Los Angeles partners James Zelenay and Nick Hanna and associate Harper Gernet-Girard are the authors of “FCA enforcement, one year into the Biden administration” [PDF] published by the Daily Journal on February 22, 2022.

Washington, D.C. partner Kristen Limarzi is the author of “The FTC’s Efforts to Break Up Facebook Misses Actual Concerns” [PDF] published by Bloomberg Law on February 17, 2022.

Decided February 24, 2022

Unicolors, Inc. v. H&M Hennes & Mauritz, LP., No. 20-915

Today, the Supreme Court held 6-3 that a copyright holder can file a copyright infringement suit even if its copyright registration application included inaccurate information that was the result of an innocent mistake of fact or law.

Background:

A copyright holder cannot bring an infringement suit unless it holds a valid copyright registration certificate. A certificate is valid even if it contains inaccurate information, unless the inaccuracy “was included on the application for copyright registration with knowledge that it was inaccurate” and, “if known, would have caused the Register of Copyrights to refuse registration.” 17 U.S.C. § 411(b). After Unicolors sued H&M for copyright infringement, H&M argued that Unicolors’ copyright registration certificate was invalid because Unicolors had knowingly included inaccurate information in its application by applying to register multiple works in a single application even though it had made those works separately available to clients and the public.

The district court ruled that a certificate is invalid under § 411(b) only if the applicant intended to defraud the Copyright Office, and Unicolors’ mistake of law did not evidence an intent to defraud. The Ninth Circuit reversed, holding that § 411(b) does not contain an intent-to-defraud requirement, and that Unicolors’ application contained factual information Unicolors knew was inaccurate. It was irrelevant, in the Ninth Circuit’s view, whether the inaccuracy was the result of Unicolors’ inadvertent misunderstanding of a principle of copyright law.

Issue:

Whether 17 U.S.C. § 411(b)’s “knowledge” requirement excuses inadvertent mistakes of fact or law.

Court’s Holding:

Yes. The “knowledge” element in § 411(b) requires a showing that the copyright registration applicant actually knew that the inaccurate information in its application was inaccurate, and excuses inaccuracies that were the result of an innocent mistake of fact or law.

“Lack of knowledge of either fact or law can excuse an inaccuracy in a copyright registration.”

Justice Breyer, writing for the Court

What It Means:

- The Court’s decision means that copyright holders can defend inaccuracies in registration certificates on the ground that they were the product of an innocent mistake of either fact or law. The Court’s ruling could provide additional protection for copyright registrants such as novelists, poets, and painters who may be unfamiliar with the complexities of the Copyright Act or who in good faith reach incorrect conclusions about what the law requires.

- Although copyright holders can file new registration applications to fix innocent inaccuracies, copyright claims have a three-year statute of limitations, and statutory damages and attorneys’ fees are available only for infringements that occur after a valid registration is in place. Today’s ruling potentially expands the scope of cases involving inaccurate copyright registrations.

- The Court emphasized that willful blindness to an inaccuracy may constitute actual knowledge under § 411(b), and that circumstantial evidence—such as the significance of the error, the complexity of the relevant rule, and the applicant’s experience with copyright law—could influence whether the applicant was actually aware of, or willfully blind to, the inaccuracy.

The Court’s opinion is available here.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding developments at the Supreme Court. Please feel free to contact the following practice leaders:

Appellate and Constitutional Law Practice

| Allyson N. Ho +1 214.698.3233 aho@gibsondunn.com |

Mark A. Perry +1 202.887.3667 mperry@gibsondunn.com |

Lucas C. Townsend +1 202.887.3731 ltownsend@gibsondunn.com |

| Bradley J. Hamburger +1 213.229.7658 bhamburger@gibsondunn.com |

Related Practice: Intellectual Property

| Howard S. Hogan +1 202.887.3640 hhogan@gibsondunn.com |

Kate Dominguez +1 212.351.2338 kdominguez@gibsondunn.com |

Y. Ernest Hsin +1 415.393.8224 ehsin@gibsondunn.com |

| Josh Krevitt +1 212.351.4000 jkrevitt@gibsondunn.com |

Jane M. Love, Ph.D. +1 212.351.3922 jlove@gibsondunn.com |

Ilissa Samplin +1 213.229.7354 isamplin@gibsondunn.com |

Los Angeles partner Heather Richardson, Orange County associate Jennafer Tryck, and Washington, D.C. associate Tessa Gellerson are the authors of “How Courts Are Ruling On The Arbitrability Of ERISA Claims” [PDF] published by Law360 on February 24, 2022.

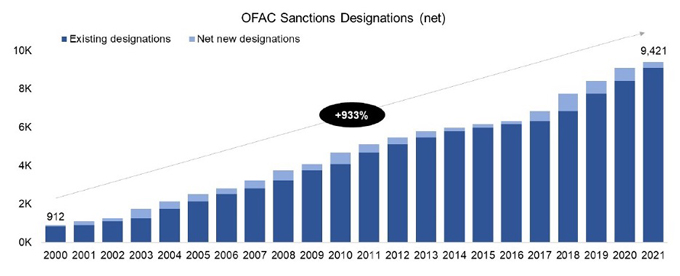

On February 21 and 22, 2022, the United States, the European Union, the United Kingdom, Australia, and Japan issued and/or announced sanctions targeting Russia and the Russia-backed separatist regions of Ukraine known as the Donetsk People’s Republic (“DNR”) and the Luhansk People’s Republic (“LNR”). The United States took the first step by issuing broad jurisdiction-based sanctions on the two regions, similar to the existing sanctions on the Crimea region of Ukraine, and followed up with additional sanctions targeting Russia’s financial system. NATO allies also announced sanctions—including targeted designations by the United Kingdom and a sanctions package by the European Union—and non-NATO allies promised tough sanctions in close coordination. These actions are only among a few of several tools we expect the United States and its allies will use in the coming days and weeks as Russia continues to stoke military tension in the region.

These actions follow nearly a decade of lasting conflict in eastern Ukraine and a quick escalation over the past few weeks. After the 2014 Ukrainian revolution and the Euromaidan movement, which saw a pro-Western government elected in Ukraine, pro-Russia protests against the new government began in eastern Ukraine. These protests in the DNR and LNR regions eventually developed into full-scale fighting, with Russia backing the separatists against the Ukrainian military and more than 10,000 people killed in the conflict. Shaky ceasefires between the two sides have existed for several years, but in recent days, artillery shelling has increased along with other violations of the ceasefire agreements, with the Ukrainian government claiming that these attacks were orchestrated by Russia or pro-Russia separatists in the region.

In response to formal appeals from the de facto leaders of the breakaway regions for sovereign recognition from Russia, Russian president Vladimir Putin convened a meeting of his security council on Monday, February 21, 2022 under the pretext of seeking recommendations on how to answer the requests. After the meeting of the council, Putin delivered a televised address to the public, referring to eastern Ukraine as “historically Russian territory” and saying that it is “necessary to take a long overdue decision to immediately recognize the independence and sovereignty of the Donetsk People’s Republic and the Luhansk People’s Republic.” Immediately thereafter, Putin ordered Russian troops to enter the regions for a “peacekeeping” mission under the treaties of “friendship and mutual assistance” that Russia ratified that same day with the individual regions. All diplomatic efforts to maintain the territorial integrity of Ukraine while the parties sought to ease building tensions thus suffered a serious setback.

US Issues New Executive Order Imposing Sweeping Sanctions on Separatist Regions

Just hours after Putin’s televised speech, President Biden signed a new Executive Order issuing broad sanctions on the DNR and LNR regions of Ukraine, and any other regions of Ukraine as may be determined by the Secretary of the Treasury, in consultation with the Secretary of State (collectively, the “Covered Regions”). The Executive Order is nearly identical to Executive Order 13685 that announced comprehensive sanctions on the Crimea region of Ukraine in 2014.

First, the Executive Order prohibits: (1) new investment in the Covered Regions by a U.S. person; (2) import of any goods, services, or technology from these regions to the United States; and (3) export of any goods, services, or technologies from the United States or by a U.S. person to these regions. The Executive Order further prohibits U.S. persons from financing, facilitating, or guaranteeing transactions by foreign persons that U.S. persons would be prohibited from engaging directly.

Second, the Executive Order authorizes blocking sanctions on any person determined by the Secretary of the Treasury, in consultation with the Secretary of State, to be: (1) a person operating in the Covered Regions; or (2) a leader, official, senior executive officer, or board member of an entity operating in the Covered Regions. The Executive Order also authorizes sanctions on an entity determined to be owned or controlled by a blocked person pursuant to the Executive Order, or any person who has provided material support for a blocked person pursuant to the Executive Order. No such individual designations have yet been made, which is very similar to how OFAC responded at the inception of Executive Order 13685.

Concurrent with the signing of the Executive Order, OFAC issued six general licenses:

- General License 17, “Authorizing the Wind Down of Transactions Involving the So-called Donetsk People’s Republic or Luhansk People’s Republic Regions of Ukraine” authorizes all prohibited transactions “that are ordinarily incident and necessary to the wind down of transactions involving” the Covered Regions until March 23, 2022.

- General License 18, “Authorizing the Exportation or Reexportation of Agricultural Commodities, Medicine, Medical Devices, Replacement Parts and Components, or Software Updates to Certain Regions of Ukraine and Transactions Related to the Coronavirus Disease 2019 (COVID-19) Pandemic” authorizes the export of agricultural commodities, medicine, medical devices, replacement parts and components, or software updates to the Covered Regions. This authorization is similar to that of the existing General License 4 with respect to the Crimea region, but is more expansive in that it does not include the exclusions that are in General License 4 (e.g., export to military or law enforcement purchasers, certain agricultural commodities, and certain medicines), that it expands the scope to software updates in addition to replacement parts, and that it includes a separate COVID-19 authorization.

- General License 19, “Authorizing Transactions Related to Telecommunications and Mail” authorizes transactions that are ordinarily incident and necessary to the receipt or transmission of telecommunications in the Covered Regions. This authorization is similar to the existing General License 8 with respect to the Crimea region.

- General License 20, “Official Business of Certain International Organizations and Entities” authorizes official business of certain international organizations and entities in the Covered Regions. Of note, the list of international organizations includes the Organization for Security and Co-operation in Europe, an entity that has been actively seeking to de-escalate the conflict in recent days.

- General License 21, “Authorizing Noncommercial, Personal Remittances and the Operation of Accounts” authorizes transactions that are ordinarily incident and necessary to the transfer of noncommercial, personal remittances to or from the Covered Regions. This authorization is similar to the existing General License 6 with respect to the Crimea region.

- General License 22, “Authorizing the Exportation of Certain Services and Software Incident to Internet-Based Communications” authorizes export of certain services incident to the exchange of personal communications over the internet or software necessary to enable such services in the Covered Regions. This is similar to the existing General License 9 with respect to the Crimea region, but is more expansive in that it does not require the services and software to be widely available to the public with no cost to the user.

The issuance of these expansive general licenses is in line with the White House’s repeated messaging that the sanctions “are not directed at the people of Ukraine” or “the innocent people who live in the so-called DNR and LNR regions.” Particularly during the COVID-19 pandemic, the Biden administration has continued to include broad humanitarian exceptions in new sanctions measures, including those taken in response to the situations in Myanmar and Ethiopia. It is noteworthy that OFAC further created an expansive COVID-19 authorization for transactions related to the prevention, diagnosis, or treatment of the COVID-19 pandemic, without any specific definition or exception.

General License 17 is also consistent with OFAC’s past practices of allowing parties a period of time to adjust to significant new sanctions measures to minimize the immediate disruption to the global economy. Similar to the more recent wind-down licenses from OFAC, there is no requirement for U.S. persons participating in authorized transactions to file a report with OFAC, which reduces the administrative burden of relying on the license. However, the 30-day wind-down period is much shorter than the typical 60- to 90-day periods that OFAC has granted in announcing other sanctions measures. It is likely that future wind-down licenses from OFAC regarding sanctions targeting Russia will be similarly brief.

Parties planning to rely on these general licenses should note that all six general licenses expressly limit their authorizations to transactions and activities that are prohibited by this particular Executive Order. The general licenses do not authorize transactions with persons or entities designated pursuant to other sanctions programs. As a result, parties should be careful not to engage in transactions and activities that are prohibited under another authority, such as the sectoral sanctions under Executive Order 13662. Parties should also take note of the differences between the general licenses granted with respect to the Crimea sanctions and to the DNR and LNR sanctions, in case a counterparty is sanctioned under both Executive Order 13685 and the new Executive Order.

US Imposes Sanctions on Russian Financial Services Sector

On February 22, 2022, OFAC designated to the SDN List two financial institutions that it determined are crucial to financing the Russian defense industry—Corporation Bank for Development and Foreign Economic Affairs Vnesheconombank (VEB) and Promsvyazbank Public Joint Stock Company (PSB)—along with 42 of their subsidiaries. OFAC also designated three individuals—Denis Aleksandrovich Bortnikov, Petr Mikhailovich Fradkov, and Vladimir Sergeevich Kiriyenko—who OFAC determined were “powerful Russians in Putin’s inner circle.”

All of the designations were made under the authority of the Executive Order 14024, which we discussed in depth in a previous update. Importantly, Executive Order 14024 had authorized blocking sanctions against persons determined to operate in certain sectors of the Russian economy, with specific sectors to be determined by the Secretary of the Treasury, in consultation with the Secretary of State. When Executive Order 14024 was issued in April 2021, OFAC had identified the technology sectors and defense and related materiel sector as potential targets of future designations. In the most recent action taken on February 22, 2022, OFAC additionally identified the financial services sector of the Russian economy, making it easier for the United States to use a single, consolidated sanctions tool to target the entire financial services sector. OFAC accompanied this determination with FAQ 964, noting that its determination merely lays the groundwork for future sanctions against persons that operate in the financial services sector, rather than actually serving as sanctions on the entire financial services sector.

Additionally, OFAC issued Directive 1A, amending and superseding Directive 1 that was issued under Executive 14024. Importantly, Directive 1A includes restrictions on the participation in the secondary market for ruble or non-ruble denominated bonds issued after March 1, 2022 by the Central Bank of the Russian Federation, the National Wealth Fund of the Russian Federation, or the Ministry of Finance of the Russian Federation. As a result of this new Directive 1A, the Central Bank of the Russian Federation, the National Wealth Fund of the Russian Federation, and the Ministry of Finance of the Russian Federation have been designated to the Non-SDN Menu-Based Sanctions List.

Concurrent with these additional sanctions, OFAC issued two general licenses:

- General License 2, “Authorizing Certain Servicing Transactions Involving State Corporation Bank for Development and Foreign Economic Affairs Vnesheconombank” authorizes all prohibited transactions “that are ordinarily incident and necessary to the servicing of bonds issued before March 1, 2022 by the Central Bank of the Russian Federation, the National Wealth Fund of the Russian Federation, or the Ministry of Finance of the Russian Federation,” but to the extent that such transaction is not prohibited by the new Directive 1A.

- General License 3, “Authorizing the Wind Down of Transactions Involving State Corporation Bank for Development and Foreign Economic Affairs Vnesheconombank” authorizes all prohibited transactions “that are ordinarily incident and necessary to the wind down of transactions involving” VEB for a 30-day period until March 24, 2022.

Again, parties planning to rely on these general licenses should note that the general licenses expressly limit their authorizations to transactions and activities that are prohibited by Executive Order 14024.

EU Announces Sanctions Package to be Implemented

The EU has announced, yet not formally issued, new sanctions on Russia. While in the morning of February 22, 2022, the presidents of the European Council and the European Commission had welcomed “the steadfast unity of [EU] Member States and their determination to react with robustness and speed,” the subsequent announcement of the specific contemplated measures was more limited in scope than expected by many and only came after a surprisingly lengthy meeting of EU Foreign Affairs Ministers. The formal issuance and implementation of the contemplated measures is now expected in the course of the week.

First, in what the EU has now referred to as “solid package” of “calibrated measures,” EU financial sanctions (broadly comparable to U.S. SDN designations) will target individuals and entities involved in the violations of international law by the Kremlin, including in the recognition of the Donetsk and Luhansk regions as independent entities.

Second, the EU will target banks that finance the Russian military apparatus and contribute to the destabilization of Ukraine. Such banks have not yet been named and will either be targeted via EU financial sanctions or via more limited EU economic sanctions (broadly comparable to U.S. SSI designations).

Third, the EU has announced that it plans to ban trade between the EU and the Donetsk and Luhansk regions by implementing comprehensive EU Economic Sanctions comparable to those implemented after the annexation by Russia of Crimea in 2014.

Finally, the EU announced new measures to restrain Russian efforts to raise further capital on EU’s financial markets by limiting respective access for the Russian state and government. Such measures will likely take the form of targeted EU Economic Sanctions and prohibit or at least limit dealings with, for example, transferable securities and money-market instruments with a certain maturity and prohibit making loans or credit to those targeted.

The EU also announced that it had prepared and stands ready to adopt additional measures at a later stage if needed in the light of further developments.

Germany Stops Certification of Nord Stream 2

As a first reaction, the German Chancellor Olaf Scholz announced that the certification of the Nord Stream 2 pipeline has been stopped, and thus the pipeline will not become operational until further notice. This action was perhaps the least expected response and carries significant practical impact. The Nord Stream 2 project was intended to supply energy from Russia to the European Union, and Germany—along with other EU member states—had so far contested any attempts to impose sanctions on the Nord Stream 2 project in light of Russian aggression, in part due to the European Union’s heavy reliance on energy sources from Russia. With this action, Germany sent a clear message that it stands ready to join severe sanctions against Russia.

United Kingdom Sanctions Russian Banks and Oligarchs

On February 10, 2022, the UK pre-emptively amended its legislation on Russia sanctions—the Russia (Sanctions) (EU Exit) Regulations 2019 (S.I. 2019/855) (the “UK Russia Sanctions Regulations”)—via the enactment of The Russia (Sanctions) (EU Exit) (Amendment) Regulations 2022 (SI 2022/123) (the “Amended Regulations”).

The Amended Regulations widened the scope of the UK Russia Sanctions Regulations by expanding its designation criteria. The designation criteria now include entities and individuals that are involved in “obtaining a benefit from or supporting the Government of Russia.” Previously, the UK could only impose travels bans or asset freezes on those involved in “destabilising Ukraine or undermining or threatening the territorial integrity, sovereignty or independence of Ukraine.”

For the purposes of the Amended Regulations, being “involved in obtaining a benefit from or supporting the Government of Russia” includes, among other things, carrying on business “of economic significance” or “in a sector of strategic significance” to the Government of Russia, those sectors being the Russian chemicals, construction, defense, electronics, energy, extractives, financial services, information, communications, digital technologies, and transport sectors. This is therefore a very significant expansion in the scope of the designation criteria which empowers the UK to impose sanctions on a wide range of businesses that may not necessarily have a strong nexus to the Russian government, save that the nature of their business and/or the sector(s) in which they operate are of economic significance to the Russian government.

Using its new powers under the Amended Regulations, the UK government updated the UK Sanctions List on February 22, 2022 by designating five Russian banks (Bank Rossiya, Black Sea Bank for Development and Reconstruction, Joint Stock Company Genbank, IS Bank, Public Joint Stock Company Promsvyazbank) as well as three wealthy individuals (Gennadiy Nikolayevich Timchenko, Boris Romanovich Rotenberg and Igor Arkadyevich Rotenberg) as being subject to an asset freeze.

The UK’s Prime Minister, Boris Johnson, has described this sanctions package as “the first tranche, the first barrage“ of what the UK is prepared to do. Foreign Secretary, Liz Truss, said in her statement that “this first wave of sanctions will hit oligarchs and banks close to the Kremlin. It sends a clear message that the UK will use [its] economic heft to inflict pain on Russia and degrade their strategic interests.” She further stated that “in the event of further aggressive acts by Russia against Ukraine,” the UK has prepared “an unprecedented package of further sanctions ready to go. These include a wide-ranging set of measures targeting the Russian financial sector, and trade.” However, for some in the UK, these measures do not go far enough, and Boris Johnson is under pressure to impose tougher sanctions.

Allies Outside NATO Join in Announcing Tough Response

Japan’s Minister of Foreign Affairs Hayashi Yoshimasa stated that Japan would continue to monitor the development of the situation in Ukraine with serious concern and coordinate a tough response, including sanctions in cooperation with the international community.

Australia’s Minister of Foreign Affairs declared that the Australian Government was coordinating closely with the United States, United Kingdom, European Union, and other governments around the world to ensure there were severe costs for Russia’s aggression and that, along with its partners, Australia was prepared to announce swift and severe sanctions that would target key Russian individuals and entities responsible for undermining Ukraine’s sovereignty and territorial integrity.

Possible Next Steps

There has been much speculation in recent days about the sanctions packages that would be revealed upon Russia’s invasion of Ukraine. So far, many world leaders have stopped short of calling Russia’s recognition of the two regions and his deployment of the Russian military to these regions a full-scale invasion, perhaps in part as an effort to deescalate tension or to leave space for additional sanctions if the situation worsens. However, the recent measures allow more authority for the Western countries to issue additional sanctions in case of further escalation—such as a new Executive Order that authorizes sanctions on persons operating in the separatist regions of Ukraine and a financial services sector determination that authorizes sanctions on persons operating in the Russian financial services sector. As tensions continue to rise, we will likely see more series of tools from the NATO countries and their allies to exert economic pressure on Russia to deescalate the ongoing crisis in Ukraine and withdraw its army from Ukraine’s borders. Companies should continue to pay attention to the ongoing developments and proactively assess their exposure to the sanctions and export controls measures being discussed.

In the lead up to the recent sanctions, leaders of the NATO countries engaged in close coordination and dialogue and had reported that they have “wrapped up“ and are “unified“ on potential sanctions packages to be used. However, we have seen varying degrees of severity and speed in the measures that each of the governments were able to impose immediately following the action from Russia. We expect there to be continued effort for coordination and convergence across the various jurisdictions, but we are closely tracking the differences in the sanctions imposed in different jurisdictions and the resulting compliance impact for companies operating in the global market.

The following Gibson Dunn lawyers assisted in preparing this client update: Claire Yi, Jacob A. McGee, Richard Roeder, Julian Reichert, Alexander Stahl, Kanchana Harendran, David A. Wolber, Judith Alison Lee, Adam M. Smith, Christopher Timura, Michael Walther, Benno Schwartz, Patrick Doris, and Attila Borsos.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding the above developments. Please contact the Gibson Dunn lawyer with whom you usually work, the authors, or any of the following leaders and members of the firm’s International Trade practice group:

United States:

Judith Alison Lee – Co-Chair, International Trade Practice, Washington, D.C. (+1 202-887-3591, jalee@gibsondunn.com)

us-and-allies-announce-sanctions-on-russia-and-separatist-regions-of-ukraine

Nicola T. Hanna – Los Angeles (+1 213-229-7269, nhanna@gibsondunn.com)

Marcellus A. McRae – Los Angeles (+1 213-229-7675, mmcrae@gibsondunn.com)

Adam M. Smith – Washington, D.C. (+1 202-887-3547, asmith@gibsondunn.com)

Christopher T. Timura – Washington, D.C. (+1 202-887-3690, ctimura@gibsondunn.com)

Courtney M. Brown – Washington, D.C. (+1 202-955-8685, cmbrown@gibsondunn.com)

Laura R. Cole – Washington, D.C. (+1 202-887-3787, lcole@gibsondunn.com)

Chris R. Mullen – Washington, D.C. (+1 202-955-8250, cmullen@gibsondunn.com)

Samantha Sewall – Washington, D.C. (+1 202-887-3509, ssewall@gibsondunn.com)

Audi K. Syarief – Washington, D.C. (+1 202-955-8266, asyarief@gibsondunn.com)

Scott R. Toussaint – Washington, D.C. (+1 202-887-3588, stoussaint@gibsondunn.com)

Shuo (Josh) Zhang – Washington, D.C. (+1 202-955-8270, szhang@gibsondunn.com)

Asia:

Kelly Austin – Hong Kong (+852 2214 3788, kaustin@gibsondunn.com)

David A. Wolber – Hong Kong (+852 2214 3764, dwolber@gibsondunn.com)

Fang Xue – Beijing (+86 10 6502 8687, fxue@gibsondunn.com)

Qi Yue – Beijing – (+86 10 6502 8534, qyue@gibsondunn.com)

Europe:

Attila Borsos – Brussels (+32 2 554 72 10, aborsos@gibsondunn.com)

Nicolas Autet – Paris (+33 1 56 43 13 00, nautet@gibsondunn.com)

Susy Bullock – London (+44 (0) 20 7071 4283, sbullock@gibsondunn.com)

Patrick Doris – London (+44 (0) 207 071 4276, pdoris@gibsondunn.com)

Sacha Harber-Kelly – London (+44 (0) 20 7071 4205, sharber-kelly@gibsondunn.com)

Penny Madden – London (+44 (0) 20 7071 4226, pmadden@gibsondunn.com)

Matt Aleksic – London (+44 (0) 20 7071 4042, maleksic@gibsondunn.com)

Benno Schwarz – Munich (+49 89 189 33 110, bschwarz@gibsondunn.com)

Michael Walther – Munich (+49 89 189 33 180, mwalther@gibsondunn.com)

Richard W. Roeder – Munich (+49 89 189 33 115, rroeder@gibsondunn.com)

© 2022 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

This past year was another busy one for Employee Retirement Income Security Act (“ERISA”) litigation, including significant decisions from the United States Supreme Court and the federal courts of appeals on issues impacting retirement and healthcare plans, coupled with the change in presidential administrations that resulted in new rules affecting ERISA plan sponsors and administrators.

Last year, Gibson Dunn also welcomed back Eugene Scalia as a partner to the Firm’s Washington, DC office after he served as the 28th U.S. Secretary of Labor from September 2019 to January 2021. Scalia’s return adds further depth to Gibson Dunn’s bench of elite ERISA litigators, who take an interdisciplinary approach to their work resolving complex matters for our clients, and bring together the Firm’s deep knowledge base and significant experience from across a variety of its award-winning practice groups, including: Executive Compensation & Employee Benefits, Class Actions, Labor & Employment, Securities Litigation, FDA & Health Care, and Appellate & Constitutional Law.

This year’s Annual ERISA Litigation Update summarizes key legal opinions and developments to assist plan sponsors and administrators navigating the rapidly changing ERISA litigation landscape.

Section I highlights two notable opinions from the United States Supreme Court rejecting a challenge to the individual mandate in the Affordable Care Act on standing grounds, and addressing the pleading standard in ERISA “excessive fee” fiduciary-breach cases. We are also watching pending petitions for certiorari concerning the application of ERISA’s fiduciary requirements to business transactions between plan administrators and third-party service providers, and ERISA preemption of state-run IRA programs for private-sector workers.

Section II delves into how the federal courts have applied the Supreme Court’s decision in Thole v. U.S. Bank, 140 S. Ct. 1615 (2020), addressing Article III standing in ERISA cases. We also discuss the implications for ERISA litigants of the Court’s recent decision on Article III standing in TransUnion LLC v. Ramirez, 141 S. Ct. 2190 (2021).

Section III addresses the continuing impact of the Supreme Court’s decision in Rutledge v. Pharmaceutical Management Association, 141 S. Ct. 474 (2020), on the issue of ERISA preemption.

Section IV provides an analysis of how the federal courts are assessing the enforceability of arbitration agreements in ERISA plans.

Section V discusses how the courts continue to grapple with the standard of review for ERISA benefits claims.

Section VI offers an overview of the Department of Labor’s rule changes concerning environmental, social, and governmental (“ESG”) investing, and the implications of those changes for ERISA plan fiduciaries.

I. Key 2021 Supreme Court Decisions & Cases to Watch

The United States Supreme Court decided two cases in 2021 with significant implications for ERISA plans and their sponsors and administrators. In California v. Texas, 141 S. Ct. 2104 (2021), the Court dismissed a challenge to the Affordable Care Act (“ACA”) by holding that the plaintiffs lacked Article III standing to bring the suit. In Hughes v. Northwestern University, the Court held that allegations that a defined-contribution retirement plan breached ERISA’s duty of prudence by offering high-cost investment options may be actionable even if the plan also offers lower-cost options. But the Court declined to adopt an ERISA-specific pleading standard for these fiduciary-breach claims.

The Court has also ordered further briefing on pending petitions for certiorari in ERISA cases concerning the application of ERISA’s fiduciary requirements to arms-length contracts between a plan administrator and third-party service providers, and the scope of ERISA preemption over state-run programs that enroll private sector employees in retirement savings programs.

A. California et al. v. Texas et al. and Texas et al. v. California et al. Uphold the Affordable Care Act

In California v. Texas, 141 S. Ct. 2104 (2021) (consolidated with Texas v. California), the Supreme Court rejected on Article III standing grounds the latest challenge to the constitutionality of the ACA. In 2012, the Court rejected constitutional challenges under the Commerce Clause to the requirement in the ACA that individuals must maintain health insurance coverage, also known as the individual mandate. Nat’l Fed’n of Indep. Bus. v. Sebelius, 567 U.S. 519 (2012). The Court reasoned that the ACA was not a command to buy health insurance—which Congress would lack the power to enact—but merely a tax for not doing so. Id. at 574–75.

In December 2017, Congress amended the ACA to eliminate the penalty for not buying health insurance, but did not eliminate the ACA’s individual mandate. Two individuals and several states, including Texas, then challenged the individual mandate as unconstitutional, arguing that because it no longer carried a penalty, it no longer qualified as a tax. They also argued that because the individual mandate is essential to the ACA, the entire statute must be struck down. When the Trump Administration declined to defend the ACA’s constitutionality, several states, including California, intervened to defend the statute and challenge the plaintiffs’ Article III standing. The Fifth Circuit held that the plaintiffs possessed standing and held that the individual mandate is unconstitutional. Texas v. United States, 945 F.3d 355, 377–93 (5th Cir. 2019), as revised (Dec. 20, 2019), as revised (Jan. 9, 2020), rev’d and remanded sub nom. California v. Texas, 141 S. Ct. 2104 (2021).

The Supreme Court reversed, holding that neither the individual plaintiffs nor the plaintiff states had Article III standing to challenge the individual mandate. See California, 141 S. Ct. at 2114–2116. The individual plaintiffs claimed that they satisfied the standing requirements because of the payments they have made and will continue to make to carry the minimum essential coverage that the ACA requires. But the Court reasoned that even if payments necessary to hold the insurance coverage required by the ACA were an injury, that injury would not be traceable to the government, because without any penalty for noncompliance, the statute is unenforceable against the individual plaintiffs. Id.

The Court likewise concluded that the states did not have Article III standing because they failed to show that their injuries were fairly traceable to unlawful government conduct. Id. at 2116. The states claimed they were indirectly injured by the mandate because it would cause more people to enroll in Medicaid or state employee health insurance programs. But the states failed to demonstrate “that an unenforceable mandate will cause their residents to enroll in valuable benefits programs that they would otherwise forgo.” Id. at 2119. Texas also asserted that it would bear increased direct costs because of ACA reporting and administrative requirements, but the Court found that these costs were not caused by the mandate and would remain even if it were struck down. Id. at 2119–20.

Justice Alito, joined by Justice Gorsuch, dissented, concluding instead that (1) the state plaintiffs possess standing in light of the increased regulatory and financial burdens from complying with the ACA, and they did not forfeit these claims, and (2) the individual mandate is unconstitutional and not severable from the rest of the ACA. Id. at 2124 (Alito, J., dissenting).

The decision is a significant one for ERISA because it eliminates, for now, some of the uncertainty around the validity of the ACA, including the ACA’s ERISA-specific requirements such as the large employer health insurance mandate. But the decision leaves unresolved the merits questions presented in the case—i.e., whether the individual mandate is constitutional or whether it is severable from the rest of the ACA—which the Court may be asked to revisit in future cases.

B. Hughes v. Northwestern University Addresses Pleading Standard in ERISA Fiduciary-Breach Suits

In Hughes v. Northwestern University, the Supreme Court reiterated in an unanimous decision that a district court’s review of a pleading challenge in an ERISA “excessive fees” fiduciary breach suit is a context-specific inquiry that requires courts to assess whether plaintiffs plausibly allege—under Ashcroft v. Iqbal, 556 U.S. 662 (2009) and Bell Atlantic Corp. v. Twombly, 550 U.S. 544 (2007)—that plan fiduciaries failed to monitor all plan investments and remove imprudent ones.

Northwestern University offered its employees defined-contribution retirement plans, in which the employees maintain individual investment accounts and choose how to invest their contributions. Hughes v. Nw. Univ., 142 S. Ct. 737, 740 (2022). Former and current employees of Northwestern alleged that the plans’ fiduciaries violated the duty of prudence under ERISA by providing employees with a menu of investment options that included allegedly high cost and poorly performing options that caused plan participants to incur excessive fees. Id. at 741. The plans also included the types of low-fee options that plaintiffs preferred. Id. at 741–42.

The Seventh Circuit affirmed the dismissal of petitioners’ claims for failure to plausibly allege a breach of fiduciary duty. Divane v. Nw. Univ., 953 F.3d 980, 993 (7th Cir. 2020). The court held in relevant part that Northwestern had complied with its duty of prudence by offering a menu of investment options that included low-cost funds, along with the other higher-cost options challenged in the complaint. Id. at 991–92.

Relying on Tibble v. Edison Int’l, 575 U.S. 523 (2015), the Supreme Court reversed, holding that the Seventh Circuit erred in dismissing the plaintiffs’ claims without making a “context-specific inquiry” that “take[s] into account [a fiduciary’s] duty to monitor all plan investments and remove any imprudent ones.” Hughes, 142 S. Ct. at 740. The Supreme Court reasoned:

[E]ven in a defined-contribution plan where participants choose their investments, plan fiduciaries are required to conduct their own independent evaluation to determine which investments may be prudently included in the plan’s menu of options. . . . If the fiduciaries fail to remove an imprudent investment from the plan within a reasonable time, they breach their duty.

Id. at 742 (citing Tibble, 575 U.S. at 529–30). The Court remanded the case to the Seventh Circuit so that it could “reevaluate the allegations as a whole” and “consider whether petitioners have plausibly alleged a violation of the duty of prudence as articulated in Tibble, applying the pleading standard discussed” in Iqbal and Twombly. Id. Under that standard, plaintiffs must plead “enough facts to state a claim to relief that is plausible on its face.” Twombly, 550 U.S. at 570; see also Iqbal, 556 U.S. at 679 (allegations must “permit the court to infer more than the mere possibility of misconduct”). The Court concluded its opinion by addressing the importance of affording deference to plan fiduciaries, stating: “At times, the circumstances facing an ERISA fiduciary will implicate difficult tradeoffs, and courts must give due regard to the range of reasonable judgments a fiduciary may make based on her experience and expertise.” Hughes, 142 S. Ct. at 742.

Ultimately, the Court’s decision in Hughes was narrow. It did not establish a new pleading standard for ERISA fiduciary-breach claims, as petitioners had sought, nor did it set out the specific allegations that would be sufficient to plead a claim under plaintiffs’ fiduciary-breach theories. It is thus left to be seen whether this decision will pave the way for more “excessive fee” suits, whether the district courts will rely on Hughes to permit more cases to proceed to discovery, or whether the Supreme Court’s guidance concerning deference to plan fiduciaries will prompt courts to find that allegations that other investment options were theoretically available at a lower cost are not alone enough to withstand a pleading challenge.

C. Supreme Court Petitions to Watch

We are also monitoring three pending petitions for certiorari implicating ERISA issues. John Doe 1 v. Express Scripts Inc. (No. 21-471) and OptumHealth Care Solutions LLC v. Peters (No. 21-761) address the application of ERISA’s fiduciary requirements to arms-length transactions between a plan administrator and a third-party that provides services to a plan. Howard Jarvis Taxpayers Association v. CA Secure Choice Retirement Program (No. 21-558), concerns whether California’s auto-IRA program, which enrolls private-sector employees in a state-run retirement savings program, is preempted by ERISA.

1. John Doe 1 v. Express Scripts Inc. (No. 21-471)

In John Doe 1 v. Express Scripts Inc., health insurance policyholders seek to revive a proposed class action accusing Anthem and Express Scripts of violating fiduciary duties under ERISA by entering into a self-interested contractual arrangement that resulted in the plans and participants paying above-market prices for prescription drugs. The case arose from Anthem’s decision, as administrator of self-insured ERISA health plans, to sell its in-house pharmacy benefit management business to Express Scripts. Plaintiffs allege that in exchange for a substantially higher purchase price for the business, Anthem agreed to delegate to Express Scripts discretion to set the drug prices charged to Anthem customers, including prices that plaintiffs claim far exceeded industry standards.

Plaintiffs petitioned the Supreme Court to hear the case after the Second Circuit affirmed dismissal, holding that Anthem and Express Scripts were not acting as fiduciaries under ERISA when executing and acting upon the drug pricing contract. See Doe 1 v. Express Scripts, Inc., 837 F. App’x 44 (2d Cir. 2020). The Second Circuit relied in part on the Sixth Circuit’s decision in DeLuca v. Blue Cross Blue Shield of Mich., which held that an insurer did “not act[ ] as a fiduciary when it negotiated” rate changes for certain medical services, “principally because those business dealings were not directly associated with the benefits plan at issue but were generally applicable to a broad range of health-care consumers.” 628 F.3d 743, 747 (6th Cir. 2010). As to Anthem, the court explained that even if Anthem’s decisions “may ultimately affect how much plan participants pay for drug prices,” they were business dealings not directly associated with the plans they may ultimately have affected. Doe 1, 837 F. App’x at 49. The Second Circuit also agreed with the district court that Express Scripts did not act as a fiduciary when it set prices for prescription drugs, even though it had “extraordinarily broad discretion,” because “at bottom the ability to set such prices is a contractual term, not an ability to exercise authority over plan assets.” Id.

Plaintiffs petitioned for certiorari, contending that the Second and Sixth Circuit decisions had established an invalid, extra-statutory “business decisions” exemption from ERISA’s definition of “fiduciary,” causing a split with the Fourth, Fifth, Seventh, Eighth, and Ninth Circuits, which do not apply such an exemption. On December 13, 2021, the Supreme Court invited the Solicitor General to file a brief expressing the views of the United States. If the Court takes up this case, it could impact whether plan administrators and their contractors may face liability as plan fiduciaries when making business decisions, such as executing service-provider contracts, that affect prices paid by the plan or its participants.

2. OptumHealth Care Solutions, LLC v. Peters (No. 21-761)

In OptumHealth Care Solutions, LLC v. Peters, the Supreme Court has called for a response to a petition for a writ of certiorari by OptumHealth Care Solutions LLC addressing ERISA section 406(a)’s prohibition against certain “transactions” by plan fiduciaries involving a “party in interest.” The petition challenges a Fourth Circuit decision holding that a non-fiduciary service provider, with no preexisting relationship to a plan, may qualify as a “party in interest” by contracting with a plan fiduciary and getting paid under those contracts.

The case arises from an agreement by Aetna to pay OptumHealth Care Solutions, Inc. (“Optum”) to provide access to Optum’s networks of chiropractors and physical therapists for members of a self-funded health plan administered by Aetna. Peters v. Aetna Inc., 2 F.4th 199, 210 (4th Cir. 2021). Plaintiff alleges that instead of paying Optum out of the fees Aetna received from the plan, Aetna requested that Optum add its administrative fee to the claims submitted by Optum’s downstream health care providers. Id. This arrangement allegedly caused Optum’s fees to be passed on to plan members, instead of being paid by Aetna, as the plan allegedly required. Id. Among other theories, plaintiff claimed that Aetna’s contract with Optum violated ERISA’s prohibition on transactions with parties in interest. Id. at 213. The district court disagreed, concluding that Optum could not be liable as a party in interest because it had no preexisting relationships with either the plan or Aetna. Id.

The Fourth Circuit reversed, holding that Optum could be held liable “based on its apparent participation in and knowledge of Aetna’s administrative fee billing model.” Id. at 240. Because Optum lacked a prior relationship with the plan, the Fourth Circuit concluded that it was not a party in interest at the time it entered into the service agreement with Aetna. But the Fourth Circuit nonetheless held that a reasonable factfinder could find Optum liable as a party in interest when it performed the contract by providing services to the plan allegedly with knowledge of circumstances that rendered the billing arrangement with Aetna unlawful. Id.

Optum filed a cert petition, asking the Supreme Court to resolve the question of whether a service provider can qualify as a party in interest under ERISA section 406(a) if the provider lacks a preexisting relationship with the plan that is independent of the relationship created by the allegedly prohibited transaction. In its petition, Optum contends that the Fourth Circuit’s decision exposes plan fiduciaries and non-fiduciary service providers to litigation simply by engaging in and being paid under an arms-length services agreement, and thereby creates a split with the Tenth Circuit, which held in Ramos v. Banner Health, 1 F.4th 769, 784, 787 (10th Cir. 2021), that ERISA does not categorically prohibit plan fiduciaries from contracting with third-party service providers, and that such an interpretation of the statute would lead to “absurd result[s]” that would extend to “run-of-the-mill service agreements, opening plan fiduciaries up to litigation merely because they engaged in an arm’s length deal with a service provider.” In Ramos, the Tenth Circuit concluded that “some prior relationship must exist between the fiduciary and the service provider to make the provider a party in interest” under ERISA. Id. at 787. The Fourth Circuit’s decision in Peters would appear not to require evidence of a “prior relationship” to trigger prohibited transaction liability.

The Supreme Court sought a response from respondent on Optum’s petition for a writ of certiorari, suggesting the Court may want to weigh in on whether a “preexisting relationship” is required before a third-party contractor providing administrative services to a plan may qualify as a “party in interest.”

3. Howard Jarvis Taxpayers Association v. CA Secure Choice Retirement Program (No. 21-558)

We are also monitoring a pending petition for a writ of certiorari that asks the Supreme Court to review a preemption challenge to CalSavers, California’s state-run auto-enrollment IRA program. CalSavers is one of a handful state-run IRA programs for private sector workers. It applies to eligible employees of certain private employers in California that do not provide their employees with a tax-qualified retirement savings plan. Eligible employees are automatically enrolled in CalSavers, but may opt out. If they do not opt out, their employers must remit certain payroll deductions to CalSavers, which then funds the employees’ IRAs. California manages and administers the IRAs and acts as the program fiduciary.

Howard Jarvis Taxpayers Association challenged the CalSavers program, arguing that it is preempted by ERISA. The Ninth Circuit rejected this argument, concluding that ERISA does not preempt CalSavers, and relying in part on the Supreme Court’s decision in Rutledge v. Pharmaceutical Care Management Association, 141 S. Ct. 474 (2020). See Howard Jarvis Taxpayers Ass’n v. California Secure Choice Ret. Sav. Program, 997 F.3d 848, 863 (9th Cir. 2021). As we discussed in last year’s ERISA update, the Supreme Court held in Rutledge that ERISA did not preempt an Arkansas statute regulating the rates at which pharmacy benefit managers (“PBMs”) reimburse pharmacies for prescription drug costs because the law “is merely a form of cost regulation . . . [that] applies equally to all PBMs and pharmacies in Arkansas,” and therefore is not subject to ERISA preemption because it did not have an impermissible connection with or reference to ERISA. Rutledge, 141 S. Ct. at 481. In Howard Jarvis, the Ninth Circuit relied on the Supreme Court’s reasoning in Rutledge to hold that ERISA did not preempt CalSavers, reasoning that:

CalSavers is not an ERISA plan because it is established and maintained by the State, not employers; it does not require employers to operate their own ERISA plans; and it does not have an impermissible reference to or connection with ERISA. Nor does CalSavers interfere with ERISA’s core purposes.

997 F.3d at 852–53. In so holding, the Ninth Circuit rejected plaintiff’s argument that CalSavers is preempted because it “competes with” ERISA plans and will “frustrate, not encourage the formation of” ERISA plans. Id. at 864. The court concluded that the Supreme Court’s decision in Rutledge made clear that “‘ERISA does not pre-empt’ state laws that ‘merely increase costs or alter incentives for ERISA plans without forcing plans to adopt any particular scheme or substantive coverage.’” Id. (quoting Rutledge, 141 S. Ct. at 480).

The Supreme Court requested the CalSavers program to respond to a petition for a writ of certiorari filed by Howard Jarvis Taxpayers Association. A decision by the Court in this case may have far-reaching impact for the viability of state-run auto-IRA programs that are proliferating throughout the country, including in Colorado, Connecticut, Illinois, Maryland, New Jersey, and Oregon. For further discussion of how courts of appeals have applied Rutledge, including further discussion of the Ninth Circuit’s decision in Howard Jarvis Taxpayers Association v. CA Secure Choice Retirement Program, see infra Section III.

II. Article III Standing in ERISA Cases Under Thole v. U.S. Bank and TransUnion LLC v. Ramirez

As we addressed in our update last year, Article III standing continues to be a key issue for ERISA litigants. Here we analyze how the federal courts are implementing the Supreme Court’s Article III standing decisions in Thole v. U.S. Bank, 140 S. Ct. 1615 (2020), and TransUnion LLC v. Ramirez, 141 S. Ct. 2190 (2021), in the ERISA context.

In Thole, the Supreme Court held that participants in a fully funded defined-benefit pension plan lacked Article III standing to sue under ERISA for breach of fiduciary duties because, while the plan lost $750 million due to the fiduciaries’ alleged breach, the participants had no “concrete stake in the lawsuit.” Thole, 140 S. Ct. at 1618–19. Plaintiffs continued to receive all of their vested benefits to which they were legally entitled, and those “benefits are fixed and will not change, regardless of how well or poorly the plan is managed.” Id. at 1620, 1622. The Court’s decision in Thole means that plaintiffs do not have standing to bring a breach of fiduciary duty claim against a defined-benefit plan unless they have suffered a concrete injury such as the plan’s failure to make the required benefit payments. Id. at 1619.

In the year and a half since Thole came down, the courts of appeals have generally declined to extend Thole outside the defined-benefit plan context. However, at least one district court has taken a broader view and applied Thole in the context of employer-sponsored health plans, finding plaintiffs lacked standing because they could not allege that their own claims for benefits were impaired by cross-plan offsetting.

In Ortiz v. American Airlines, Inc., the Fifth Circuit declined to extend Thole to claims of breach of fiduciary duty brought by plan participants in a defined-contribution retirement plan. 5 F.4th 622, 629 n.9 (5th Cir. 2021). In relevant part, plaintiffs alleged that defendants should have offered a stable-value investment option in their plan, and that plaintiffs lost investment income by investing in the lower return option in their plan. Id. at 629. Defendants argued that Thole should preclude Article III standing because the plaintiffs did not have a cognizable injury giving them a concrete stake in the lawsuit. Id. The Fifth Circuit disagreed, explaining that Thole “explicitly drew a distinction between a defined-benefit plan and a defined contribution plan, such as a 401(k), in which the retirees’ benefits are typically tied to the value of their accounts, and the benefits can turn on the plan fiduciaries’ particular investment decisions.” Id. (quotation markss omitted). Here, however, the court noted that plaintiffs had presented evidence that the plan fiduciaries’ decisions, although affecting the plan as a whole, resulted in “lost investment income” to their individual accounts that was concrete and redressable for purposes of standing. Id. at 629.

The Third Circuit will have the opportunity to decide an appeal raising a similar issue in the near future. In Boley v. Universal Health Services, Inc., 498 F. Supp. 3d 715 (E.D. Pa. 2020), plaintiffs allege that fiduciaries for their defined-contribution retirement plan imprudently offered high-fee investment options in the plan, resulting in the plan and its participants paying excessive fees. Id. at 718. Plaintiffs alleged that they invested in only seven of the plan’s many fund offerings during the putative class period, and defendants argued that under Thole, plaintiffs lacked standing to bring claims as to the remaining funds, because plaintiffs could not show a personal injury to their individual account balances due to the performance of the funds in which they did not invest. Id. at 719. The district court disagreed, concluding that plaintiffs had standing to challenge funds in which they did not invest because, unlike in Thole, plaintiffs’ claims alleged, among other things, a “[p]lan-wide breach as to process,” and this “imprudent process forced [plaintiffs], and all Plan participants, to choose from an expensive menu of investment options” that injured all plan participants, including plaintiffs. Id. at 719, 721, 723–24 (quotation marks omitted). Defendants have appealed this decision, with argument held on February 11, 2022. See generally Boley v. Universal Health Svcs., Inc., No. 21-2014 (3d Cir.). Thus, like the Fifth Circuit in Ortiz, the Third Circuit will have to decide whether allegations of injury stemming from fiduciaries’ alleged retention of imprudent investment options—thereby causing a plan to generate less investment income for its participants—are sufficient to satisfy Article III standing even where the named plaintiffs do not allege they invested in the challenged funds.

Last year, the Second Circuit also had the opportunity to weigh in on the breadth of Thole. In Gonzales de Fuente v. Preferred Home Care of New York LLC, the court affirmed dismissal of plaintiffs’ complaint on standing grounds where plaintiffs were participants in a defined-benefit health plan who claimed breach of ERISA fiduciary duties due to alleged misappropriation of employer contributions to the plan, which plaintiffs contended should have been used to provide them a superior plan. 858 F. App’x. 432 (2d Cir. 2021). The case implicated New York’s wage parity law, which forbids employers from retaining any “portion of the dollars spent or to be spent to satisfy the wage or benefit portion” of employee compensation. Id. at 434 (quoting N.Y. Pub. Health Law § 3614-c(5)(a)). Plaintiffs argued that the New York law made their status under ERISA more like that of defined contribution plan participants, and they argued they suffered “concrete injuries in the form of increased out-of-pocket costs and reduced coverage.” Id. at 433. In rejecting this argument, the Second Circuit relied on Thole to hold that plaintiffs lacked standing to bring their ERISA claims because they had received, and would receive, all promised benefits under their health plan, and any compensation plaintiffs may have been entitled to under the New York law was separate from their ERISA claim. Id. at 434.

The United States District Court for the District of Minnesota reached a similar result in Scott v. UnitedHealth Group, Inc., 540 F. Supp. 3d 857, 859 (D. Minn. 2021). The court rejected plaintiffs’ argument that they had standing to challenge their employers’ health plans’ practice of cross-plan offsetting because their plans are funded in part by their payroll contributions. Id. at 862. The court found that, as in Thole, the “plaintiffs do not have any claim to the plans’ assets; instead, their only claim is to receive the benefits to which they are entitled” under the plans. Id. at 863. Thus, the court found that rather than being a defined contribution plan, an employer-sponsored health plan is “closely analogous” to a defined-benefit plan. Id. at 864. Applying Thole, the court held that plaintiffs did not have standing because they could not allege that any of their own claims for benefits had been denied due to the alleged cross-plan offsetting. Id. at 865.

The Supreme Court further clarified the requirements for Article III standing last year in TransUnion LLC v. Ramirez, 141 S. Ct. 2190 (2021), limiting the size of a putative class action alleging violations of the Fair Credit Reporting Act (“FCRA”) for failing to ensure that information on TransUnion’s credit reports is accurate before disseminating them. Id. at 2200. Even though most class members did not suffer an injury from the disclosure of their credit reports to third parties, the Ninth Circuit affirmed certification of the class and concluded that all class members had Article III standing to recover damages because of the mere “risk of harm to their concrete privacy, reputational, and informational interests protected by the FCRA.” Id. at 2202; id. at 2216 (Thomas, J., dissenting) (emphasis added).

The Supreme Court reversed in part, narrowing the class to plaintiffs who could establish Article III standing, reasoning that “Article III does not give federal courts the power to order relief to any uninjured plaintiff” regardless of whether they are part of a class. Id. at 2208 (Kavanaugh, J.) (quoting Tyson Foods, Inc. v. Bouaphakeo, 577 U.S. 442, 466 (2016) (Roberts, C.J., concurring)). The Court explained that the violation of a federal statute is not, alone, sufficient to confer standing under Article III, id. at 2206, but may be sufficient if the harm alleged has a “‘close relationship’ to a harm traditionally recognized as providing a basis for a lawsuit,” id. at 2200. Here, the Court explained, plaintiffs whose credit reports bearing misleading information had been disclosed to third parties could establish Article III standing based on reputational harm analogous to the traditional tort of defamation. Id. at 2205, 2209. But the Court held that the rest of the plaintiffs—whose credit reports were not disseminated to third parties—lacked standing to seek damages because they merely faced, at most, a “risk of future harm.” Id. at 2210. Although “a person exposed to a risk of future harm may pursue forward-looking, injunctive relief to prevent the harm from occurring, at least so long as the risk of harm is sufficiently imminent and substantial,” the Court held that “in a suit for damages, the mere risk of future harm, standing alone, cannot qualify as a concrete harm—at least unless the exposure to the risk of future harm itself causes a separate concrete harm.” Id. at 2210–11.

These holdings may have significant consequences in ERISA cases. In ERISA class actions, TransUnion appears to require Plaintiffs to establish that each class member suffered an Article III injury, potentially raising individualized inquiries that could impede class certification. Further, TransUnion clarifies the standard for establishing Article III standing, potentially limiting ERISA claims premised on purely procedural injuries or risk of future harm in actions seeking damages or other retrospective relief. Taken together, the Thole and TransUnion decisions give ERISA defendants paths to argue (1) that plan participants lack concrete harm sufficient to confer Article III standing, and (2) for limits on available remedies.

III. Impact of the Supreme Court’s Decision in Rutledge v. Pharmaceutical Care Management Association on ERISA Preemption

As we anticipated in our 2020 ERISA Update, the Supreme Court’s decision in Rutledge v. Pharmaceutical Care Management Association, 141 S. Ct. 474 (2020) has played a significant role over the last year-and-a-half in litigation concerning ERISA preemption of state laws. Subject to certain exceptions, ERISA preempts any state law that “relate[s] to” an ERISA plan, 29 U.S.C. § 1144(a), meaning that the law has either a “connection with” or a “reference to” ERISA plans, Egelhoff v. Egelhoff ex rel. Breiner, 532 U.S. 141, 147 (2001) (citation omitted). A state law has an impermissible connection with ERISA plans if it “governs … a central matter of plan administration or interferes with nationally uniform plan administration.” Gobeille v. Liberty Mut. Ins. Co., 577 U.S. 312, 320 (2016) (internal quotation marks and citation omitted). And a state law impermissibly refers to ERISA plans if it “acts immediately and exclusively upon ERISA plans” or “the existence of ERISA plans is essential to the law’s operation.” Id. at 319–20 (citation omitted).

In Rutledge, the Court applied these principles to an Arkansas statute regulating the rates at which pharmacy benefit managers (PBMs), acting as middlemen between ERISA plans and pharmacies, reimburse pharmacies for prescription drug coverage. 141 S. Ct. at 478. Although PBMs generally pass drug prices on to plans, the Court held that “ERISA does not pre-empt state rate regulations that merely increase costs or alter incentives for ERISA plans without forcing plans to adopt any particular scheme of substantive coverage.” Id. at 480. The Court explained that the statute in question did not have an impermissible connection with ERISA plans because it merely regulated the cost of covered prescription drugs, not plan choices about which drugs to cover. Id. at 481. The Court also explained that the statute did not “refer to” ERISA plans because it affected plans only indirectly and it “regulate[d] PBMs whether or not the plans they service fall within ERISA’s coverage.” Id.

Last year, the Eighth, Seventh, and Ninth Circuits, as well as a number of district courts, had the opportunity to apply Rutledge, and these decisions suggest the courts are taking a narrower view of ERISA preemption.

In Pharmaceutical Care Management Association v. Wehbi, 18 F.4th 956, 964 (8th Cir. 2021), the Supreme Court vacated an earlier Eighth Circuit decision and directed the court to reconsider the case in light of Rutledge. As in Rutledge, Wehbi involved a preemption challenge to a state statute regulating in various ways the relationship between PBMs and pharmacies. Id. Most notably, the law “limit[ed] the accreditation requirements that a PBM may impose on pharmacies as a condition for participation in its network.” Id. at 968. The Eighth Circuit had initially held that the statute was preempted because it had an impermissible “reference to” ERISA, in that the statute’s “definitions of and references to ‘pharmacy benefits manager,’ ‘third-party payer,’ and ‘plan sponsor’” either referenced ERISA plans or were “taken verbatim” from ERISA. Pharm. Care Mgmt. Ass’n v. Tufte, 968 F.3d 901, 905 (8th Cir. 2020). But on remand neither party disputed that Rutledge had undercut any argument for “reference to” preemption. 18 F.4th at 969–70. The Eighth Circuit recognized this shift in the law, explaining that while “[p]reviously, circuit precedent held that the existence of ERISA plans is essential to a law’s operation if the law can apply to an ERISA plan,” now “the existence of ERISA plans is essential to a law’s operation only if the law cannot apply to a non-ERISA plan.” Id. at 969 (emphases added).

The briefing on remand focused on “connection with” preemption. The Eighth Circuit held, however, that the statute was not preempted on that basis. Id. at 970. Addressing a recurring issue, the panel explained that “the challenged provisions do not escape preemption” simply because “they regulate PBMs rather than plans.” Id. at 966. But the panel nonetheless concluded that the statute—including its limited accreditation requirements—was not preempted because it “constitute[d], at most, regulation of a noncentral ‘matter of plan administration’ with de minimis economic effects and impact on the uniformity of plan administration across states.” Id. at 968–69 (citation omitted). In upholding North Dakota’s authority to restrict the accreditation requirements a PBM may impose on pharmacies as a condition of participation in its network, the decision raises important questions about the ability of states to regulate membership in plan networks in both the pharmacy and medical treatment contexts.

Courts have also applied Rutledge in other contexts. For instance, in Halperin v. Richards, 7 F.4th 534 (7th Cir. 2021), the Seventh Circuit considered whether ERISA preempts state law claims against a company’s “directors and officers who serve[d] dual roles as both corporate and ERISA fiduciaries.” Id. at 539. The plaintiffs—creditors of a company undergoing bankruptcy proceedings—alleged that the company’s directors and officers had conspired with the trustee for the company’s ERISA-covered employee stock ownership plan to inflate the valuations of the company’s stock to drive up their own pay, which was tied to the stock ownership plan valuations. Id. The defendants argued that the claims were preempted because the company’s “valuations were governed by ERISA” and they acted solely in their ERISA roles when evaluating the company’s stock. Id. at 540. The Seventh Circuit concluded, however, that ERISA did not preempt these claims against the directors and officers, explaining that Rutledge stands for the proposition that “[s]ome parallel state rules … are not preempted,” id. at 541, and holding that “ERISA contemplates parallel state-law liability against directors and officers serving dual roles as both corporate and ERISA fiduciaries,” id. at 542. The court nonetheless held that ERISA preempted the claims against the trustee and its non-fiduciary contractor, as claims against those individuals “would interfere with the cornerstone of ERISA’s fiduciary duties.” Id. at 539.

The Ninth Circuit also relied on Rutledge in the decision at issue in the petition for a certiorari in Howard Jarvis Taxpayers Association v. CA Secure Choice Retirement Program, which is discussed supra in Section 1.C.2. See Petition for Writ of Certiorari, Howard Jarvis Taxpayers Ass’n v. CA Secure Choice Ret. Program (No. 20-15591).

A number of district court decisions have also applied Rutledge to find that ERISA does not preempt various state laws and claims. See, e.g., ACS Primary Care Physicians Sw., P.A. v. UnitedHealthcare Ins. Co., 514 F. Supp. 3d 927, 941–42 (S.D. Tex. 2021) (emergency care statutes); Emergency Physician Servs. of New York v. UnitedHealth Grp., Inc., 2021 WL 4437166, at *2, 8–9 (S.D.N.Y. Sep. 28, 2021) (breach of implied-in-fact contract and unjust enrichment claims for failing to reimburse emergency services at a reasonable rate ); Emergency Servs. of Oklahoma, PC v. Aetna Health, Inc., 2021 WL 3914255, at *1–3 (W.D. Okla. Aug. 24, 2021) (same); Elena v. Reliance Standard Life Ins. Co., 2021 WL 2072373, at *2–4 (S.D. Cal. May 24, 2021) (intentional infliction of emotional distress claim based on post-traumatic stress disorder intensified by “ridicule” suffered from third-party claim administrator’s agent with regards to disability coverage claim); Sarasota Cnty. Pub. Hosp. Bd. v. Blue Cross & Blue Shield of Florida, Inc., 511 F. Supp. 3d 1240, 1243–44, 1249 (M.D. Fla. 2021) (breach of preferred provider agreement); Florida Emergency Physicians Kang & Assocs., M.D., Inc. v. United Healthcare of Florida, Inc., 526 F. Supp. 3d 1282, 1289, 1298–99 (S.D. Fla. 2021) (conspiracy to “manipulate and depress the usual or customary reimbursement rate” for medical services).

We expect ERISA preemption will continue to be a highly litigated area this year, with courts being asked to apply Rutledge to a broad array of state regulations and common law claims. And should the Supreme Court grant the pending petition in Howard Jarvis Taxpayers Association v. CA Secure Choice Retirement Program, it would have the opportunity to further define the parameters of ERISA preemption.

IV. Arbitrability of ERISA Fiduciary-Breach Claims

The arbitrability of ERISA section 502(a)(2) fiduciary-breach claims continued to generate contentious litigation in 2021. As we detailed in our 2020 ERISA Update, the Ninth Circuit’s 2019 decision in Dorman v. Charles Schwab Corp., 934 F.3d 1107, 1111–12 (9th Cir. 2019) struck down decades of case law holding that fiduciary-breach lawsuits under ERISA could not be arbitrated. This in turn led many companies to write new arbitration language into their plans. We can now shed more light on the enforceability of these arbitration terms as additional courts of appeal have weigh in, including the Seventh and Second Circuits, as well as district courts in Ohio and Florida. As these cases suggest, federal courts continue to struggle with whether and how to enforce arbitration agreements in ERISA plans, and we expect arbitrability to continue to be a hotly litigated issue this year.

In September, the Seventh Circuit decided Smith v. Board of Directors of Triad Manufacturing, Inc., 13 F.4th 613, 615 (7th Cir. 2021), a case brought by an individual on his own behalf, and on behalf of a putative class, alleging a claim for fiduciary breach under ERISA section 502(a)(2) for mismanagement of his retirement plan and seeking removal of the plan fiduciaries. However, plaintiff’s suit ran headlong into his plan’s arbitration provision, which in relevant part, provided that plaintiff could not “seek or receive any remedy which has the purpose or effect of providing additional benefits or monetary or other relief to any Eligible, Employee, Participant or Beneficiary other than the Claimant.” Id. at 616. The district court denied defendants’ motion to compel arbitration, and the Seventh Circuit affirmed. The appellate court “[j]oin[ed] every other circuit to consider the issue” in holding that “ERISA claims are generally arbitrable.” Id. at 620. But the court concluded that the particular arbitration provision at issue ran afoul of the effective vindication doctrine, which holds that an arbitration provision may be held unenforceable on public policy grounds when it “operate[s] … as a prospective waiver of a party’s right to pursue statutory remedies.” Id. at 620–21 (citing Am. Exp. Co. v. Italian Colors Rest., 570 U.S. 228, 235 (2013)). Deploying the doctrine—which “rare[ly]” applies—the Seventh Circuit reasoned that the plan’s arbitration provision precluded certain remedies that ERISA “expressly permit[s].” Id. at 623. Specifically, the provision precluded plaintiff from seeking relief that extended beyond himself, even though ERISA expressly contemplates “such other equitable or remedial relief as the court may deem appropriate.” Id. at 621. Because the provision would preclude plaintiff from pursuing the remedy of removing the plan fiduciary, which “would go beyond just [plaintiff] and extend to the entire plan,” the provision operated as a waiver of statutory remedies and could not be enforced. Id. at 621–623. However, the court was careful to explain that “the problem with the plan’s arbitration provision is its prohibition on certain plan-wide remedies, not plan-wide representation,” signaling that the court took no issue with the provision’s class action waiver. Id. at 622. The Seventh Circuit also saw “no conflict” between its decision and the Ninth Circuit’s decision in Dorman because the Dorman arbitration provision “lacked the problematic language present here.” Id. at 623.

The Second Circuit’s recent decision in Cooper v. Ruane Cunniff & Goldfarb Inc., 990 F.3d 173 (2d Cir. 2021), provides yet another example of the emerging and divergent approaches to assessing the arbitrability of section 502(a)(2) fiduciary-breach claims. There, a split panel reversed a district court order compelling arbitration. Id. at 175–76. Rather than taking issue with the enforceability of the clause itself (as in Smith) the court noted that the plaintiff’s claims did not fall within the scope of the arbitration provision. Id. at 179. The provision covered “all legal claims arising out of or relating to employment,” but the defendant had not argued that plaintiff’s claim for fiduciary breach arose out of his employment, so the question before the Court was limited: did plaintiff’s fiduciary breach claim “relat[e] to [his] employment”? Id. at 180. The majority answered in the negative, reasoning that arbitration was only required when the “merits of th[e] claim involve facts particular to an individual plaintiff’s own employment.” Id. at 184. Writing in dissent, Judge Sullivan articulated a more expansive view of the arbitrability of fiduciary-breach claims. He argued that “[w]here, as here, an arbitration agreement uses broad language that is ambiguous about whether an issue in dispute is arbitrable, we must resolve that ambiguity in favor of arbitration.” Id. at 186 (Sullivan, J., dissenting).

This year, the Sixth Circuit will also hear an appeal in Hawkins v. Cintas Corp., No. 19-1062, 2021 WL 274341 (S.D. Ohio Jan. 27, 2021), wherein the district court declined to compel arbitration of breach of fiduciary duty claims brought on behalf of the plaintiffs’ plan. Id. at *7. The district court reasoned that the claims were not arbitrable because they were brought on behalf of the plan and there was “no agreement” between the plan and the defendant to arbitrate plan disputes. Id. at *3–4. Specifically, while the plaintiffs’ participant agreements stated that “‘the rights and claims of Employee’ will be arbitrated,” that language bound only the individual employee, not the plan. Id. at *6. The court explicitly distinguished Dorman, emphasizing that the defendant had provided no evidence that any plan document actually bound the plan to arbitration. Id. Separately, the court rejected defendant’s argument that, as sponsor of the plan, it could either consent to arbitration via the filing of a motion to compel, or otherwise “modify Plan documents to require Plan claims to proceed to arbitration.” Id. at *5, 7. Because the court found no valid agreement to arbitrate existed between the plan and the defendant, it ruled that the claims must proceed in federal court absent intervention by the Sixth Circuit.