to consider the evolving developments related to the continued conflicts between Russia and Ukraine and in the Middle East, as well as continued tensions between China and the United States, including as to whether risks associated with these developments are adequately discussed in the risk factors, as well as their direct and indirect impacts on their business, operating results, and financial condition.

As discussed in our client alert “Considerations for Preparing Your 2023 Form 10-K,” companies with operations in the People’s Republic of China (the “PRC”) should review the Division of Corporation Finance’s sample comment letter[21] highlighting three focus areas for periodic disclosures related to China-specific matters, including those arising from the Holding Foreign Companies Accountable Act (the “HFCAA”), the Uyghur Forced Labor Prevention Act, and specific government-related operational risks. In addition to posing questions regarding HFCAA disclosures, the sample letter includes comments directed at risk factors and MD&A disclosure.

Director Gerding of the Division of Corporation Finance communicated in June that the Staff would continue to focus on China-based companies and to elicit disclosure from companies on material risks they face from the PRC intervening in, or exercising control over, their operations in the PRC.[22] Director Gerding also noted that the Staff continues to believe that companies should provide more prominent, specific, and tailored disclosures about China-specific matters so that investors have the information they need to make informed investment and voting decisions.

While inflationary pressures have eased and interest rates have decreased as compared to 2023, companies should continue to consider whether their disclosures regarding inflation impacts and risks and uncertainty regarding inflation or future rate changes are adequately discussed, including in light of announced plans from President-elect Trump regarding the implementation of tariffs on U.S. imports as discussed below. Depending on the effect on a company’s operations and financial condition, additional disclosure in risk factors, MD&A, or the financial statements may be necessary.

In June, Director Gerding stressed that material ongoing impacts of inflation, including particularized risks, should continue to be disclosed and companies should not simply discuss high-level trends.[23] Additionally, given the market disruptions in the banking industry that began in 2023, the Staff also indicated that it would continue to scrutinize updated disclosures related to interest rate risk and liquidity risk.[24]

The President-elect has frequently reiterated plans to implement tariffs on U.S. imports of up to 20% on all imports generally, with higher rates for select U.S. trade partners, and has recently communicated that he will impose tariffs of 25% on imports entering the United States from Canada and Mexico, and an additional 10% tariff on imports from China, as one of his first executive orders. Implementation of these tariffs could adversely affect efforts to stem inflationary pressures in the United States and correspondingly influence interest rates. Companies should continue to monitor the risks associated with these proposed policies and confirm that such risks are adequately addressed in their disclosures, including if such proposed plans have already begun to impact their business.

In recent comment letters relating to inflation, the Staff has focused on how current inflationary pressures have materially impacted a company’s operations, including by referring to statements regarding inflation made in a company’s quarterly filings, and sought disclosure to quantify the impact and to identify planned or taken efforts to mitigate the impact of inflation. If inflation is identified as a significant risk, the Staff asked companies to update disclosure if inflationary pressures have resulted in a material impact, to identify the types of inflationary pressures being faced and to quantify the impact of factors contributing to inflationary pressures.[25]

In recent comment letters relating to interest rates, the Staff has asked companies to expand their discussion of interest rates in the risk factors and MD&A sections to specifically identify the impact on the company’s business operations and to discuss specific risk policies and procedures used by the company to manage and monitor interest rate risk.[26]

It is also critical that companies confirm that their disclosures in “Item 7A. Quantitative and Qualitative Disclosures About Market Risk” are up-to-date and responsive to the requirements of Item 305 of Regulation S-K.

III. Disclosure Trends and Considerations for the 2025 Proxy Statement

In August 2022, the Delaware General Corporation Law was amended to allow companies to amend their certificate of incorporation to exculpate certain officers from personal liability for monetary damages for breaches of fiduciary duty in a manner similar to, but more narrow than, what is currently permitted for directors.

Such exculpation provisions apply only to direct claims against officers alleging a breach of fiduciary duty of care and provide a basis for early dismissal of certain claims in the preliminary stages of litigation, before extensive and expensive discovery. Because insurance and indemnification already serve to protect officers’ assets in such cases, the company is the primary beneficiary of extending exculpation to officers. This protection must be implemented through an amendment to the company’s certificate of incorporation, requiring both board and shareholder approval.

Although companies initially faced uncertainty regarding the reception of these amendments by proxy advisory firms and institutional investors, most proposals have received strong investor support during 2023, and this support continued in 2024. Between the 2023 and 2024 proxy seasons, approximately 27% of all S&P 500 companies incorporated in Delaware proposed exculpation amendments; all but three (96%) received stockholder approval.[27] Institutional Shareholders Services tends to support these proposals on a case-by-case basis, while Glass Lewis tends to oppose them, absent a “compelling rationale.”

The adoption of officer exculpation amendments reflects evolving expectations around liability protections for corporate officers. Companies contemplating such amendments should consider whether to engage with shareholders in advance to address potential concerns.

Institutional investors are increasingly scrutinizing directors’ time commitments to ensure effective governance. While the primary focus remains adhering to strict numerical limitations on the number of public company boards a director should serve on (generally, no more than two boards for directors who are executive officers and no more than four boards for non-executive directors), there is an increasing push to require companies to disclose their internal director time commitment policies and demonstrate adherence to such policies.[28] With a view to demonstrating the company’s responsiveness to evolving investor expectations and commitment to robust corporate governance, companies should revisit their policy and the processes used by their nominating committee or board of directors to assess director candidates in determining to nominate them for election to the board of directors and consider whether any enhancements are appropriate.

Companies should take a fresh look at their vetting processes to support disclosures with respect to director independence determinations. In 2024, the SEC brought settled charges against a director for proxy rule violations after he was identified in the company’s proxy statement as independent despite maintaining a close personal relationship with an executive officer of the company. The director did not disclose this relationship to the board of directors, thereby allegedly causing the company’s proxy statement to contain materially misleading statements. This enforcement action highlights the need for rigorous diligence in assessing relationships and transactions that could compromise a director’s independence. In light of these developments, companies should assess their independence determination processes, including reviewing their annual directors’ questionnaires and considering whether there are any opportunities to enhance board or nominating committee oversight and related proxy disclosures.

Most companies have already complied with the SEC’s “pay versus performance” (“PvP”) disclosure rules in their annual 2023 and 2024 proxy statements. As companies begin to prepare their 2025 disclosures, we’ve highlighted some notable trends and developments below based on prior proxy seasons and comment letters from the Staff:

- One additional year. Reminder that companies must add 2024 as an additional year to the PvP table and should not remove any years until after the PvP table contains five years total (three years for smaller reporting companies).

- Relationship disclosures. Although the rule permits graphical, narrative, or a combination thereof to describe the relationship between compensation actually paid and the various performance metrics, the comment letters from the Staff indicate a preference for graphical depictions. Graphical depictions have also been the majority practice during the last two proxy seasons.

- Metrics reporting. The Staff has placed an emphasis on ensuring (i) the compensation numbers included in the PvP table reconcile with those disclosed in the Summary Compensation Table, (ii) any Generally Accepted Accounting Principles (“GAAP”) numbers used, including net income, reconcile to the applicable numbers disclosed on the company’s Form 10-K, (iii) companies include clear descriptions of how they calculated any non-GAAP numbers included in the PvP disclosure, and (iv) the company-selected measure in the PvP table is included in the company’s list of the most important measures used to link pay and performance.

- Reconciliations. As a reminder, footnote reconciliations of the amounts deducted and added to calculate compensation actually paid for years other than the most recent fiscal year are required only if material to an understanding of the PvP information reported for the most recent fiscal year. As such, many companies can streamline their PvP disclosures by omitting prior years’ footnote reconciliations. In line with such guidance, the Staff has indicated that if a company revises the compensation actually paid included for prior fiscal years, then footnote reconciliations for such prior years should be included.

- Precise headings. The Staff has placed an emphasis on avoiding the use of vague terms in the headings of PvP table footnote reconciliations, such as “year-over-year.” Instead, the Staff prefers specific headings that track closely to the language of the rules, such as “prior fiscal year end to current fiscal year end” or “prior fiscal year end to vesting date.”

- Peer group changes. As a reminder, if the peer group used for peer group total shareholder return (“TSR”) disclosures in the PvP table changes from the prior year, the footnote must include the reason for the change and a comparison of the company’s TSR with that of both the new peer group and the peer group from the prior year.

In light of the above, companies should review their PVP table and related disclosures to incorporate and consider whether any improvements are necessary to comply with the latest SEC guidance.

The SEC continues to bring enforcement actions against companies relating to perquisite disclosure (as recently as this month), so companies may want to revisit their director and officer questionnaire and other disclosure control processes ahead of the upcoming proxy statement. Perquisites facing scrutiny include personal travel and commuting (including use of corporate aircraft), personal expenses, personal entertainment, personal transportation and personal security.

On December 11, 2024, the U.S. Court of Appeals for the Fifth Circuit vacated the SEC’s approval of Nasdaq’s board diversity disclosure rules, which previously required Nasdaq-listed companies to annually disclose a board diversity matrix with information about each of its director’s self-identified gender and demographic characteristics. Nasdaq has communicated that it does not intend to seek further review. As a result, companies will no longer be required to follow Nasdaq’s board diversity disclosure rules but may want to consider relevant investment community expectations when assessing any changes to their proxy disclosures.

IV. SEC Comment Letter Trends[29]

In 2024, comment letters from the Staff continued an emphasis on addressing disclosures in MD&A as well as the use of non-GAAP measures. Notably, following the adoption and subsequent stay of the SEC’s final climate disclosure rule in 2024, the number of comment letters from the Staff regarding companies’ climate-related disclosures decreased as the SEC reprioritized its focus areas.

Many of the comment letters addressing MD&A continued to focus on disclosures relating to results of operations, with the Staff often requesting that companies explain related disclosures with more specificity. The Staff has continued to focus on disclosures regarding material period-to-period changes in quantitative and qualitative terms as prescribed by Item 303(b) of Regulation S-K. For example, the Staff has commented on disclosures about factors contributing to period-on-period changes in financial line items, such as revenue, gross margin, cost of sales, expenses and operating cash flows, to request that companies provide both more quantitative detail regarding the extent to which each factor had contributed to the overall change in the line item, as well as qualitative discussion of the underlying factors attributable to such contributing factors.[30] The Staff often requested companies to “use more definitive terminology, rather than general or vague terms such as ‘primarily,’ to describe each contributing factor.”[31] The Staff has also continued to request that companies make disclosures about known trends and uncertainties affecting their results of operations.[32]

Another area that the Staff has continued to focus on is ensuring that key performance indicators (“KPIs”) are properly contextualized so that they are not misleading.[33] The Staff has, in certain circumstances, requested that companies provide additional disclosures regarding how KPIs are defined and calculated, why they are useful to investors and how they are used by management.[34] In addition, the Staff asked companies why KPIs or other performance metrics are discussed in earnings releases or investor presentations if not also discussed in their periodic reports or presented inconsistently.[35]

The Staff has also often asked companies to quantify and provide additional disclosure regarding significant components of financial condition and results of operations that have affected segment results.[36]

Two other key areas of MD&A that the Staff continued to focus on were critical accounting estimates and liquidity and capital resources. The Staff frequently noted that companies’ disclosures regarding critical accounting estimates were too general and requested that companies provide a more robust analysis, including both qualitative and quantitative information necessary to understand the estimation uncertainty and its impact on the financial statements, consistent with the requirement now set forth in Item 303(b)(3).[37] The Staff often indicated that these disclosures should supplement, not duplicate, the disclosures in footnotes to financial statements.[38] The Staff frequently commented on cash flows disclosures regarding enhancing the comparative analysis of the drivers of material changes period-on-period and the underlying reasons for such material changes, with a view to provide investors an understanding of trends and variability in cash flows.[39] The Staff also noted that such disclosures should not merely recite changes evident in the financial statements.[40]

The Staff has continued to express concerns regarding the improper use of non-GAAP measures in filings and issued several comments aligned with the Staff’s Compliance and Disclosure Interpretations (“C&DIs”).[41] Comments related to the latest C&DIs continued to focus on whether operating expenses are “normal” or “recurring” (Non-GAAP C&DI 100.01), and, therefore, whether exclusion from non-GAAP financial measures might be misleading.[42] The Staff has also asked companies about whether certain non-GAAP adjustments to revenue or expenses have made the adjustments “individually tailored” (Non-GAAP C&DI 100.04).[43] In addition to a continued focus on the topics covered under the C&DIs, the Staff continued to focus on a number of other matters relating to compliance with Item 10(e) of Regulation S-K, including the prominence of non-GAAP measures, reconciliations to GAAP measures and the usefulness and purpose of particular non-GAAP measures.