On August 30, 2023, the U.S. Department of Labor issued a proposed rule to revise its regulations implementing minimum wage and overtime exemptions for executive, administrative, and professional employees, among others, under the Fair Labor Standards Act (“FLSA”). The proposal, if finalized, would revise the minimum wage and overtime exemptions issued by the Trump Administration in 2019, which have been in effect since January 1, 2020.

Among other things, the proposal would increase the compensation thresholds that are used when determining whether an employee qualifies for the executive, administrative, or professional exemptions. Under the Department’s existing regulations an employee qualifies for an exemption if: (1) she is paid a predetermined and fixed salary that is not subject to reduction because of variations in the quality or quantity of work performed; (2) the amount of salary paid meets a minimum specified amount; and (3) her job duties are primarily executive, administrative, or professional. The Department has periodically revised the minimum salary component of the test, most recently in 2019, when it set the minimum salary at $684 per week ($35,568 on an annual basis).

The Department’s proposal would increase the salary threshold substantially. The Department proposes to increase the threshold to at least $1,059 per week, which is approximately $55,000 per year, representing a nearly 55 percent increase over the current threshold. The proposal also leaves open the possibility that the Department might use more recent wage data when it finalizes the rule, which means the compensation thresholds could easily be as high as $1,140 or $1,158 per week, or approximately $60,000 per year. (A higher threshold applies under state law in only a handful of states, such as California which requires that exempt employees earn at least $1,240 per week.) These increases are the result of the Department’s proposal to tie the compensation thresholds to the 35th percentile of wage survey data of full-time salaried workers in the lowest-wage Census Region—as opposed to 20th percentile of wage survey data of full-time salaried workers in the lowest-wage Census Region and of retail workers nationally.

The proposal would also increase the compensation threshold for the highly compensated employees exemption. Employees earning at least $107,432 annually currently qualify for this exemption if they regularly perform at least one executive, administrative, or professional duty. The Department proposes to increase the compensation threshold to $143,988, an increase of approximately 34 percent.

These changes to the Department’s compensation thresholds would, if implemented, have significant consequences for many employers. It is estimated that the changes will expand the number of workers who would be eligible for overtime wages by at least 3.6 million.

The Department also proposes to automatically increase the compensation thresholds every three years to account for changes in wage survey data collected by the Bureau of Labor Statistics. If implemented, the automatic increase mechanism would likely result in significantly higher compensation thresholds in the coming years.

Increases to the compensation threshold, including automatic increases, were included in the Obama Administration’s 2016 rule. That rule, which would have increased the compensation threshold to $913 per week ($47,476 on an annual basis), was enjoined before it took effect. It was later struck down by the U.S. District Court for the Eastern District of Texas on the grounds that the Department’s reliance on salary thresholds to the exclusion of an analysis of employees’ job duties exceeded the Department’s authority under the statute. A similar challenge should be expected to any final rule resulting from the Department’s new rulemaking, particularly in light of Justice Kavanaugh’s dissent in Helix Energy Solutions Group, Inc. v. Hewitt, 598 U.S. 39 (2023), which suggested that the Department’s compensation threshold test may be inconsistent with the FLSA.

Interested parties will have 60 days to submit comments on the proposed rule after it is published in the Federal Register. The Department may issue a final rule as soon as early-to-mid 2024. As noted, legal challenges are possible once a final rule is adopted.

The following Gibson Dunn attorneys assisted in preparing this client update: Eugene Scalia, Jason Schwartz, Katherine Smith, Andrew Kilberg, and Blake Lanning.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. To learn more about these issues, please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s Labor and Employment or Administrative Law and Regulatory practice groups, or the following authors and practice leaders:

Eugene Scalia – Co-Chair, Administrative Law & Regulatory Group, Washington, D.C.

(+1 202-955-8210, [email protected])

Jason C. Schwartz – Co-Chair, Labor & Employment Group, Washington, D.C.

(+1 202-955-8242, [email protected])

Katherine V.A. Smith – Co-Chair, Labor & Employment Group, Los Angeles

(+1 213-229-7107, [email protected])

Helgi C. Walker – Co-Chair, Administrative Law & Regulatory Group, Washington, D.C.

(+1 202-887-3599, [email protected])

© 2023 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

Orange County partner Blaine Evanson and Washington, D.C. associate Jeremy Christiansen are the authors of “How ‘Purely Legal’ Issues Ruling Applies To Rule 12 Motions” [PDF] published by Law360 on August 30, 2023.

Los Angeles partner Theodore Boutrous and New York associates Lee Crain and Randi Kira Brown are the authors of “How NY SLAPP Defendants Can Recover Fees In Fed. Court” [PDF] published by Law360 on August 29, 2023.

New York associate Connor Sullivan contributed to the article.

Because of an expiring transition rule, a partner that currently relies on a “bottom dollar guarantee” to support an allocation of liabilities may be required to recognize gain under section 731(a) unless that partner takes action before October 4, 2023.[1] After a brief overview and discussion of the applicable Treasury regulations, we describe the action that should be taken.

I. Overview

In October 2019, the IRS and Treasury issued final regulations (the “2019 Regulations”) that provide that “bottom dollar payment obligations” (commonly referred to as “bottom dollar guarantees”) do not cause a partnership’s liabilities to be treated as recourse with respect to the partner providing the guarantee. The result of this rule is that a bottom dollar guarantee does not cause the guaranteed liability to be allocated to the partner providing the guarantee.[2] The absence of such an allocation may cause the partner providing the guarantee to recognize gain in an amount up to the amount of the liabilities. The 2019 Regulations are effective for partnership liabilities incurred and guarantees entered into on or after October 5, 2016.

The 2019 Regulations include a seven-year transition rule for a partner that had a “negative tax capital account” immediately before October 5, 2016 and was relying on an allocation of recourse liabilities to avoid gain recognition. In general, a partner would have a “negative tax capital account” to the extent that the partner has previously been allocated losses or deductions or received distributions from the partnership in excess of the partner’s capital investment in the partnership (i.e., capital contributions to the partnership and previous allocations of income or gain by the partnership to the partner). The transition rule also applies to liabilities incurred and payment obligations entered into before October 5, 2016 that were subsequently refinanced or modified.

When the transition rule expires on October 4, 2023, bottom dollar guarantees will no longer be effective to cause partnership liabilities to be treated as recourse with respect to the partner providing the guarantee. As a result, absent other action, the partner may recognize gain under section 731(a) to the extent of the partner’s remaining “negative tax capital account.”

II. Discussion

A. Background on the Allocation of Partnership Liabilities

An entity that is classified as a partnership for U.S. federal income tax purposes allocates its liabilities among its partners in accordance with section 752 and the regulations interpreting section 752. Any liability that is allocated to a partner increases that partner’s basis in its partnership interest. A partner with a share of liabilities may, therefore, be able to receive greater distributions of money from the partnership without recognizing gain under section 731(a) or claim deductions for a greater amount of partnership deductions than would be possible without the share of liabilities.

When a partner’s share of a liability decreases—whether because the liability is repaid or because it is allocated to a different partner—the partner whose share decreases is treated as receiving a distribution of money in an amount equal to the reduction. If the amount of the reduction exceeds the partner’s basis in its interest, the partner recognizes taxable gain under section 731(a).

Whether a partnership liability is allocated to a particular partner depends, in the first instance, on whether the liability is “recourse” or “nonrecourse.” A liability that is “recourse” to a particular partner is allocated to that partner. A liability that is not recourse to any particular partner is considered “nonrecourse” and generally is allocated among all partners (though, in many cases, there is substantial flexibility with respect to the allocation of nonrecourse liabilities under Treas. Reg. § 1.752-3).

For this purpose, a liability is a recourse liability when a partner or related person bears the “economic risk of loss” with respect to that liability. To determine whether any partner or related person bears the economic risk of loss with respect to a liability, the Treasury regulations require the partnership to determine whether any partner would have a “payment obligation” if all of the assets of the partnership (including cash) became worthless and the liabilities became due (this is sometimes referred to as the “atom bomb test”).[3]

B. Use of Guarantees to Cause Allocations of Liabilities

A partner that wishes to be allocated a share of partnership liabilities in excess of its share of nonrecourse liabilities sometimes will guarantee repayment of some or all of the partnership’s liabilities. For example, if a partner with a $0 basis in its interest is entitled to a distribution of money from the partnership, and the partner does not want to recognize taxable gain on the distribution, the partner might guarantee a partnership liability before the distribution. If the amount of the guarantee is at least equal to the amount of money to be distributed, the distribution does not cause the partner to recognize gain under section 731(a) because the liability “supports” the distribution by providing additional basis.

This well-understood and perfectly acceptable planning technique, of course, is not without economic risk; a partner that guarantees a liability may be called upon to satisfy that guarantee. With lower-leverage partnerships, this can be relatively low risk. In a higher-leverage partnership—for example, certain real estate joint ventures—however, the risk can be more significant.

Before the issuance of temporary Treasury regulations in October 2016, a partner that sought to be allocated a share of liabilities while reducing the associated economic exposure sometimes entered into a so-called “bottom dollar guarantee.” Unlike other guarantees (in which the guarantor is liable for the amount guaranteed beginning with the first dollar of the unsatisfied outstanding principal balance), a bottom dollar guarantee requires the guarantor to make a payment only to the extent that the lender ultimately collects less than the amount guaranteed. That is, a bottom dollar guarantee exposes the guarantor to the last dollars of loss rather than the first. A bottom dollar guarantee thus caused a liability to be a recourse liability that exposed the guarantor to lower risk while still constituting sufficient risk exposure to support an allocation of liabilities (in an amount equal to the guarantee). This allowed the partner providing the guarantee to avoid gain recognition to the extent of the associated liabilities.

C. IRS and Treasury Response to Bottom Dollar Guarantees

The IRS and Treasury perceived bottom dollar guarantees as lacking commercial substance and, in January 2014, proposed an initial set of regulations seeking to curb their use. Under the final 2019 Regulations, “bottom dollar payment obligations” are not recognized (i.e., a bottom dollar guarantee does not result in the guarantor partner being treated as having the economic risk of loss with respect to the liability). Under the regulations, a bottom dollar payment obligation generally includes any payment obligation under a guarantee or similar arrangement with respect to which the partner (or a related person) is not liable for up to the full amount of the payment obligation in the event of non-payment by the partnership. In other words, the lender must be able to recover from the guarantor beginning with the lender’s first dollar of loss. In determining whether a guarantee meets the definition of a bottom dollar payment obligation, and, relatedly, whether the partner (or a related person) bears the economic risk of loss, every aspect of the guarantee must be considered, including whether, by reason of contract, state law, or common law, the partner has a reimbursement or contribution right (for example, by claiming reimbursement or contribution from the joint venture on a priority basis relative to the other partners, from the other partners, or from third parties).

The determination of whether a particular guarantee meets the definition of “bottom dollar payment obligation” is, therefore, a mixed issue of law and transaction-specific facts.

D. Special Rule for “Vertical Slice” Guarantees

One important clarification of the bottom dollar guarantee rules is the rule for so-called “vertical slice” guarantees. The 2019 Regulations provide that a guarantee is not a bottom dollar guarantee if the guaranteed obligation equates to a fixed percentage of every dollar of the guaranteed partnership liability. That is, a partner does not need to guarantee the entire liability but rather can guarantee a “vertical slice” of the entire liability. For example, suppose a partner agrees to guarantee ten percent of a $100 million partnership liability, which would be $10 million. In a typical guarantee, the partner would be liable for the first $10 million of the lender’s losses—that is, if the lender recovers less than $100 million, the guarantor is liable for up to $10 million. If, however, the partner enters into a “vertical slice guarantee” for ten percent of the lender’s loss up to the same $10 million amount, the partner would be liable for ten percent of each dollar of the lender’s loss, thus reducing its effective economic exposure in the event of a loss. That is, if the lender recovered only $60 million from the partnership, the guarantor would be liable for $4 million (ten percent of the $40 million loss). Unlike a bottom dollar guarantee (which, in the example, would not have resulted in a payment obligation because the lender recovered in excess of the $10 million guaranteed amount), a “vertical slice guarantee” exposes a guarantor partner to liability from the first dollar of loss.

Accordingly, a partner seeking to provide a guarantee of only a portion of a partnership liability may be able to use a “vertical slice guarantee” to accomplish this goal while reducing economic exposure in the event of a loss.

E. Anti-Abuse Rule

The 2019 Regulations contain an anti-abuse rule pursuant to which a payment obligation is disregarded if the facts and circumstances indicate a plan to circumvent or avoid the obligation. Factors cited by the regulations as evidence of such a plan include the partner (or a related person) not being subject to commercially reasonable contractual restrictions that protect the likelihood of payment and that the terms of the partnership liability would be substantially the same had the partner (or related person) not agreed to provide the guarantee. These rules should be considered if entering into a guarantee or other payment obligation.

III. How May The Expiration Of The Transition Rule Impact You?

If you:

- are a partner in an entity classified as a partnership for U.S. federal income tax purposes;

- guaranteed one or more partnership liabilities before October 5, 2016; and

- your share of partnership liabilities exceeded your basis in your partnership interest at that time;

then you should consult your tax lawyers to determine whether the guarantee is a bottom dollar payment obligation. If it is, the transition rule described above will expire on October 4, 2023, and you should consider whether to take any action before that date. Actions that can be taken include entering into a replacement guarantee that complies with the 2019 Regulations before October 4, 2023. If you do not, you may recognize gain equal to all or a portion of your current “negative tax capital account,” either in 2023 or later.

____________________________

[1] Unless indicated otherwise, all “section” references are to the Internal Revenue Code of 1986, as amended (the “Code”), and all “Treas. Reg. §” references are to the Treasury regulations promulgated under the Code.

[2] The 2019 Regulations finalized temporary regulations promulgated in T.D. 9788 on October 5, 2016.

[3] There is a special rule for liabilities with respect to which the lender may look only to specific partnership assets. In that case, the liability is treated as satisfied by transferring the property to the lender.

This alert was prepared by Emily Leduc Gagné,* Evan M. Gusler, James Jennings, Andrew Lance, and Eric B. Sloan.

Gibson Dunn lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, the authors, or any of the following leaders and members of the firm’s Tax or Real Estate practice groups:

Tax Group:

Dora Arash – Los Angeles (+1 213-229-7134, [email protected])

Sandy Bhogal – Co-Chair, London (+44 (0) 20 7071 4266, [email protected])

Michael Q. Cannon – Dallas (+1 214-698-3232, [email protected])

Jérôme Delaurière – Paris (+33 (0) 1 56 43 13 00, [email protected])

Michael J. Desmond – Los Angeles/Washington, D.C. (+1 213-229-7531, [email protected])

Anne Devereaux* – Los Angeles (+1 213-229-7616, [email protected])

Matt Donnelly – Washington, D.C. (+1 202-887-3567, [email protected])

Pamela Lawrence Endreny – New York (+1 212-351-2474, [email protected])

Benjamin Fryer – London (+44 (0) 20 7071 4232, [email protected])

Kathryn A. Kelly – New York (+1 212-351-3876, [email protected])

Brian W. Kniesly – New York (+1 212-351-2379, [email protected])

Loren Lembo – New York (+1 212-351-3986, [email protected])

Jennifer Sabin – New York (+1 212-351-5208, [email protected])

Hans Martin Schmid – Munich (+49 89 189 33 110, [email protected])

Eric B. Sloan – Co-Chair, New York (+1 212-351-2340, [email protected])

Jeffrey M. Trinklein – London/New York (+44 (0) 20 7071 4224 /+1 212-351-2344), [email protected])

Edward S. Wei – New York (+1 212-351-3925, [email protected])

Lorna Wilson – Los Angeles (+1 213-229-7547, [email protected])

Daniel A. Zygielbaum – Washington, D.C. (+1 202-887-3768, [email protected])

Emily Leduc Gagné* – New York (+1 212-351-6387, [email protected])

Evan M. Gusler – New York (+1 212-351-2445, [email protected])

James Jennings – New York (+1 212-351-3967, [email protected])

Real Estate Group:

Andrew Lance – New York (+1 212-351-3871, [email protected])

*Anne Devereaux is of counsel in the firm’s Los Angeles office who is admitted only in Washington, D.C.; Emily Leduc Gagné is an associate in the firm’s New York office who is admitted in Ontario, Canada.

© 2023 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

On August 23, 2023, the U.S. Securities and Exchange Commission (the “SEC”) by a 3-2 vote adopted final rules (the “Final Rules”) under the Investment Advisers Act of 1940, as amended (the “Advisers Act”), which modify certain aspects of the rules initially proposed on February 9, 2022 (the “Proposed Rules”) and adopt others largely as proposed. The Final Rules reflect the SEC’s asserted goal of bringing “transparency” to the inner workings of private funds and their sponsors by restricting or requiring extensive disclosure of preferential treatment granted in side letters, as well as imposing numerous additional reporting and other compliance requirements.[1] While several of the Final Rules require further clarification, and industry practice will undoubtedly evolve as the Final Rules are further analyzed and, to the extent possible, implemented, the following table sets forth a high-level overview of key requirements and restrictions reflected in the Final Rules. Following the table is a Q&A addressing some of the most frequently asked questions sponsors and other industry participants have asked us. These materials are a general, initial summary and do not assess the legality of the Final Rules, which remain subject to potential challenge.

Private Funds Rules – Overview of Key Requirements and Restrictions

|

Requirement or Restriction |

High-Level Observations |

|

|

Preferential Treatment Rule (Disclosure Requirements): An adviser may not admit an investor into a fund unless it has provided advance disclosure of material economic terms granted preferentially to other investors, and must disclose all other preferential treatment “as soon as reasonably practicable” after the end of the fundraising period (for illiquid funds) or the investor’s investment (for liquid funds) and at least annually thereafter (if new preferential terms are granted since the last notice). |

As set forth below, this requirement fundamentally changes the rules of the game with respect to a fund’s typical MFN process and requires advance disclosure of material economic terms, including to those investors who are not entitled to elect them, and to those who would not typically see them (e.g., smaller investors who do not have side letters).Because the disclosure requirements apply to existing funds, older funds will need to disclose preferential treatment previously granted but not yet disclosed. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers) Existing funds grandfathered? No. |

|

Quarterly Statement Rule: Registered advisers must issue quarterly statements detailing information regarding fund-level performance; the costs of investing in the fund, including itemized fund fees and expenses; the impact of any offsets or fee waivers; and an itemized accounting of all amounts paid to the adviser or its related persons by each portfolio company. |

As set forth below, the requirement to show performance metrics for illiquid funds, both with and without the impact of fund-level subscription facilities, and to spell out clearly all fund-level and portfolio company-level special fees and expenses (e.g., monitoring fees) and provide a cross-reference to the section of the private fund’s organizational and offering documents setting forth the applicable calculation methodology with respect to each is extremely burdensome and could provide another basis for the SEC staff to review performance calculations and fee and expense allocations during exams. We also expect the timing deadlines for the quarter- and year-end statements to present significant operational challenges for sponsors. |

Compliance Date: 18 months (Larger and Smaller Advisers) Existing funds grandfathered? No |

|

Private Fund Audit Rule: Registered advisers must obtain an annual audit for each private fund that meets the requirements of the audit provision in the Advisers Act custody rule (Rule 206(4)-2), and will no longer be able to opt out of the requirement using surprise examinations. |

Many private fund sponsors are already providing audited financial statements in compliance with the custody rule. Sponsors who opt out of this requirement in favor of surprise examinations will be affected. We note that the SEC has re-opened its comment period with respect to its proposal regarding safeguarding client assets to allow commenters to assess its interplay with the Private Fund Audit Rule. |

Compliance Date: 18 months (Larger and Smaller Advisers) Existing funds grandfathered? No |

|

Adviser-Led Secondaries Rule: Registered advisers must obtain and distribute an independent fairness opinion or valuation opinion in connection with an adviser-led secondary transaction, and disclose material business relationships the adviser has had in the last two years with the opinion provider.

|

We believe that a U.S. market norm has likely developed in recent years where many sponsors are already providing fairness opinions or valuation opinions as a best practice in GP-led secondaries. This requirement will, however, increase expenses for transactions that have not historically relied on such opinions (such as where a third-party bid establishes the price), and ultimately such expenses will be passed onto investors. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? No |

|

Books and Records Rule Amendments: Requirement to maintain certain books and records demonstrating compliance with the Final Rules. |

We believe that the books and records amendments generally clarify that sponsors must maintain specific records of compliance with the new rules. We anticipate the SEC staff will focus on this requirement in considering possible deficiencies related to the new rules as part of routine exams. |

Compliance Date: Based on the compliance date of the underlying rule for which records are required Existing funds grandfathered? No |

|

Restricted Activities Rule (Investigation Costs): An adviser may not allocate to the private fund any fees or expenses associated with an investigation of the adviser without disclosing as much and receiving consent from a majority in interest of fund investors (excluding the adviser and its related persons), and is prohibited from charging the fund for fees and expenses for an investigation that results or has resulted in a sanction for a violation of the Advisers Act or the rules thereunder. |

We believe this rule will adversely affect and burden sponsors.[4] Sponsors will no longer be able to allocate costs of an investigation to a fund unless a majority in interest of unaffiliated investors consent. The adopting release makes clear that the SEC intends that sponsors seek separate consents for each investigation, which would suggest that the practice of describing such costs with generality in the fund’s governing document would not be sufficient. Even if sponsors obtain consent to allocate costs related to an investigation to a fund, they will not be able to do so if the investigation results in sanctions for violations of the Advisers Act. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Yes, if disclosed.[5] |

|

Restricted Activities Rule (Regulatory/Compliance Costs): Advisers may not charge or allocate to the private fund regulatory, examination, or compliance fees or expenses unless they are disclosed to investors within 45 days after the end of the fiscal quarter in which such charges occur. |

The adopting release makes clear that the SEC continues to view advisers charging to the fund “manager-level” expenses that it feels should more appropriately be borne by the adviser as “contrary to the public interest and the protection of investors.” As is currently the case, an adviser that allocates its regulatory, compliance and examination costs to a fund should ensure that this practice is clearly permitted under the fund’s governing documents. However, even with such authority, the level of granular disclosure regarding such costs that the Final Rule seemingly requires could have a chilling effect on the practice (where applicable) and discourage investment in compliance. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Disclosure requirement generally applies |

|

Restricted Activities Rule (After-tax Clawback): Advisers may not reduce the amount of a GP clawback by amounts due for certain taxes unless the pre-tax and post-tax amounts of the clawback are disclosed to investors within 45 days after the end of the fiscal quarter in which the clawback occurs. |

Advisers who wish to reduce their GP clawback amount by their actual or hypothetical taxes (the latter being a common practice permitted by most fund governing documents) will need to provide investors with notice of having done so and disclosure of specific dollar amounts. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Yes, with disclosure |

|

Restricted Activities Rule (Non-pro rata investment-level allocations): Advisers may not charge or allocate fees or expenses related to a portfolio investment on a non-pro rata basis when multiple funds and other clients are invested, unless the allocation is “fair and equitable” and the adviser distributes advance notice describing the charge and justifying its fairness and equitability. |

We believe that this requirement will put additional pressure on advisers to determine, at the outset of a fundraise, whether certain costs, such as those related to AIVs or feeder funds set up to accommodate particular investors’ unique tax or regulatory profiles, will be allocated across the fund or instead allocated exclusively to such investors. Increased disclosure will likely lead to more allocation of these costs across the fund. This rule also places additional pressure on the practice of disproportionately allocating broken deal expenses to the fund as opposed to investors who were proposed to have invested alongside the fund, which is a longstanding focus of the SEC. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Disclosure requirement generally applies |

|

Restricted Activities Rule (Borrowing from the fund): Advisers may not borrow or receive an extension of credit from a private fund without disclosure to and consent from fund investors. |

This rule does not apply to the more typical practice of sponsors lending money to the fund. In light of the clarification that disclosure and consent are required, a minority of sponsors may seek to include the ability to borrow from the fund on certain pre-defined terms in the fund’s governing documents. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Yes.[6] |

|

Preferential Treatment Rule (Redemption Rights): An adviser may not offer preferential treatment to investors regarding their ability to redeem if the adviser reasonably expects such terms to have a material, negative effect on other investors, unless such ability is required by law or offered to all other investors in the fund without qualification. |

State pension funds and sovereign wealth funds, in particular, often negotiate special redemption rights. Sponsors are being placed in the difficult position of determining whether such rights have a material, negative effect on other investors, when they are not driven by laws, rules or regulations applicable to the investor. The SEC has provided little guidance to assist in this determination, which must be examined on a case-by-case basis. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Yes.[7] |

|

Preferential Treatment Rule (Portfolio Holdings Information): An adviser may not provide preferential information about portfolio holdings or exposures if the adviser reasonably expects that providing the information would have a material, negative effect on other investors, unless such preferential information is offered to all investors. |

Attention should be given to information required by bespoke reporting templates to determine whether this provision applies. |

Compliance Date: 12 months (Larger Advisers) 18 months (Smaller Advisers Existing funds grandfathered? Yes.[8] |

|

Compliance Rule Amendment: All registered advisers (including those without private fund clients) must document in writing the required annual review of their compliance policies and procedures. |

We believe this codifies an informal position that the SEC examinations staff has already imposed on advisers. |

Compliance Date: 60 days after publication of the Final Rules in the Federal Register Existing funds grandfathered? N/A |

Frequently Asked Questions:

The following Q&A sets forth our answers to questions to frequently asked questions:

| Question: Which of the Final Rules apply to various types of sponsors? |

-

- Registered investment advisers to private funds are subject to all of the rules and restrictions set forth in the table above.

- Exempt reporting advisers and other unregistered advisers are not affected by the Quarterly Statement Rule, the Private Fund Audit Rule, the Adviser-Led Secondaries Rule or the Compliance Rule Amendment.

- Offshore advisers whose principal place of business is outside the U.S., whether registered or unregistered, are technically subject to the Final Rules, but the SEC has indicated that it will not extend the requirements of these rules to the adviser’s activities with respect to their offshore private fund clients, even if the offshore funds have U.S. investors.

- The Final Rule states that Quarterly Statement Rule, Private Fund Audit Rule, Adviser-Led Secondaries Rule, Restricted Activities Rule and Preferential Treatment Rules do not apply to investment advisers with respect to securitized asset funds they advise; real estate funds relying on Section 3(c)(5)(C), and other collective investment vehicles that are not “private funds”[9] are also outside the technical scope of those rules.

- Real estate fund managers that are not registered with the SEC (or filing reports as an exempt reporting adviser) on the basis that they are not advising on “securities” are not subject to the Advisers Act or the Final Rules.

| Question: What do sponsors have to disclose before and after admitting investors, and how will the current MFN process change? |

Sponsors will now have to disclose (i) fee and carry breaks or other material economic arrangements preferentially granted to other investors ahead of admitting new investors into their private funds, and (ii) all preferential treatment as soon as reasonably practicable after the final closing of a closed end fund or the admission of the new investor in an open-end fund, and at least annually thereafter if preferential terms are provided that were not previously disclosed. This disclosure requirement applies to existing funds, even if they have held a final closing prior to the compliance date.

In a statement released concurrently with the release of the Final Rule, Commissioner Caroline A. Crenshaw stated that “collective action problems appear to prevent coordination among investors to bargain for uniform baseline terms.”[10] The SEC’s decision to require disclosure of material economic terms ahead of admitting investors to the fund and disclosure of all preferential treatment post-final closing takes aim at that purported collective action problem.

Notably, the SEC seemingly narrowed its original proposal by opting to require advance written disclosure of “any preferential treatment related to any material economic terms,” as opposed to advance disclosure of all preferential treatment, as originally proposed.[11] Notwithstanding that concession, all preferential treatment (notably, without the materiality qualifier) must invariably be disclosed as soon “as reasonably practicable” following the end of the private fund’s fundraising period (for illiquid funds) or the investor’s investment in the private fund (for liquid funds).[12]

The SEC notes that “as soon as reasonably practicable” will be a facts and circumstances analysis, but suggests that it believes that “it would generally be appropriate for advisers to distribute the notices within four weeks.”[13] We find this proposed timeline ambitious and, in the absence of a hard deadline, would predict that many sponsors will continue take additional time to complete their MFN process. The “as soon as reasonably practicable” requirement would, however, cut against conducting an MFN process an excessive number of months after the final closing, as sometimes happens at present.

Material economic terms that require prior disclosure include, without limitation, “the cost of investing, liquidity rights, fee breaks, and co-investment rights.”[14] The SEC cited excuse rights as an example of non-economic preferential terms which must be disclosed post-closing. Providing a summary of preferential treatment provisions with sufficient specificity to convey its relevance will satisfy this requirement, as will providing the actual provisions granted, and in each case this may be done on an anonymized basis.[15]

In our experience, most investors in private funds with commitments in excess of a certain threshold negotiate side letters with sponsors that contain a “most favored nations” (“MFN”) clause entitling them to view all or part of the side letters granted to other investors and, most frequently, to opt into those more favorable terms negotiated by other investors who make commitments that are equal to or lesser than their capital commitment (and are not otherwise inapplicable to them). This process (the “MFN Process”) typically happens after the fund’s final closing in the closed-end fund context. Accordingly, the Final Rules essentially require sponsors to conduct a portion of their MFN Process in piecemeal fashion, with part of the process conducted prior to the final closing and the rest conducted post final closing, and to do so with respect to each investor regardless of whether such investor negotiated a side letter with an MFN clause or is entitled to elect any of the disclosed provisions. This will curtail the common practice of only showing other investors’ side letter provisions to those investors with MFN provisions and of only showing investors those provisions which they are eligible to elect. Due to the ongoing disclosure requirements, those sponsors of closed-end funds which already held their final closings and ran a more limited MFN process will now be required to disclose any preferential treatment granted to other investors, regardless of size, that had not been previously disclosed. There is no requirement to offer the election of such provisions to the investors who receive the disclosure.

While, as a technical matter, only disclosure of the key terms is required (and not an opportunity to elect such terms), the natural consequence of disclosure is that investors may ask sponsors at the time they are informed of key terms (regardless of whether they have a side letter with an MFN provision) to be granted the same terms as other similarly situated investors.

We expect that these disclosure requirements will present a substantial logistical challenge and may affect previously negotiated commercial arrangements. The SEC has not prescribed a method of delivery for electronic notices, so sponsors will be able to choose whether to do so in the private placement memorandum (the “PPM”), as a standalone disclosure document in an electronic data room, via email or otherwise. PPM supplements may be a natural place to make this disclosure, since private funds typically accept investors across multiple closings over the course of a fundraising and already provide supplements to PPMs, although virtual data rooms may also be an attractive alternative delivery method.

Sponsors will face the issue of how to handle their first closing and how to handle disclosure of terms that are being negotiated concurrently in the final hours before a later closing. In a typical fund closing, multiple side letters are negotiated concurrently with investors in the days leading up to the closing date. Time will tell where the industry lands on this point, but one potential reading of the Final Rules suggests that a sponsor concerned about managing these closing dynamics could take the position that any preferential terms granted as of the same date and at a given closing can be deemed not to have been granted prior to the capital commitments made by any other investor in that closing, and therefore may be disclosed later. It remains to be seen, however, whether this approach is consistent with the intent of the Final Rules and whether, alternatively, the Final Rules would effectively obligate sponsors to communicate two dates to their prospective investors for their closings: one being the “drop dead” date when all side letter terms need to be agreed to, and the second being a later date when commitments will be accepted and the closing will occur. This approach would give the fund, and legal counsel, time to disclose any additional material economic terms to all investors and make any last-minute updates to their side letters in response to any requests to opt into those terms that they are eligible for. In any event, we expect that the Preferential Treatment Rule’s disclosure requirement, assuming it can be practically implemented, will increase organizational expense costs for sponsors. Many sponsors agree to organizational expense caps with their investors, and some are able to negotiate that the MFN Process falls outside of those caps. If at least a portion of the MFN Process, which can be lengthy and expensive, must take place ahead of closing investors, then sponsors are likely to seek increases to their organizational expense caps to accommodate these added costs. The Final Rules will also allow smaller investors, including those that did not themselves negotiate a “most favored nations” clause (or even have a side letter), to view the provisions negotiated by larger investors. This may result in more protracted negotiations with investors who are making capital commitments at sizes which, in the view of sponsors, do not typically entitle them to a side letter arrangement, or to propose in the fund’s PPM fee breakpoints and other means of giving preference based on size, timing and other pre-determined criteria instead of doing so through the side letter process.

| Question: How will sponsors’ quarterly and annual reports be affected? |

Under the Final Rules, registered investment advisers are required to prepare quarterly statements for each of their private funds that include (A) a table with a detailed accounting of all fees, compensation and other amounts paid to the adviser or any of its related persons by the fund as well as all other fees and expenses paid by the fund during the relevant reporting period, (B) a table with a detailed accounting of all fees and compensation paid to the adviser or any of its related persons by the fund’s covered portfolio investments and (C) performance measures of the fund for the relevant reporting period.[16] Advisers must comply with the quarterly statement requirement for a new fund once it has had two full fiscal quarters of operating results. The Final Rule goes into granular detail about what information needs to be clearly and prominently disclosed in the quarterly statements, including the methodologies used and assumptions relied upon in the quarterly statement, as further described below.

(A) Quarterly Statement: Fund-Level Fee, Compensation and Expense Disclosure

The Quarterly Statement Rule requires registered investment advisers to disclose on a quarterly basis (1) a detailed accounting of all compensation, fees, and other amounts allocated or paid to the adviser or any of its related persons by the private fund during the reporting period, including, but not limited to, management, advisory, sub-advisory, or similar fees or payments, and performance-based compensation (e.g., carried interest), (2) a detailed accounting of all fees and expenses allocated to or paid by the private fund during the reporting period other than those listed in (1), including, but not limited to, organizational, accounting, legal, administration, audit, tax, due diligence, and travel fees and expenses, and (3) the amount of any offsets or rebates carried forward during the reporting period to subsequent quarterly periods to reduce future payments or allocations to the adviser or its related persons.

The SEC emphasizes in several places throughout its commentary to the Final Rules that there should be separate line items for each category of compensation, fee or expense and that the exclusion of de minimis expenses, the grouping of smaller expenses into broad categories or the labeling of any expenses as miscellaneous is prohibited, which will require significant effort on the part of advisers. Additionally, they advise that to the extent a certain expense could be categorized as either adviser compensation or a fund expense, the Final Rule requires that such payment or allocation be categorized as adviser compensation. For example, if an adviser or its related persons provide consulting, legal or back-office services to a private fund as a permitted expense under the private fund’s governing documents, such amounts should be categorized as compensation as opposed to an expense. This highlights the technicalities that the Final Rule imposes upon advisers and the potential pitfalls that may arise in compliance.

The SEC also noted in its commentary that the definitions of “related person” and “control” adopted under the Final Rules are consistent with the definitions used on Form ADV and Form PF, which registered investment advisers are familiar with.

This set of disclosure must be done before and after the application of any offsets, rebates or waivers to fees or compensation received by the adviser, including, but not limited to, any fees an adviser or its related person receives for management services provided to a fund’s portfolio company.

(B) Quarterly Statement: Portfolio Investment-Level Fee and Compensation Disclosure

Similar to the above, the Quarterly Statement Rule requires registered investment advisers to disclose a detailed accounting of all portfolio investment compensation allocated or paid by each covered portfolio investment during the reporting period in a single, separate table from the disclosure table noted above.

The definition of a portfolio investment is broad and is intended to cover any entity through which a private fund holds an investment, including through holding vehicles, subsidiaries, acquisition vehicles, special purpose vehicles or the like. In its commentary to the Final Rules, the SEC recognizes that this may impose challenges specifically for funds of funds, as it may be difficult to determine portfolio investment compensation arrangements at the underlying fund level.

This prong of the Final Rule also similarly requires a detailed line-by-line itemization of all portfolio investment compensation. Additionally, the SEC also notes in its commentary to the Final Rules that advisers are required to list the portfolio investment compensation allocated or paid with respect to each covered portfolio investment both before and after the application of any offsets, rebates or waivers. However, it is not clear how this is intended to apply at this level, as such offsets are taken into account at the fund level, not the portfolio company level.

“Portfolio investment compensation” includes any compensation, fees, and other amounts allocated or paid to the adviser or any of its related persons by the portfolio investment attributable to the private fund’s interest in the portfolio investment, including, but not limited to, origination, management, consulting, monitoring, servicing, transaction, administrative, advisory, closing, disposition, directors, trustees or similar fees or payments. Notably, this requirement could cause some sponsors to consider transitioning in-house or affiliated operating groups to unaffiliated entities (e.g., owned by the operating advisors themselves).

(C) Quarterly Statement: Performance Disclosure

Under the Final Rule, registered investment advisers are required to provide standardized fund performance information in each quarterly statement. The performance metrics shown will depend on whether a private fund is classified as a liquid fund or an illiquid fund. An “illiquid fund” is defined as a private fund that does not have investor redemption mechanisms and that has limited opportunities for investor withdrawal other than in exceptional circumstances. A “liquid fund” is defined as a private fund that is not an illiquid fund.

(1) Liquid Funds

For liquid funds, registered investment advisers are required to show performance based on (A) annual net total return for each fiscal year for the 10 fiscal years prior to the quarterly statement or since inception (whichever is shorter), (B) average annual net total returns over one-, five-, and 10-fiscal year periods, and (C) cumulative net total return for the current fiscal year as of the end of the most recent fiscal quarter. It is anticipated that estimations may need to be made for liquid funds that have been operating for lengthy periods of time that did not keep adequate records of the earlier years.

(2) Illiquid Funds

For illiquid funds, registered investment advisers of illiquid funds are required to (i) show performance based on internal rates of return and multiples of invested capital (both gross and net metrics shown with equal prominence) (A) since inception and (B) for the realized and unrealized portions of the illiquid fund’s portfolio, with the realized and unrealized performance shown separately and (ii) present a statement of contributions and distributions. The Final Rule defines the terms “internal rate of return” and “multiple of invested capital”, on both a gross and net basis, and provides color on what is expected to be included in the statement of contributions and distributions.[17] This illustrates the granular and prescriptive nature of the Final Rule, which will require concerted effort on behalf of fund sponsors to ensure compliance.

Advisers are required to consider the impact of fund-level subscription facilities on returns and disclose such performance information for illiquid funds on both a levered and an unlevered basis. In its commentary to the Final Rules, the SEC is repeatedly focused on standardizing information across private funds as much as possible, and as such has provided no room for exclusions to this rule, such as possibly exempting advisers from providing unlevered returns on short-term subscription facilities or excluding subscription line fees and expenses from the calculation of net performance figures.

The SEC notes in its commentary to the Final Rules that to the extent that certain funds rely on information from portfolio investments to generate the required performance data and such information is not available prior to the distribution of the quarterly statement, an adviser would be expected to use the performance measures “through the most recent practicable date”, which is likely the end of the immediately preceding quarter.

An additional prong to the quarterly statement rule is to include clear and prominent disclosure of the methodologies and assumptions made in calculating performance information. This includes, but is not limited to, whether dividends were reinvested in a liquid fund, or whether any fee rates or fee discounts were assumed in the calculation of net performance measures.

This Final Rule also requires the quarterly statement to include cross-references to the sections of the private fund’s organizational and offering documents that set forth the applicable calculation methodology for all expenses, payments, allocations, rebates, waivers, and offsets. This will likely result in significant changes to how private placement memoranda and the operating agreements of private funds are drafted going forward. Furthermore, to the extent that the allocation and methodology provisions in existing operating agreements are not adequately detailed, this requirement under the Final Rule may prompt future LPA amendments that require limited partner consent.

This consequence of the Final Rules is in tension with the legacy status (i.e. grandfathering) that the Final Rules afford governing agreements entered into prior to the date that the Final Rules take effect. The cross-reference requirement of the Quarterly Statement Rule may effectively eliminate the protections provided by the legacy status concept if sponsors will be required to amend their governing agreements to include sufficient allocation and methodology provisions according to the SEC’s new standards. Notwithstanding the fact that many sponsors may already disclose some of the information required under the Quarterly Statement Rule to their investors, it is anticipated that compliance with the Quarterly Statement Rule will result in significant increased cost to advisers and funds, especially at the outset in establishing compliant quarterly statement templates and disclosures.

Such disclosures must be included in the quarterly statement itself as opposed to in a separate document. The SEC noted that while advisers are not required to provide all supporting calculations in quarterly statements, such information should be made available to investors upon request.

With regards to timing, the Final Rule mandates that registered investment advisers must distribute the quarterly statements to the private fund’s investors within 45 days after the end of the first three fiscal quarters of each fiscal year and within 90 days after the end of each fiscal year, and in the case of fund of funds, within 75 days after the end of the first three fiscal quarters of each fiscal year and within 120 days after the end of each fiscal year.

| Question: Which of the Proposed Rules were not adopted or were modified by the Final Rules? |

While the Final Rules will require sponsors to provide investors with significantly more “transparency” regarding preferential economic arrangements granted in side letters (notably, with respect to material economic terms, before closing new investors into their funds) and fees received by the adviser and related persons, as well as providing new rules on quarterly statements, fund audits, adviser-led secondaries, books and records, annual compliance reviews and certain restricted activities, and some of the “disclose and consent” requirements may operate in practical effect as prohibitions on the relevant conduct, it is worth noting that the Final Rules do not specifically adopt the following items which had been set forth in the Proposed Rules.

In particular, the Final Rules do not:

(i) require all preferential rights granted by side letter to be disclosed prior to investment (only material economic terms must be disclosed prior, the rest must be disclosed later);

(ii) eliminate sponsors’ ability to be indemnified, or limit liability, for simple negligence (preserving the “gross negligence” standard for indemnification);

(iii) prohibit clawbacks of carried interest net of taxes (as noted above, this was replaced by a disclosure requirement);

(iv) expressly prohibit allocating portfolio investment fees and expenses to funds on a non-pro rata basis, subject to disclosure requirements; or

(v) prohibit borrowing from a fund (which may done with disclosure and consent).

Further, the Final Rules also do not provide the specific prohibition against charging accelerated monitoring fees that was noted in the Proposed Rules; although members of the SEC staff clarified during the open meeting held on the Final Rules on August 23, 2023 (the “Open Meeting”) that they did not feel specific language on accelerated monitoring fees was necessary because they believe such fees are already prohibited under applicable guidance. The Final Rules also do not expressly prohibit charging an adviser’s regulatory, compliance, examination and certain investigation costs to the fund (except, in some cases, with consent and disclosure and excluding those investigations that result from a violation of the Advisers Act). Our view, however, is that the SEC’s consistent messaging on the impropriety of such charges, combined with burdensome disclosure requirements, could function as a de-facto prohibition of such charges.

___________________________

[1] Resources:

– Link to the Final Rule and the Adopting Release (Release No. IA-6383; File No. S7-03-22 , RIN 3235-AN07, 17 CFR Part 275, Private Fund Advisers; Documentation of Registered Investment Adviser Compliance Reviews: Final Rule)

– Link to the SEC’s Fact Sheet concerning Final Rules

[2] For purposes of the compliance date, the SEC recognized that smaller advisers will require more time to implement certain rules and provided size-based deadlines for implementation, which will be staggered starting from the publication of the Final Rule in the Federal Register. “Larger Advisers” means advisers with assets under management attributable to private funds (“Private Funds AUM”) of $1.5 billion or more. “Smaller Advisers” means advisers with Private Funds AUM of less than $1.5 billion.

[3] The Final Rules grandfather in certain existing arrangements if the private fund has “commenced operations” and has made contractual arrangements related to the provision that were entered into prior to the compliance date, and if the Final Rules would require amending such agreements.

[4] Note that the term “investigation” does not appear to include examinations of the adviser, which are addressed in the row immediately below.

[5] Except that costs associated with investigations resulting in Advisers Act sanctions may not be allocated to new or existing funds even with disclosure and consent.

[6] For loan agreements entered into prior to the compliance date if compliance would require an amendment to such agreements

[7] With respect to contractual obligations entered into prior to the compliance date.

[8] With respect to contractual obligations entered into prior to the compliance date.

[9] Issuers that would be investment companies but for the exclusions contained in Section 3(c)(1) or 3(c)(7) of the Investment Company Act of 1940.

[10] “Statement Regarding Private Fund Adviser Rulemaking”, Aug. 23, 2023, Commissioner Caroline A. Crenshaw (https://www.sec.gov/news/statement/crenshaw-statement-private-fund-advisers-082323?utm_medium=email&utm_source=govdelivery)

[11] Release, page 292.

[12] Release, page 294.

[13] Release, page 299.

[14] Id.

[15] Id at 297.

[16] 17 C.F.R. § 275.211(h)(1)-2(b)-(c).

[17] See 17 C.F.R. § 275.211(h)(1)-1. “Multiple of invested capital” means (i) the sum of: (A) the unrealized value of the illiquid fund; and (B) the value of distributions made by the illiquid fund; (ii) divided by the total capital contributed to the illiquid fund by its investors. “Internal rate of return” means the discount rate that causes the net present value of all cash flows throughout the life of the private fund to be equal to zero. Gross metrics are calculated gross of all fees, expenses and performance-based compensation borne by the private fund, whereas net metrics are calculated net of all fees, expenses and performance-based compensation borne by the private fund.

Gibson Dunn’s lawyers are available to assist with any questions you may have regarding the issues and considerations discussed above, and we will continue to monitor developments in the coming months. Please contact the Gibson Dunn lawyer with whom you usually work in the firm’s Investment Funds practice group, or any of the individuals listed below:

Investment Funds Group:

Jennifer Bellah Maguire – Los Angeles (+1 213-229-7986, [email protected])

Kevin Bettsteller – Los Angeles (+1 310-552-8566, [email protected])

Albert S. Cho – Hong Kong (+852 2214 3811, [email protected])

Candice S. Choh – Los Angeles (+1 310-552-8658, [email protected])

John Fadely – Singapore/Hong Kong (+65 6507 3688/+852 2214 3810, [email protected])

A.J. Frey – Washington, D.C./New York (+1 202-887-3793, [email protected])

Shukie Grossman – New York (+1 212-351-2369, [email protected])

James M. Hays – Houston (+1 346-718-6642, [email protected])

Kira Idoko – New York (+1 212-351-3951, [email protected])

Gregory Merz – Washington, D.C. (+1 202-887-3637, [email protected])

Eve Mrozek – New York (+1 212-351-4053, [email protected])

Roger D. Singer – New York (+1 212-351-3888, [email protected])

Edward D. Sopher – New York (+1 212-351-3918, [email protected])

William Thomas, Jr. – Washington, D.C. (+1 202-887-3735, [email protected])

Tax Group:

Pamela Lawrence Endreny – New York (+1 212-351-2474, [email protected])

Brian W. Kniesly – New York (+1 212-351-2379, [email protected])

Daniel A. Zygielbaum – Washington, D.C. (+1 202-887-3768, [email protected])

The following Gibson Dunn attorneys assisted in preparing this client update: Kevin Bettsteller, Shannon Errico, Greg Merz, and Rachel Spinka.

© 2023 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

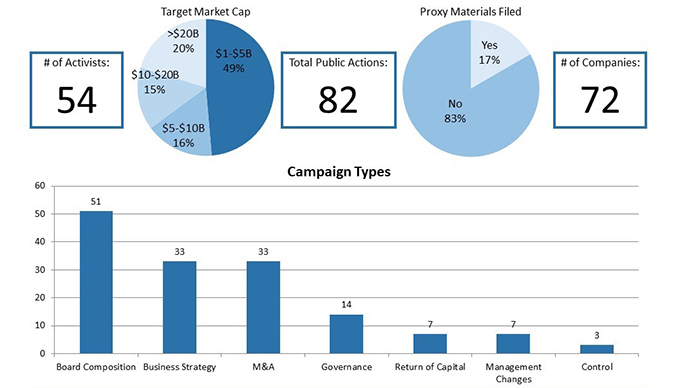

This Client Alert provides an update on shareholder activism activity involving NYSE- and Nasdaq-listed companies with equity market capitalizations in excess of $1 billion and below $100 billion (as of the last date of trading in 2022) during 2022.

Announced shareholder activist activity increased relative to 2021. The number of public activist actions (82 vs. 76), activist investors taking actions (54 vs. 48) and companies targeted by such actions (72 vs. 69) each increased. The period spanning January 1, 2022 to December 31, 2022 also saw several campaigns by multiple activists targeting a single company, such as the campaigns involving: Alphabet Inc. that included activity by NorthStar Asset Management and Trillium Asset Management; C.H. Robinson Worldwide, Inc. that included Ancora Advisors and Pacific Point Wealth Management; and SpartanNash Company that included Ancora Advisors and Macellum Advisors. In addition, certain activists launched multiple campaigns during 2022, including Ancora Advisors, Carl Icahn, Elliott Investment Management, Engine Capital, JANA Partners, Land & Buildings, Starboard Value and Third Point Partners, which each launched three or more campaigns in 2022 and collectively accounted for 32 out of the 82 activist actions reviewed, or 39% in total. Proxy solicitation occurred in 17% of campaigns in 2022—a slight decrease from the amount of solicitations in 2021 (18%).

By the Numbers—2022 Public Activism Trends

*Study covers selected activist campaigns involving NYSE- and Nasdaq-listed companies with equity market capitalizations of greater than $1 billion as of December 31, 2022 (unless company is no longer listed), and all information is derived from publicly available sources

**Ownership is highest reported ownership since the public action date and includes economic exposure to derivatives where applicable.

Additional statistical analyses may be found in the complete Activism Update linked below.

Notwithstanding the increase in activism levels, the rationales for activist campaigns during 2022 were generally consistent with those undertaken in 2021. Over both periods, board composition and business strategy represented leading rationales animating shareholder activism campaigns, representing 63% and 39% of rationales in 2022 and 58% and 34% of rationales in 2021, respectively. M&A (which includes advocacy for or against spin-offs, acquisitions and sales) increased in importance relative to 2021, as the frequency with which M&A animated activist campaigns was 40% in 2022 and 33% in 2021. At the opposite end of the spectrum, management changes, return of capital and control remained the most infrequently cited rationales for activist campaigns, as was also the case in 2021. (Note that the above-referenced percentages total over 100%, as certain activist campaigns had multiple rationales.)

23 settlement agreements pertaining to shareholder activism activity were filed during 2022, which is an increase from the 17 filed in 2021. Those settlement agreements that were filed had many of the same features noted in prior reviews, including voting agreements and standstill periods as well as non-disparagement covenants and minimum-share ownership and/or maximum-share ownership covenants. Expense reimbursement provisions were included in less than half of those agreements reviewed, which is a decrease from previous years. We delve further into the data and the details in the latter half of this Client Alert.

We hope you find Gibson Dunn’s 2022 Annual Activism Update informative. If you have any questions, please reach out to a member of your Gibson Dunn team.

The following Gibson Dunn lawyers prepared this client alert: Barbara Becker, Richard Birns, Dennis Friedman, Andrew Kaplan, Saee Muzumdar, Kristen Poole, Daniel Alterbaum, and Joey Herman.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding the issues discussed in this publication. For further information, please contact the Gibson Dunn lawyer with whom you usually work, or any of the following practice leaders, members, and authors:

Barbara L. Becker (+1 212.351.4062, [email protected])

Dennis J. Friedman (+1 212.351.3900, [email protected])

Richard J. Birns (+1 212.351.4032, [email protected])

Andrew Kaplan (+1 212.351.4064, [email protected])

Daniel S. Alterbaum (+1 212.351.4084, [email protected])

Kristen P. Poole (+1 212.351.2614, [email protected])

Joey Herman (+1 212.351.2402, [email protected])

Mergers and Acquisitions Group:

Robert B. Little – Dallas (+1 214-698-3260, [email protected])

Saee Muzumdar – New York (+1 212-351-3966, [email protected])

Securities Regulation and Corporate Governance Group:

Elizabeth Ising – Washington, D.C. (+1 202.955.8287, [email protected])

Brian J. Lane – Washington, D.C. (+1 202.887.3646, [email protected])

James J. Moloney – Orange County, CA (+1 949.451.4343, [email protected])

Ronald O. Mueller – Washington, D.C. (+1 202.955.8671, [email protected])

Lori Zyskowski – New York (+1 212.351.2309, [email protected])

© 2023 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.

Gibson Dunn’s Public Policy Practice Group is closely monitoring the debate in Congress over potential oversight of artificial intelligence (AI). We have previously summarized major federal legislative efforts and White House initiatives regarding AI in our May 19, 2023 alert Federal Policymakers’ Recent Actions Seek to Regulate AI. We have also covered two U.S. Senate hearings that focused on AI in our June 6, 2023 alert “Oversight of AI: Rules for Artificial Intelligence” and “Artificial Intelligence in Government” Hearings.

On July 25, 2023, the Senate Judiciary Committee’s Subcommittee on Privacy, Technology, and the Law held the second in a series of “Oversight of AI” hearings, following its May 16, 2023 hearing on “Rules for Artificial Intelligence,” with a focus on “Principles for Regulation.”[1] A bipartisan group of Senators, led by Chair Richard Blumenthal (D-CT) and Ranking Member Josh Hawley (R-MO), emphasized the urgent need for AI legislation in the face of rapidly advancing AI technology, including generative algorithms and large language models (LLMs).

Witnesses included:

- Stuart Russell, Professor of Computer Science, The University of California – Berkeley;

- Yoshua Bengio, Founder and Scientific Director, Mila – Québec AI Institute; and

- Dario Amodei, Chief Executive Officer, Anthropic.

I. Points of Particular Interest from July 25, 2023 Hearing

We provide a full hearing summary and analysis below. Of particular note, however:

- Chair Blumenthal opened the hearing by noting that, when speaking to constituents about AI, the word he heard most often was “scary.” He pointed to the hearing’s witnesses as “provid[ing] objective, fact-based views to reinforce those fears.” Although he recognized these fears as existential threats, Chair Blumenthal continued to emphasize AI’s enormous potential for good and reiterated the need not to stifle innovation and to maintain U.S. leadership in the AI sector.

- Both Chair Blumenthal and Ranking Member Hawley extolled the rare bipartisan support for AI regulation. In particular, Chair Blumenthal and Ranking Member Hawley highlighted their recent introduction of a bill to waive immunity under Section 230 of the Communications Act of 1934 for claims related to generative AI, following the Subcommittee’s May 19 discussion of whether such immunity should apply to actors in the AI sector.[2]

- Senator Amy Klobuchar (D-MN) emphasized the need to act quickly to capitalize on this bipartisan appetite for AI regulation and avoid “decay[ing] into partisanship and inaction.”

- Ranking Member Hawley emphasized AI’s potential impact, questioning whether it will be an innovation more like the Internet or the atom bomb. Ranking Member Hawley thought the question facing society, and Congress specifically, is whether Congress will “strike that balance between technological innovation and our ethical and moral responsibility to humanity, to liberty, to the freedom of this country.”

- The subcommittee and its witnesses invoked recent efforts by the White House to secure voluntary commitments from leading AI companies—including Mr. Amodeo’s company, Anthropic—to safeguard against key risks.[3] However, Chair Blumenthal stated that many of these commitments are non-enforceable and relatively unspecific. Chair Blumenthal emphasized that this hearing, in contrast, sought to develop legislation and regulations that would create specific, enforceable obligations on actors in the AI sector.

II. Alleged Risks of Particular Concern

In his opening statement, Ranking Member Hawley commented that he had no doubt that AI will be good for large companies, but that he was less confident that AI would be good for the American people. Much of the hearing, therefore, discussed key areas of risks or alleged harms posed by unregulated AI.

The witnesses testifying before the subcommittee typically divided these risks between immediate or short-term risks that may currently exist in AI—such as privacy concerns, copyright issues, alleged bias in algorithms, and possible misinformation—and more medium-term or long-term risks that may present themselves as AI technology advances. The witnesses emphasized the need for Congress to act urgently to prevent these longer term risks from materializing. Professor Bengio drove home this need, explaining that many AI experts had previously “placed a plausible timeframe for [the] achievement of [human-level AI] somewhere between a few decades and a century” but now considered “a few years to a couple of decades” to be the appropriate estimate.

Throughout the hearing, senators focused on a number of short-term and longer term risks, primarily relating to: (i) misinformation and political influence, (ii) national security, (iii) privacy, and (iv) intellectual property.

a. Misinformation and Political Influence

As in the subcommittee’s previous hearing, concerns about misinformation—particularly in the context of elections—took center stage, with Chair Blumenthal noting that “[i]f there’s nothing else that focuses the attention of Congress, it’s an election.” Both the lawmakers and witnesses highlighted risks associated with “deep fakes” and other forms of misinformation or external influence campaigns using AI.

While Mr. Amadeo noted that his company, Anthropic, trains its AI not to generate misinformation or politically biased content, Ranking Member Hawley pushed back on the idea that AI companies can be trusted to police these lines in the face of business pressures commenting that certain decisions about ethics may be “in the eye of the beholder.” Ranking Member Hawley expressed that, in his view, the control that a relatively small number of companies exercise over the AI sector creates a “serious structural issue” regarding who makes decisions about ethics and misinformation.

Other lawmakers and witnesses echoed Ranking Member Hawley’s concerns about the difficulty of policing AI-generated misinformation, with Senator Klobuchar noting the need to comply with the First Amendment’s protections for free speech and Professor Russell invoking the Orwellian specter of “Ministry of Truth.” Professor Russell proposed, however, that Congress could look to other highly regulated industries like banks and credit cards for guidance on how to balance effective and truthful disclosure requirements with free speech concerns.

b. National Security

Concerns about AI’s implications for national security permeated the hearing, with Ranking Member Hawley listing this issue as one of his top four priorities.

Some of these alleged national security risks related to the use of lethal weapons. For example, Chair Blumenthal noted agreement between the U.S. and China that on limiting certain uses of AI in connection to nuclear weapons, and Professor Russell echoed the popular position against the creation of lethal autonomous weapons systems (LAWS) with the ability to kill in the absence of direction or input from a human actor.

Mr. Amodei specifically addressed concerns that AI could enable malicious actors to develop sophisticated biological weapons. His company had, he explained, conducted a six month study that found that current AI systems are capable of filling in some, but not all, steps in the highly technical process of developing biological weapons. This study extrapolated, however, that AI systems may be able to fill in all steps of these processes within two to three years, allowing malicious actors that lack specialized expertise to weaponize biology.