Californians have ushered in a law protecting individuals’ privacy unlike any other in the United States, and businesses are well-advised to evaluate its impact and prepare to comply. Proposition 24, which passed during this month’s vote, establishes the California Privacy Rights Act (CPRA), which will take effect Jan. 1, 2023. If this seems like déjà vu, it is because just two years ago, the California legislature passed an unprecedented privacy law, the California Consumer Privacy Act (CCPA), which the CPRA amends. The continuing shift in privacy law embodied by the CPRA is set to make a significant impact on businesses’ compliance efforts and operational risk, as well as individuals’ expectations.

Businesses should take comfort that the Jan. 1, 2023 effective date, and delayed enforcement start (July 1, 2023), means there is time to come into compliance. However, the law imposes various changes that will require businesses to address new considerations—even factoring in the efforts many already have made to comply with the CCPA.

Originally published by The Recorder on November 18, 2020.

The following Gibson Dunn lawyers assisted in the preparation of this article: Cassandra Gaedt-Sheckter, Alexander H. Southwell and Ryan Bergsieker.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, the authors, or any member of the firm’s California Consumer Privacy Act Task Force or its Privacy, Cybersecurity and Consumer Protection practice group:

California Consumer Privacy Act Task Force:

Benjamin B. Wagner – Palo Alto (+1 650-849-5395, [email protected])

Ryan T. Bergsieker – Denver (+1 303-298-5774, [email protected])

Cassandra L. Gaedt-Sheckter – Palo Alto (+1 650-849-5203, [email protected])

Joshua A. Jessen – Orange County/Palo Alto (+1 949-451-4114/+1 650-849-5375, [email protected])

H. Mark Lyon – Palo Alto (+1 650-849-5307, [email protected])

Alexander H. Southwell – New York (+1 212-351-3981, [email protected])

Deborah L. Stein – Los Angeles (+1 213-229-7164, [email protected])

Eric D. Vandevelde – Los Angeles (+1 213-229-7186, [email protected])

Please also feel free to contact any member of the Privacy, Cybersecurity and Consumer Protection practice group:

United States

Alexander H. Southwell – Co-Chair, PCCP Practice, New York (+1 212-351-3981, [email protected])

Debra Wong Yang – Los Angeles (+1 213-229-7472, [email protected])

Matthew Benjamin – New York (+1 212-351-4079, [email protected])

Ryan T. Bergsieker – Denver (+1 303-298-5774, [email protected])

Howard S. Hogan – Washington, D.C. (+1 202-887-3640, [email protected])

Joshua A. Jessen – Orange County/Palo Alto (+1 949-451-4114/+1 650-849-5375, [email protected])

Kristin A. Linsley – San Francisco (+1 415-393-8395, [email protected])

H. Mark Lyon – Palo Alto (+1 650-849-5307, [email protected])

Karl G. Nelson – Dallas (+1 214-698-3203, [email protected])

Deborah L. Stein – Los Angeles (+1 213-229-7164, [email protected])

Eric D. Vandevelde – Los Angeles (+1 213-229-7186, [email protected])

Benjamin B. Wagner – Palo Alto (+1 650-849-5395, [email protected])

Michael Li-Ming Wong – San Francisco/Palo Alto (+1 415-393-8333/+1 650-849-5393, [email protected])

Europe

Ahmed Baladi – Co-Chair, PCCP Practice, Paris (+33 (0)1 56 43 13 00, [email protected])

James A. Cox – London (+44 (0)20 7071 4250, [email protected])

Patrick Doris – London (+44 (0)20 7071 4276, [email protected])

Bernard Grinspan – Paris (+33 (0)1 56 43 13 00, [email protected])

Penny Madden – London (+44 (0)20 7071 4226, [email protected])

Michael Walther – Munich (+49 89 189 33-180, [email protected])

Kai Gesing – Munich (+49 89 189 33-180, [email protected])

Alejandro Guerrero – Brussels (+32 2 554 7218, [email protected])

Vera Lukic – Paris (+33 (0)1 56 43 13 00, [email protected])

Sarah Wazen – London (+44 (0)20 7071 4203, [email protected])

Asia

Kelly Austin – Hong Kong (+852 2214 3788, [email protected])

Connell O’Neill – Hong Kong (+852 2214 3812, co’[email protected])

Jai S. Pathak – Singapore (+65 6507 3683, [email protected])

© 2020 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Please join us to discuss the SEC’s enforcement priorities and key areas of risk in light of COVID-19. In this webcast, we will discuss:

- The SEC’s latest accounting and pandemic-related enforcement trends and initiatives;

- Impact of the SEC Division of Enforcement’s EPS Initiative;

- Key areas of accounting risk amplified by COVID-19, including revenue recognition, asset impairment, and going concern risks; and

- Disclosure issues pertaining to COVID-19’s impact on business and forward-looking guidance.

View Slides (PDF)

PANELISTS:

Richard W. Grime is co-chair of Gibson Dunn’s Securities Enforcement Practice Group. Mr. Grime’s practice focuses on representing companies and individuals in corruption, accounting fraud, and securities enforcement matters before the SEC and the DOJ. Prior to joining the firm, Mr. Grime was Assistant Director in the Division of Enforcement at the SEC, where he supervised the filing of over 70 enforcement actions covering a wide range of the Commission’s activities, including the first FCPA case involving SEC penalties for violations of a prior Commission order, numerous financial fraud cases, and multiple insider trading and Ponzi-scheme enforcement actions.

Monica K. Loseman is co-chair of Gibson, Dunn’s Securities Litigation Practice Group and is a partner in the Denver office. Ms. Loseman has substantial experience in complex corporate and securities enforcement matters and civil litigation. Her practice includes a focus on financial reporting, accounting and related investigations and accountant defense. Ms. Loseman’s trial experience largely focused on accounting and financial reporting and corporate governance matters, including three trials before SEC administrative law judges, several bench and jury trials, and private arbitrations. Ms. Loseman also conducts independent investigations involving allegations of corporate fraud and issues relating to financial reporting, accounting, internal controls, and other issues, and is skilled at interacting with Board committees and other stakeholders in presenting results and remedial recommendations.

Michael J. Scanlon is a partner in the Washington, D.C. office, where he is a member of the Firm’s Securities Regulation and Corporate Governance, and Securities Enforcement Practice Groups. Mr. Scanlon has an extensive practice representing U.S. and foreign public company and audit firm clients on regulatory, corporate governance, and enforcement matters. He advises corporate clients on SEC compliance and disclosure issues, the Sarbanes-Oxley Act, and corporate governance best practices, with a particular focus on financial reporting matters.

Jason H. Smith is a senior associate in the Washington, D.C office where, he is a member of the White Collar Defense and Investigations Practice Group and focuses primarily on white collar defense, corporate compliance, and securities enforcement. Mr. Smith has particular experience representing multinational corporate clients in government investigations, including before the Department of Justice, Securities and Exchange Commission, and other regulatory and enforcement agencies.

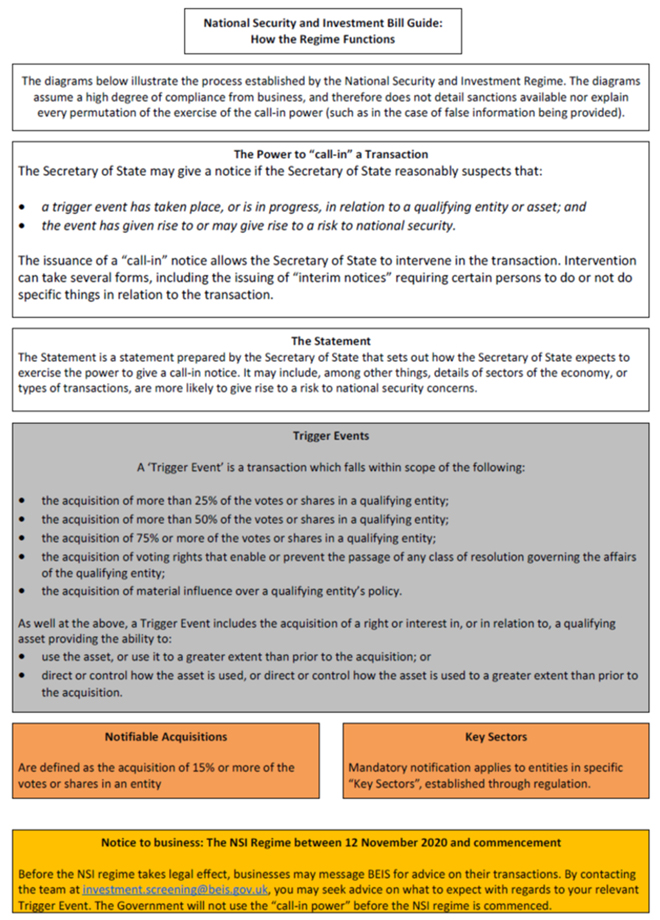

The UK Government (the “Government”) has announced plans to upgrade and widen significantly its intervention powers on grounds of national security.

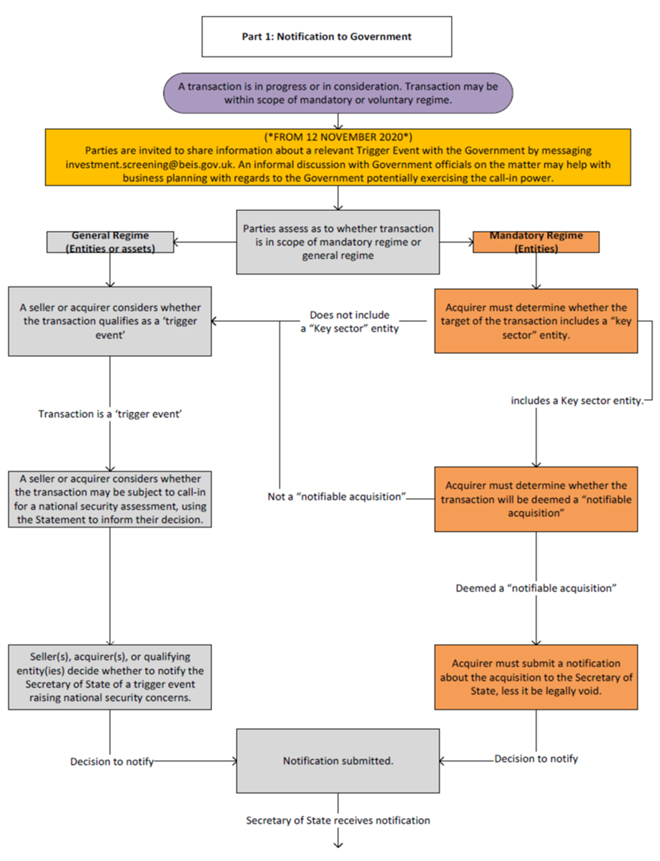

The proposal is for a ‘hybrid regime’ whereby notification and approval would be mandatory prior to completing certain deals (described further below) in specified areas of the economy deemed particularly sensitive. Here, clearance would be required to be obtained prior to closing. Further, any failure to notify would result in a transaction that is ‘legally void’,[1] sanctions would be applicable and the Government would have a potentially indefinite period to ‘call-in’ the deal (a period which would be reduced to 6 months if the Secretary of State for Business, Energy and Industrial Strategy (the “SoS”) becomes aware of the deal). Notification will otherwise be voluntary. However, the Government will be able to ‘call-in’ such transactions for a period of up to 5 years (again, this period would be reduced to a period of 6 months if the SoS becomes aware of the deal). Once a transaction has been called in and assessed, where necessary and proportionate, the Government will have the power to impose a range of remedies to address any national security concerns.

The proposed regime represents a significant expansion and extension of the current rules, including a significant broadening of the nature of transactions that can be reviewed (e.g. removing safe harbours based on turnover and market share and including acquisitions of certain qualifying assets, including acquisitions of land, physical assets and IP).[2] It is expected to result in significantly higher levels of scrutiny going forward. Indeed, the Government estimates that around 1,000-1,830 notifications could be received a year with 70-95 cases called in for a full national security assessment under the new regime. However, practitioners are of the view that the bill and the proposed secondary legislation detailing the sensitive sectors (as currently drafted) could result in many more notifications.

The Government, however, continues to emphasise the importance of foreign direct investment projects in the UK and the need to ensure that the UK remains an attractive place to invest. Indeed, the Government’s commitment to staying open to foreign investment is reflected in the Prime Minister’s recent announcement of the creation of the Office for Investment. This is a Government unit aimed at driving foreign investment into the UK (tasked to land high value investment opportunities and to resolve potential barriers to landing ‘top tier’ investments).[3] The Business Secretary Alok Sharma also specifically stated on the bills introduction to Parliament that: “The UK remains one of the most attractive investment destinations in the world and we want to keep it that way […] This Bill will mean that we can continue to welcome job-creating investment to our shores, while shutting out those who could threaten the safety of the British people.” The emphasis of the new proposals is thus on encouraging engagement, so that the Government becomes aware of a greater number of deals and can check that they do not pose risks to the UK’s national security. It has been emphasised that a targeted and proportionate approach to enforcement will be adopted, and that most transactions will be cleared without intervention (albeit that conditions will be required to be imposed in some cases and reviews will impact transaction timetables). The regime also introduces a clearer and more defined process for national security reviews than is currently the case, which should assist with transaction planning.[4]

The proposal is set out in the ‘National Security and Investment Bill’ (the “NSIB”) which will be subject to Parliamentary scrutiny before being passed into law.[5] However, in the interim, investors will need to be aware that the proposed legislation will give the Government the retroactive power from commencement to open an investigation into a transaction that has been completed following the introduction of the NSIB to Parliament (i.e. on or from 12 November 2020) but prior to the commencement of the Act. In such circumstances, the Government will have 6 months from the commencement day to intervene, if the SoS previously became aware of the transaction. Otherwise, the Government will be able to ‘call-in’ the deal up to 5 year’s following the commencement date, unless the SoS becomes aware of the transaction earlier in which case this period is reduced to 6 months from when the SoS becomes aware of the deal.[6]

Key aspects of the proposed new regime are detailed below. At the end of this briefing, we also include some practical tips for transacting parties.

Mandatory vs voluntary notification

- The NSIB provides for the mandatory pre-closing notification of certain acquisitions of voting rights or shares (see “Trigger events/qualifying transactions”, below) in entities active in specified sectors and involved in activities considered higher risk.

- The Government is currently consulting on the proposed sectors, and which parts of each sector, should fall within the scope of the mandatory regime, which will later be defined through secondary legislation.[7]

- As currently proposed, the following 17 sectors would be affected: advanced materials; advanced robotics; artificial intelligence; civil nuclear; communications; computing hardware; critical suppliers to government; critical suppliers to the emergency services; cryptographic authentication; data infrastructure; defence; energy; engineering biology; military or dual-use technologies; quantum technologies; satellite and space technologies and transport.

- The NSIB will provide the Government with powers to amend the types of transactions in scope of the mandatory notification regime – which will include powers to amend the sectors subject to mandatory notification as well as the nature of transactions giving rise to mandatory notification requirements (discussed further below) and exempting certain types of acquisition. It is not clear as yet the circumstances in which dispensations will be granted – it is expected that these will be developed over time (if, for example, the Government finds that certain types of transactions caught by the mandatory regime routinely do not require remedies and thus do not present sufficient security concerns – this may, for example, be based on the characteristics of the investors involved or the type of transaction).

- The fact that sectors of the economy giving rise to mandatory notification requirements will be defined in secondary legislation gives ministers significant discretion to alter the regime without full parliamentary scrutiny. Indeed, it has been specifically called out by the Government that such sectors are ‘highly likely to change over time’, in response to changing risks.

- As mentioned above, if parties fail to notify a trigger event that is subject to mandatory notification, the Government can call it in whenever it is discovered – albeit that the Government is under a 6 month deadline from which the SoS becomes aware of the transaction to call-in the deal. This does not apply to events which take place prior to the commencement of the NSIB, as no mandatory notification requirement will apply until that point.

- In addition to the mandatory regime, parties will be able to voluntary notify deals. The NSIB will permit ministers to ‘call-in’ transactions (not subject to the mandatory regime) up to 6 months after the SoS becomes aware of the transaction (including potentially, through coverage of the deal in a national news publication[8]) provided that this is done within 5 years and there is a ‘reasonable suspicion’ that it may give rise to a national security risk (a transaction cannot be ‘called-in’ for any broader economic interest issues such as employment).[9]

Trigger events / qualifying transactions

- The NSIB envisages that a number of transactions will give rise to so called ‘trigger events’, which will provide an opportunity for the Government to review a transaction. These include acquisitions of:

- More than 25%, 50% and 75% of the voting rights or shares of an entity (with increases in shareholding passing over these thresholds notifiable);

- Voting rights that ‘enable or prevent the passage of any class of resolution governing the affairs of the entity’;

- ‘Material influence’ over an entity’s policy; and

The concept of ‘material influence’ is an existing concept under the UK’s competition regime. It can be based on an acquirer’s shareholding, its board representation or other factors. For shareholdings, the CMA may examine shareholdings of 15% or more to determine whether an acquirer will have material influence. Even a shareholding of less than 15% might attract scrutiny in exceptional cases (where other factors indicate that the ability to exercise material influence over policy are present).

-

- A right or interest in, or in relation to, a qualifying asset providing the ability to:

- use the asset, or use it to a greater extent than prior to the acquisition; or

- direct or control how the asset is used, or direct or control how the asset is used to a greater extent than prior to the acquisition.

- A right or interest in, or in relation to, a qualifying asset providing the ability to:

Assets in scope of the regime will be defined in the NSIB – as currently proposed, this includes land, tangible moveable property,[10] and ideas, information, or techniques with industrial, commercial or other economic value (including, for example, trade secrets, databases, algorithms, formulae, non-physical designs and models, plans, drawings and specifications, software, source code and IP).

- The mandatory notification requirement would apply to the trigger events specified in (i) and (ii), above, plus an acquisition of 15% or more of the voting rights or shares of an entity. Whilst the latter is not a ‘trigger event’ for notification per se, it is designed to bring transactions to the attention of the SoS so that they can decide whether trigger event (iii) has occurred.

- So, in summary, the NSIB envisages that it could apply to shareholding as low as 10-15% and will cover deals involving a broad range of asset types.

- Moreover there are currently no safe harbour provisions (e.g. in terms of UK market share or turnover requirements) pursuant to which the Government would not have jurisdiction to review the transaction. However, transactions will require a UK nexus (as discussed below).

UK nexus

- The new regime will apply to investors from any country, including where acquirers and sellers do not have a direct link to the UK. To intervene in such circumstances, the SoS must be satisfied that:

- in respect of a target entity formed or recognised under laws outside of the UK, the entity carries on activities in the UK or supplies goods or services to persons in the UK; and

- in respect of a target asset situated outside of the UK or intellectual property, the asset must be used in connection with activities carried on in the UK or the supply of goods or services to persons in the UK.[11]

- This means, for example, that a business in one country acquiring a business in another country may fall within the regime if the latter carries out activities or provides services or goods in the UK with national security implications. This is also the case in relation to assets which may be used in connection with goods or services provided to UK persons e.g. deep-sea cables located outside of the UK’s geographical borders delivering energy to the UK or intellectual property located outside of the UK but key to the provision of critical functions in the UK.

- The Government intends to legislate for a tighter nexus test in the case of mandatory transactions, but this would not preclude the Government from using the call-in power to intervene in transactions with less direct links to the UK.

Likelihood of intervening – voluntary notifications

- The Government intends to publish a Statutory Statement of Policy Intent (which will be reviewed at least every 5 years), setting out when the Government expects to use its call-in power. This document will assist with the assessment of when a voluntary notification is more likely to be called in – however, a large amount of discretion will still be exercisable when deciding whether or not to intervene.

- The current draft Statutory Statement of Policy Intent, published alongside the NSIB,[12] states that the SoS will consider three factors when deciding whether or not to exercise its powers, namely:

- Acquirer risk (i.e. the extent to which the acquirer raises national security concerns);

- Target risk (i.e. the nature of the target and whether it is active in an area of the economy where the Government considers risks more likely to arise e.g. within the headline sectors where mandatory notification is required); and

- Trigger event risk (i.e. the type and level of control being acquired and how this could be used in practice to undermine national security).

Examples of trigger event risk include – but are not limited to – the potential for: (i) disruptive or destructive actions: the ability to corrupt processes or systems; (ii) espionage: the ability to have unauthorised access to sensitive information; (iii) inappropriate leverage: the ability to exploit an investment to influence the UK; and (iv) gaining control of a crucial supply chain or obtaining access to sensitive sites, with the potential to exploit them. The risk will be assessed according to the practical ability of a party to use an acquisition to undermine national security.

- The type of asset acquisitions where Government may encourage a notification will also be set out in the Statutory Statement of Policy Intent. The current draft suggests that the SoS will intervene ‘very rarely’ in asset transactions. However, where assets are integral or closely related to activities deemed particularly sensitive (e.g. in sectors subject to the mandatory regime) or, in the case of land, where it is or is proximate to a sensitive site or location (e.g. critical national infrastructure sites or government buildings), acquisitions are more likely to be called in. The SoS may also take into account the intended use of the land.

Procedure

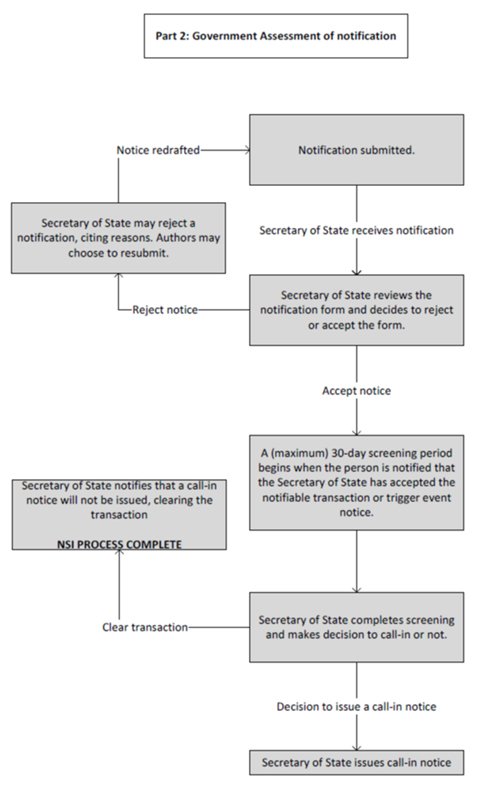

- Unsurprisingly, decisions will be taken by the SoS (currently responsible for making decisions in most national security cases under the current regime) rather than an independent body (as with competition cases).

- The SoS will be supported by the Investment Security Unit, which will sit within the Department for Business, Energy and Industrial Strategy and provide a single point of contact for businesses wishing to understand the NSIB and notify the Government about transactions. The unit will also coordinate cross-government activity to identify, assess and respond to national security risks arising through market activity.

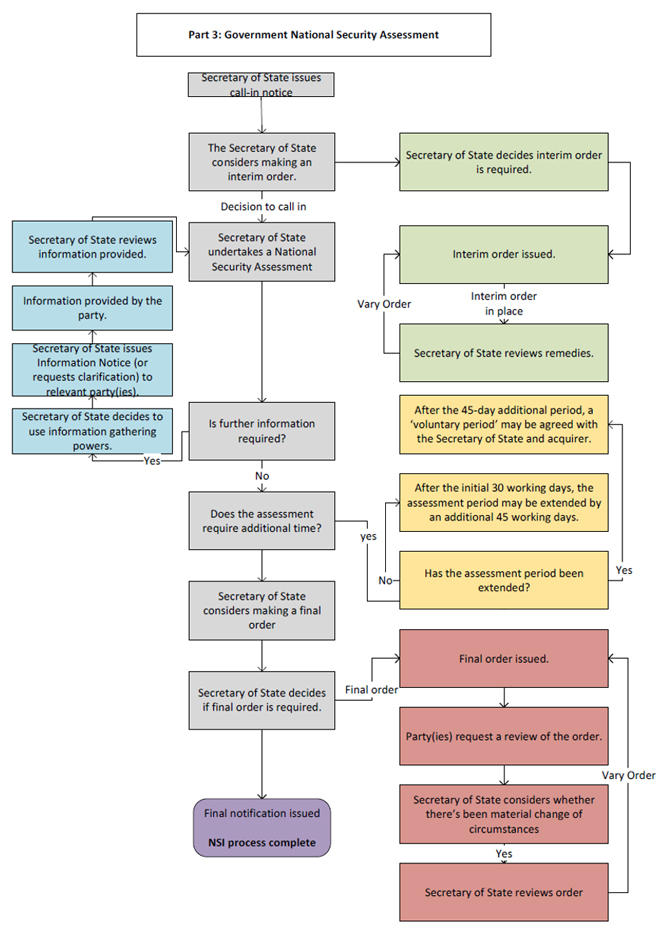

- Where a notification has been made (whether mandatory or voluntary) the SoS will have an initial 30 working day ‘screening period’ to issue a ‘call-in’ notice. Where a transaction is ‘called in’ (including for non-notified transactions), the Government will then have a 30 working day preliminary assessment period. This period would be extendable by a further 45 working days where the initial assessment period is not sufficient to fully assess the risks involved. Further extensions, beyond 75 working days, may be agreed between the acquirer and the SoS for problematic transactions. The SoS will also have the ability to ‘stop the clock’ through formally issuing an information notice or attendance notice during the process, until such a notice is complied with.

- At the end of its review, the SoS will either clear the transaction or must decide to issue a final order, if satisfied that the transaction poses, or would pose, a national security risk (on the balance of probabilities). Such orders may impose conditions or may rule that the transaction should be blocked or unwound.

- The SoS will have a range of remedies available to address national security risks associated with transactions, both while assessments take place and after their completion.

- It is not intended, as under the current regime, that parties will be able to voluntarily offer up undertakings to address concerns (however, parties will be encouraged to maintain a dialogue with the Government throughout the assessment process and it is anticipated that these conversations will assist in designing remedies; further, there will be opportunity for the parties to make representations on remedies during the assessment process). All conditions to approval will be formalised in an order and enforceable through sanctions.

- During an investigation, the Government may also issue interim orders to prevent parties from completing a transaction or, where deals have closed, integrating their operations. Such orders may have extra-territorial effects.

- Legal challenges to decisions will be subject to the standard judicial review process (subject, for certain decisions, to a shortened time limit – 28 days as opposed to the usual three-month period, although the court can give permission to bring the claim after the expiry of the 28 days). The key implication being that it will not be possible to open up decisions for a full appeal on the merits (except in respect of decisions relating to civil penalties, for which a full merits appeal will be available). Close material procedures (“CMPs”) will be utilised to ensure that sensitive materials are not improperly disclosed.[13]

Sanctions

- The proposed legislation creates a number of sanctions, civil and criminal, that will apply in the event of non-compliance. For instance, criminal and civil sanctions are applicable where an acquirer progresses to completion an acquisition subject to the mandatory notification regime, without first obtaining clearance from the SoS. The recommendation would thus be to engage early with the Government and complete the notification process in such circumstances.[14]

Anticipated impact

According to Government data, the NSIB could result in approximately 1,000-1,830 notifications a year, with call-ins/full national security assessments conducted in 70-95 cases a year and remedies anticipated in around 10 cases a year.

By comparison, the UK’s competition regime typically investigates less than 100 deals per year whilst the EU merger control regime – which is one of the toughest in the world – covered 645 cases in 2019 (283 of which were under its simplified procedure regime). Further, the current regime has involved just 12 interventions on a national security basis since 2002 (the peak year for interventions being 2019, in which 4 interventions were issued).

If enacted, this would clearly take the UK from having one of the lightest touch regimes in Europe to arguably one of the most expansive. However, it is also clear that, whilst the Government expects to be engaged and have the opportunity to review transactions (which may have consequences in terms of deal timelines and give rise to hold separate obligations in anticipated and/or completed deals), most transactions will be cleared without any intervention by way of remedies.

Timing and next steps

It is anticipated that the National Security and Investment Act will commence during the first half of next year. The Second Reading of the NSIB took place on Tuesday 17 November 2020. The committee stage (where the bill will undergo a line by line examination, with every clause agreed to, changed or removed) is scheduled for 24 November 2020.

The consultation period on the mandatory notification sectors closes on 6 January 2021. Industry is encouraged to respond and provide views on the scope of the sectors and activities currently covered by this process – as currently drafted, there a number of areas where the scope is potentially over-reaching and insightful, technical input from the market will be welcome.

Other points of note

The national security assessment will run in parallel to any competition assessment for a transaction (which will continue to be conducted by the UK Competition and Markets Authority, the “CMA”). However, whilst the two processes will be separate, there will be interactions and, in practice, outcomes will be intertwined. In particular, the legislation will include a power that would allow the SoS to intervene where competition remedies run contrary to national security interests, where this is considered necessary and proportionate. Further, the Government’s intention is that, as far as possible, any national security remedies will be aligned with competition remedies (and that the timetables will be aligned, to the extent possible, within the statutory framework to achieve this).

The Government is clear that any conflict between competition remedies and risks posed to national security will be resolved after consultation with the CMA and that mutually beneficial remedies will be imposed wherever possible. Interaction between the two regimes will be covered in more detail in a Memorandum of Understanding with the CMA. The CMA will also be under a duty to share information with the SoS and provide other assistance reasonable required to perform its functions.

What does this mean for transacting parties?

This new proposal will have a potentially significant impact on targets, sellers and acquirers alike.

For targets and sellers, it will be incumbent to undertake a review of the target’s business and activities to consider if they fall within one of the sensitive sectors and to be alive to this risk in conjunction with future capital raises, share transfers or sales of all or parts of the business, including sales of key assets, going forwards. There may be structuring options to consider. If targets or sellers are undertaking sale processes, there will also need to be greater scrutiny of acquirers in assessing transaction risk. Auction processes should also take into account the risk that a bidder may pose.

For acquirers (whether domestic or foreign – as the regime is not only designed to capture non-UK parties) consideration should be given to their ultimate controllers, the track record of those people in relation to other acquisitions or holdings, whether the acquirer has control or significant holdings in other entities active in the same sector and any relevant criminal offences or known affiliations of parties involved in the transaction, whereby an acquirer may be regarded as giving rise to acquirer risk from the SoS perspective. It is not clear to what extent parties may be able to pre-clear or seek constructive guidance in advance from the Government. There is reference in the proposals, for example, to parties having informal discussions with the Government earlier on in a sale process. However, these appear to envisage a situation whereby a specific transaction is under contemplation. Further, the Government has flagged that in a competitive process any mandatory or voluntary notification should only be made by the final bidder or acquirer in the process.

Transactions and investment deals will need to be structured to accommodate this additional risk including through introducing additional conditionality. The UK has always been open to foreign investment and, consistent with this, no transaction has been blocked to date on national security concerns. However, strict conditions have been required for deals to be cleared under the current regime. Such implications need to be considered up-front by an acquirer when planning a transaction (and risk, procedural and timing impacts appropriately factored into contractual documentation).

Given the increasing and widening emphasis on screening transactions for national security concerns, it will be important to analyse early on the risks of Government intervention/concerns arising for a transaction. Whilst concerns will be highest in the context of a takeover by a buyer affiliated to a ‘hostile state or actor’ or where a buyer owes allegiance to a hostile state or organisation, foreign nationality more generally has been considered a risk factor under the current regime. Interventions have been launched, for example, in the past, in response to investments from the United States, Canada and elsewhere in Europe. Any foreign entity may thus face close scrutiny. Concerns over asset stripping and rationalisation motivations may also provoke investigations when the acquiring company is a UK entity.

Appendix – Government Guidance, Flow Charts on Process [15]

[2] ‘Entities’ are also broadly defined , covering any entity (whether or not a legal person) but not individuals. This includes a company, LLPs, other body corporates, partnerships, unincorporated associations and trusts.

[3] See further: https://www.gov.uk/government/news/new-office-for-investment-to-drive-foreign-investment-into-the-uk.

The draft Statutory Statement of Policy Intent published concerning the new national security regime also specified with respect to the new regime that: “Its use will not be designed to limit market access for individual countries; the transparency, predictability, and clarity of the legislation surrounding the call-in power is designed to support foreign direct investment in the UK, not to limit it.”

[4] See further the Government’s press release on this development, available here: https://www.gov.uk/government/news/new-powers-to-protect-uk-from-malicious-investment-and-strengthen-economic-resilience.

[7] See further: https://www.gov.uk/government/consultations/national-security-and-investment-mandatory-notification-sectors.

[8] See, to this effect, the draft Statement of Policy Intent published: https://www.gov.uk/government/publications/national-security-and-investment-bill-2020/statement-of-policy-intent.

[9] The regime only applies to issues of national security. Other public interest issues concerning e.g. media plurality, financial stability or the UK’s ability to maintain in the UK the capability to combat, and to mitigate the effects of, public health emergencies, will continue to be dealt with through the existing channels and processes.

[10] The types of tangible moveable property of greatest national security interest will vary across sectors but are likely to be closely linked to the activities of companies in areas more likely to raise national security concerns (as identified through the requirements of the mandatory notification regime). Examples of such assets may include physical designs and models, technical office equipment, and machinery.

[12] See: https://www.gov.uk/government/publications/national-security-and-investment-bill-2020/statement-of-policy-intent.

[13] CMPs are civil proceedings in which the court is provided with evidence by one party that is not shown to another party to the proceedings. Any restricted evidence is heard in closed hearings, with the other party(ies) excluded and their interests represented by a Special Advocate. The rationale behind CMPs is to ensure that evidence can still be used in the proceedings, rather than being excluded completely under the doctrine of public interest immunity (and, specifically, on grounds of national security).

[14] Further examples are listed below – however, this is not an exhaustive list of proposed sanctions.

Failure to notify or non-compliance with interim or final orders could result in fines of up to 5% of total worldwide turnover or £10 million (whichever is higher) on businesses and prison sentences and/or fines for individuals. Failing to comply, without reasonable excuse, with an information or attendance request could results in fines on companies and fines and/or imprisonment for individuals. It will also be an offence to knowingly or recklessly supply information that is false or misleading in a material respect – punishable through fines and/or through the sentencing of individuals to prison. There would also be an opportunity for the SoS to reconsider decisions and (re-)review a trigger event in these circumstances, even if outside of the prescribed ‘call-in’ period for voluntary transactions. Unauthorised use or disclosure of regime information would also see individuals subject to imprisonment and/or a fine.

[15] Source: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/934438/process-flow-chart-for-businesses.pdf.

Gibson Dunn’s lawyers are available to assist in addressing any questions that you may have regarding the issues discussed in this update. For further information, please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s Antitrust and Competition, Mergers and Acquisitions, or International Trade practice groups, or the authors:

Ali Nikpay – Partner – Head of Competition and Consumer Law, London (+44 (0) 20 7071 4273, [email protected])

Deirdre Taylor – Partner – Antitrust and Competition, London (+44 (0) 20 7071 4274, [email protected])

Attila Borsos – Partner – Competition and Trade, Brussels (+32 2 554 72 11, [email protected])

Selina S. Sagayam – Partner – International Corporate, London (+44 (0) 20 7071 4263, [email protected])

Sarah Parker – Associate – Competition and Consumer Law, London (+44 (0) 78 3324 5958, [email protected])

Tamas Lorinczy – Associate – Corporate, London (+44 (0) 20 7071 4218, [email protected])

© 2020 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

In 2013, California set hydrogen infrastructure targets to promote development and growth of the fuel cell electric vehicle (FCEV) and hydrogen fueling market.[1] Yesterday, the California Air Resources Board (CARB) released a draft annual report that analyzes the industry’s current status and near-term outlook, and recommends “actions necessary to maintain progress and enable continued future expansion.”[2]

Despite the COVID-19 pandemic, California’s hydrogen fueling network and the number of FCEVs on the road have continued to grow over the past year.[3] CARB concluded that the hydrogen fueling industry is “responding favorably” to California’s “maturing support systems.”[4] As of July 3, 2020, there were 42 open-retail stations, with five stations opened and nine newly funded this year.[5] The total network has reached 71 opened and planned projects across the State.[6] And the California Energy Commission is expected to announce the recipients of co-funding for new stations in the near future.[7]

Although growth projections have shifted back one year compared to prior estimate due to the pandemic, auto manufacturers nevertheless seem poised to accelerate production of FCEVs in tandem with projected fueling station development.[8] And deployment data suggests that FCEV technology has a shot at wide-spread consumer adoption based on similar trends for consumer acceptance of the current generation of battery electric vehicles.[9]

While California’s hydrogen fueling network has continued to advance and has become a priority among public and private stakeholders, CARB notes that progress must “not only continue[] but accelerate[]” in order to meet “State and industry targets for both zero-emission infrastructure development and [zero-emission vehicle] deployment.”[10] Although the State is on track to meet its AB 8 goals, “there is little room for station development delays.”[11] Specifically, the market needs “continued and coordinated industry and State support” to achieve economies of scale so that manufacturers will continue to produce FCEVs, and customer-facing costs will drop enough to make FCEV ownership possible for a broader swath of the California population.[12] CARB cites several “complementary factors” that are crucial to successful FCEV market growth: development of new supply chains and manufacturing capacity; increased consumer awareness and acceptance of FCEVs and hydrogen technology; expansion of the hydrogen fuel production network; and use of consumer incentives to make the technology more affordable.[13]

CARB recommends six specific priorities for industry development:

- Use AB 8 and HRI program funding, and any other means available, to develop as many light-duty hydrogen fueling stations as possible through the end of the AB 8 program.

- Appropriately balance the goals of developing stations in communities statewide and driving larger-capacity growth in highly developed local networks.

- Continue to assess ongoing and projected development pace and quickly address bottlenecks as the technology transitions to a broader market.

- Understand capacities and opportunities to reduce State funding and transition to a financially self-sufficient industry.

- Expand upstream hydrogen supply to ensure fuel availability for customers as the market expands.

- Encourage use of renewable hydrogen.[14]

CARB has solicited public and expert review of the draft report and will release a final revised report in 2021.

___________________

[1] Assembly Bill No. 8 (Statutes of 2013).

[2] California Air Resources Board, 2020 Annual Evaluation of Fuel Cell Electric Vehicle Deployment & Hydrogen Fuel Station Network Development xiv.

The following Gibson Dunn lawyers assisted in preparing this client update: Thomas Manakides, Abbey Hudson, Joseph Edmonds and Jessica Pearigen.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s Environmental Litigation and Mass Tort practice group, or any of the following:

Stacie B. Fletcher – Co-Chair, Washington, D.C. (+1 202-887-3627, [email protected])

Daniel W. Nelson – Co-Chair, Washington, D.C. (+1 202-887-3687, [email protected])

Thomas Manakides – Orange County (+1 949-451-4060, [email protected])

Abbey Hudson – Los Angeles (+1 213-229-7954, [email protected])

Joseph D. Edmonds – Orange County (+1 949-451-4053, [email protected])

Jessica M. Pearigen – Orange County (+1 949-451-3819, [email protected])

© 2020 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Trying a merger case against a government enforcement agency, state or federal, presents unique challenges. Drawing on their experiences in the recent AT&T/Time Warner and Sprint/T-Mobile merger trials, Gibson Dunn trial and appellate lawyers will discuss cases where the government did and did not have the benefit of a presumption of competitive harm, as well as the role of fact witnesses, party documents, and experts. The panel will also discuss how to involve trial counsel in the merger-clearance phase and how the merging parties’ strategy during the clearance phase can affect the eventual litigation strategy.

View Slides (PDF)

PANELISTS:

Kristen Limarzi is a partner in the Washington, D.C. office of Gibson Dunn, where her practice focuses on investigations, litigation, and counseling on antitrust merger and conduct matters, as well as appellate and civil litigation. Ms. Limarzi previously served as the Chief of the Appellate Section of the U.S. Department of Justice’s Antitrust Division, where she led a team of more than a dozen professionals litigating appeals in the Division’s civil and criminal enforcement actions and participating as amicus curiae in private antitrust actions. While at the Antitrust Division, she litigated appeals of merger challenges in United States v. AT&T and United States v. Anthem. She also advised Division leadership and investigative teams on merger matters involving novel antitrust issues across a variety of industries.

Richard Parker is a partner in the Washington, D.C. office of Gibson Dunn and a member of the firm’s Antitrust and Competition Practice Group. Mr. Parker is a leading antitrust lawyer who has successfully represented clients before both enforcement agencies and the courts. As an experienced antitrust trial and regulatory lawyer, Mr. Parker has been involved in many major antitrust representations, including merger clearance cases, cartel matters, class actions, and government civil investigations. He has extensive experience representing clients in matters before the Federal Trade Commission (FTC) and the U.S. Department of Justice Antitrust Division. His experience in high-profile merger trials has earned him high honors, including being recognized by Chambers USA as a first-tier ranked “Leading Lawyer” in Antitrust, and included on Benchmark Litigation’s “Top 100 Trial Lawyers in America” list.

Mike Raiff is a Gibson Dunn partner in Texas. He has a wide range of litigation experience and has tried numerous cases (jury trials, bench trials, and arbitrations), including helping try the AT&T/Time Warner merger trial in D.C. federal court. In addition to his trial and arbitration practice, Mr. Raiff has argued numerous cases before appellate courts, including Texas appellate courts and several United States Circuit courts. In addition to his antitrust matters, Mr. Raiff has represented clients in various cases involving class actions, shareholder derivative actions, securities fraud, merger and acquisition litigation, contract disputes, environmental disputes, tortious interference claims, infrastructure and public finance disputes, partnership disputes, commercial fraud, and civil conspiracy.

Brian Robison is a partner in Gibson Dunn’s Dallas office. He is a member of the firm’s Antitrust and Competition, Class Actions, and White Collar Defense and Investigations Practice Groups, and he was a member of the team representing Deutsche Telekom in the recent Sprint/T-Mobile merger trial in federal court in New York. Mr. Robison has experience in a wide range of business litigation and antitrust matters in both state and federal courts. He has handled antitrust cases involving claims of monopolization, predatory pricing, price-fixing, supply control, bid rigging, bid rotation, and immunity under the Capper-Volstead Act, the McCarran-Ferguson Act, and the act of state doctrine. He also has counseled clients on the antitrust implications of proposed business transactions, and he has represented clients in civil and criminal antitrust investigations conducted by both state and federal authorities. Mr. Robison has taken both civil and criminal cases to trial, served as a prosecutor for Dallas County, and argued before state courts of appeals. He has been recognized by numerous publications for his work including Chambers USA: America’s Leading Lawyers for Business, The Best Lawyers in America®, and America’s Top 100 High-Stakes Litigators.

Rob Walters is a nationally recognized trial and antitrust lawyer. He has served as lead trial counsel in a wide array of antitrust trials and cases, including as lead trial counsel to AT&T in the DOJ’s 2018 challenge to its $106 billion acquisition of Time Warner, Inc. He also counsels clients in government investigations and the antitrust aspects of mergers and acquisitions. Mr. Walters serves as Partner-in-Charge of the firm’s Dallas office and as a member of the firm’s worldwide Executive Committee. Mr. Walters served as Executive Vice President and General Counsel of Energy Future Holdings, a $60 billion market-cap power, distribution, and energy retail company, from 2008 until 2011. Mr. Walters lectures on the antitrust laws and trial of complex litigation, including as an adjunct professor at Southern Methodist University School of Law in trial advocacy and at the University of Texas School of Law on energy policy and law.

Chris Wilson is Of Counsel in the Washington, D.C. office of Gibson Dunn. He is a member of the firm’s Antitrust and Competition Practice Group. Mr. Wilson assists clients in navigating DOJ, FTC, and international competition authority investigations as well as private party litigation involving complex antitrust and consumer protection issues, including matters implicating the Sherman Act, the Clayton Act, the FTC Act, the Hart-Scott-Rodino (HSR) merger review process, as well as international and state competition statutes. His experience crosses multiple industries, including health insurance, transportation, telecommunications, technology, energy, agriculture, and biotechnology, and his particular areas of focus include merger enforcement, interlocking directorates, joint ventures, compliance programs, and employee “no-poach” agreements.

On November 12, 2020, President Trump issued Executive Order (“E.O.”) 13959 restricting the ability of U.S. persons to invest in securities of certain “Communist Chinese military companies.”[1] This E.O. alleges that under China’s national strategy of “Military-Civil Fusion,” China “exploits United States investors” to finance the development of its military, intelligence, and security capabilities. While the E.O. is only the latest in a flurry of actions by the Trump administration directed against Beijing, it is the first measure to focus on securities—including investments in securities of dozens of prominent Chinese companies, as well as mutual funds and index funds that hold such companies’ shares. Under the E.O., U.S. persons—including individual and institutional investors, stock exchanges, fund managers, investment advisers, broker-dealers, and insurance companies—will be prohibited from purchasing for value publicly traded securities of certain Chinese companies starting in early January 2021 and, absent a change in policy by the incoming Biden administration, will be incentivized to engage in divestment transactions through November 11, 2021.

The E.O. currently applies to 31 ostensibly civil companies that the United States alleges have ties to the Chinese military. The names of those companies appear on two lists published by the U.S. Department of Defense in June 2020 and August 2020, and reproduced below. The U.S. Department of the Treasury has yet to publish guidance indicating whether the E.O. extends to those companies’ subsidiaries; however, a plain-language reading of the E.O. suggests that it may only apply to subsidiaries (if any) that the U.S. Secretary of the Treasury identifies by name. Among the targeted entities are substantial enterprises such as China Mobile Communications and Hikvision, many of which have shares traded on mainland Chinese, Hong Kong, or U.S. stock exchanges. Additionally, several of the targeted companies were added earlier this year to the U.S. Department of Commerce’s Entity List and are therefore already subject to stringent restrictions on access to U.S.-origin goods, software, and technologies. In that sense, the new E.O. marks an expansion of U.S. pressure on Beijing from targeting suppliers of certain large Chinese firms to constricting their sources of financing, albeit in a relatively narrow manner. According to a leading China-focused research organization, of the 31 companies identified to date, only 13 are publicly traded components of the MSCI China Index and only Hikvision has substantial foreign ownership.[2]

Effective January 11, 2021—sixty days after the E.O. was issued—U.S. persons are prohibited from engaging in “any transaction in publicly traded securities, or any securities that are derivative of, or are designed to provide investment exposure to such securities, of any Communist Chinese military company.” “Transaction” is defined to mean the purchase for value of any publicly traded security and the prohibition applies to shares in such companies, as well as shares held indirectly through popular investment vehicles such as exchange traded funds. The E.O. also permits U.S. persons, until November 11, 2021—one year after the E.O. was issued—to engage in otherwise prohibited transactions in order to divest their existing holdings in any of the named Communist Chinese military companies. Although the E.O.’s narrow definition of prohibited transactions does not appear to require U.S. persons to divest holdings in these companies, the prospect of securities becoming illiquid after November 11, 2021 may lead many U.S. investors to divest their holdings during this time.

In this regard the surgical and staggered imposition of restrictions under the E.O. reflects prior approaches the United States used with Venezuela and Russia and is likely animated by similar concerns. When the United States acted to limit the Maduro regime’s access to finance starting in 2017, it, inter alia, restricted transactions associated with certain Venezuela bonds. But, in order to limit the collateral consequences on innocent parties that held significant numbers of those bonds, the United States allowed the limited divestment of those bonds. In the Russia context, following the Crimea incursion in 2014, the United States imposed sanctions on some of the largest enterprises in the Russian financial and energy sectors. However, due to the exposure of U.S. and allied interests to those enterprises, the United States similarly stopped short of imposing blocking sanctions on any of the targeted entities. As with the new China E.O., Russian “sectoral” sanctions prohibit U.S. persons from engaging in only certain types of financial transactions with identified firms. And, importantly, absent some other prohibition, the earlier Russian sectoral sanctions and the new China E.O. permit U.S. persons to continue engaging in all other lawful dealings with listed entities.

The new E.O. is the latest in a series of U.S. measures calculated to address perceived threats to U.S. national security posed by China’s policy of “Military-Civil Fusion.”[3] Like the U.S. Department of Commerce’s expansion of the Military End User Rule, the new Huawei-specific Direct Product Rule, and the recent spate of Entity List designations, as well as the U.S. Government’s procurement ban on certain technologies from several Chinese companies (including two companies that are subject to the new E.O.), this latest action is designed to curtail American support for Chinese companies that allegedly support the Chinese military. The E.O. also complements outreach by the U.S. State Department in August 2020 urging colleges and universities to divest from Chinese holdings more generally,[4] and President Trump’s Working Group on Financial Markets, which has developed guidance that would require companies to provide American regulators with access to audit work papers to remain listed on U.S. exchanges, access that China had historically refused.[5] White House officials are reportedly prioritizing further action against Beijing during President Trump’s final weeks in office.

While the E.O.’s prohibition will take effect shortly before President-elect Biden is sworn in, the apparent wind-down period for U.S. persons to divest their holdings in the listed Communist Chinese military companies extends nearly a year into the next president’s term. As such, in our assessment, the key date for this new policy is not only January 11, 2021, when the prohibition takes effect, but also nine days later when the new administration assumes power. Because the E.O. is not mandated by statute or any other requirement, once in office President Biden could engage with the E.O. as he sees fit: he could revoke the E.O. outright, narrow its reach through published guidance and the exercise of enforcement discretion, decline to target additional Chinese companies, or allow the E.O. to lapse on November 12, 2021 when the President is required by the International Emergency Economic Powers Act to renew the national emergency determination that allowed for the E.O.

However, even for a Biden administration that will be intent on changing the tone of U.S. foreign policy—including through closer coordination with traditional allies—rescinding or eliminating these and other restrictions on Beijing without receiving any concessions in return could spark bipartisan pushback in the U.S. Congress and potentially in the electorate. Moreover, even if President Biden were to narrow or revoke the new E.O., the measure may nevertheless serve its intended purpose of making U.S. persons (including U.S. financial institutions) less willing to hold securities or other financial instruments of, or do other business with, companies that have been linked to the Chinese military, intelligence, or security services. Furthermore, in light of China’s increasingly robust regulatory responses to U.S. unilateral measures—seen in the Hong Kong national security law, Beijing’s new export control law, and its continued threat of establishing an “unreliable” suppliers list for companies that choose to comply with U.S. regulations and cease certain sales to Chinese companies—we expect that China will also respond to this E.O. How China chooses to react will either reduce tensions between Beijing and Washington or continue to exacerbate the situation by potentially imposing costs on entities that choose to comply with this new measure.

* * *

As of November 12, 2020, the 31 Communist Chinese military companies to which the prohibition will apply are as follows:

- Aviation Industry Corporation of China (AVIC)

- China Aerospace Science and Technology Corporation (CASC)

- China Aerospace Science and Industry Corporation (CASIC)

- China Electronics Technology Group Corporation (CETC)

- China South Industries Group Corporation (CSGC)

- China Shipbuilding Industry Corporation (CSIC)

- China State Shipbuilding Corporation (CSSC)

- China North Industries Group Corporation (Norinco Group)

- Hangzhou Hikvision Digital Technology Co., Ltd. (Hikvision)

- Huawei

- Inspur Group

- Aero Engine Corporation of China

- China Railway Construction Corporation (CRCC)

- CRRC Corp.

- Panda Electronics Group

- Dawning Information Industry Co (Sugon)

- China Mobile Communications Group

- China General Nuclear Power Corp.

- China National Nuclear Corp.

- China Telecommunications Corp.

- China Communications Construction Company (CCCC)

- China Academy of Launch Vehicle Technology (CALT)

- China Spacesat

- China United Network Communications Group Co Ltd

- China Electronics Corporation (CEC)

- China National Chemical Engineering Group Co., Ltd. (CNCEC)

- China National Chemical Corporation (ChemChina)

- Sinochem Group Co Ltd

- China State Construction Group Co., Ltd.

- China Three Gorges Corporation Limited

- China Nuclear Engineering & Construction Corporation (CNECC)

_____________________

[1] Exec. Order No. 13959, 85 Fed. Reg. 73185 (Nov. 12, 2020), https://www.govinfo.gov/content/pkg/FR-2020-11-17/pdf/2020-25459.pdf.

[2] Another Trump Attack on Chinese Stocks, Gavekal Dragonomics (Nov. 13, 2020), https://research.gavekal.com/article/another-trump-attack-chinese-stocks.

[3] The Military-Civil Fusion policy is described in China’s national strategic plan “Made in China 2025,” which was announced by Premier Li Keqiang and his cabinet in May 2015.

[4] Kevin Cirilli & Shelly Banjo, U.S. Warns Colleges to Divest China Stocks on Delisting Risk, Bloomberg Quint (Aug. 19, 2020), https://www.bloombergquint.com/business/state-department-urges-colleges-to-divest-from-chinese-companies.

[5] Press Release, President’s Working Group on Financial Markets Releases Report and Recommendations on Protecting Investors from Significant Risks from Chinese Companies, U.S. Dep’t of Treasury (Aug. 6, 2020), https://home.treasury.gov/news/press-releases/sm1086.

The following Gibson Dunn lawyers assisted in preparing this client update: Judith Alison Lee, Adam Smith, Jose Fernandez, Chris Timura, Stephanie Connor, R.L. Pratt and Scott Toussaint.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding the above developments. Please contact the Gibson Dunn lawyer with whom you usually work, the authors, or any of the following leaders and members of the firm’s International Trade practice group:

United States:

Judith Alison Lee – Co-Chair, International Trade Practice, Washington, D.C. (+1 202-887-3591, [email protected])

Ronald Kirk – Co-Chair, International Trade Practice, Dallas (+1 214-698-3295, [email protected])

Jose W. Fernandez – New York (+1 212-351-2376, [email protected])

Marcellus A. McRae – Los Angeles (+1 213-229-7675, [email protected])

Adam M. Smith – Washington, D.C. (+1 202-887-3547, [email protected])

Stephanie L. Connor – Washington, D.C. (+1 202-955-8586, [email protected])

Christopher T. Timura – Washington, D.C. (+1 202-887-3690, [email protected])

Ben K. Belair – Washington, D.C. (+1 202-887-3743, [email protected])

Courtney M. Brown – Washington, D.C. (+1 202-955-8685, [email protected])

Laura R. Cole – Washington, D.C. (+1 202-887-3787, [email protected])

Jesse Melman – New York (+1 212-351-2683, [email protected])

R.L. Pratt – Washington, D.C. (+1 202-887-3785, [email protected])

Samantha Sewall – Washington, D.C. (+1 202-887-3509, [email protected])

Audi K. Syarief – Washington, D.C. (+1 202-955-8266, [email protected])

Scott R. Toussaint – Washington, D.C. (+1 202-887-3588, [email protected])

Shuo (Josh) Zhang – Washington, D.C. (+1 202-955-8270, [email protected])

Asia and Europe:

Fang Xue – Beijing (+86 10 6502 8687, [email protected])

Qi Yue – Beijing – (+86 10 6502 8534, [email protected])

Joerg Bartz – Singapore – (+65 6507 3635, [email protected])

Peter Alexiadis – Brussels (+32 2 554 72 00, [email protected])

Attila Borsos – Brussels (+32 2 554 72 10, [email protected])

Nicolas Autet – Paris (+33 1 56 43 13 00, [email protected])

Susy Bullock – London (+44 (0)20 7071 4283, [email protected])

Patrick Doris – London (+44 (0)207 071 4276, [email protected])

Sacha Harber-Kelly – London (+44 20 7071 4205, [email protected])

Penny Madden – London (+44 (0)20 7071 4226, [email protected])

Steve Melrose – London (+44 (0)20 7071 4219, [email protected])

Matt Aleksic – London (+44 (0)20 7071 4042, [email protected])

Benno Schwarz – Munich (+49 89 189 33 110, [email protected])

Michael Walther – Munich (+49 89 189 33-180, [email protected])

Richard W. Roeder – Munich (+49 89 189 33-160, [email protected])

© 2020 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Please join our distinguished panelists for a discussion about the U.S. Sentencing Guidelines and how they apply in corporate enforcement actions. They will discuss issues arising in white collar matters and strategies that can impact the calculation of the Sentencing Guidelines fine range, including gain from the offense, corporate recidivism, and cooperation, among other issues. Another area of focus will be how the Guidelines address corporate compliance programs and how organizations can position themselves for maximum credit.

View Slides (PDF)

PANELISTS:

Stephanie L. Brooker is co-chair of Gibson Dunn’s Financial Institutions Practice Group and member of the White Collar Group. She is the former Director of the Enforcement Division at FinCEN, and previously served as the Chief of the Asset Forfeiture and Money Laundering Section in the U.S. Attorney’s Office for the District of Columbia and as a DOJ trial attorney for several years. Ms. Brooker represents multi-national companies and individuals in internal corporate investigations and DOJ, SEC, and other government agency enforcement actions involving, for example, matters involving BSA/AML; sanctions; anti-corruption; securities, tax, and wire fraud; whistleblower complaints; and “me-too” issues. Her practice also includes BSA/AML compliance counseling and due diligence and significant criminal and civil asset forfeiture matters. Ms. Brooker has been named a Global Investigations Review “Top 100 Women in Investigations” and National Law Journal White Collar Trailblazer.

David Debold is a partner in the Washington D.C. office, where he practices in the Litigation Department, and is a member of the firm’s White Collar Defense and Investigations Practice Groups. Mr. Debold’s white collar and regulatory matters include: major SEC enforcement actions and investigations involving accounting irregularities, investigations and regulatory actions by FINRA and the PCAOB; and federal criminal investigations and prosecutions involving a number of federal offenses in the environmental, tax, mortgage loan fraud, securities fraud, stock options backdating, money laundering, and antitrust areas.

Michael S. Diamant is a partner in the Washington, D.C. office and a member of the firm’s White Collar Defense and Investigations Practice Group. He also serves on the firm’s Finance Committee. His practice focuses on white collar criminal defense, internal investigations, and corporate compliance. Mr. Diamant has broad white collar defense experience representing corporations and corporate executives facing criminal and regulatory charges. He has represented clients in an array of matters, including accounting and securities fraud, antitrust violations, and environmental crimes, before law enforcement and regulators, like the U.S. Department of Justice and the Securities and Exchange Commission. Mr. Diamant also regularly advises major corporations on the structure and effectiveness of their compliance programs.

Patrick F. Stokes is a partner in the Washington, D.C. office, where his practice focuses on internal corporate investigations and enforcement actions regarding corruption, securities fraud, and financial institutions fraud. Prior to joining the firm, Mr. Stokes headed the DOJ’s FCPA Unit, managing the FCPA enforcement program and all criminal FCPA matters throughout the United States covering every significant business sector. Previously, he served as Co-Chief of the DOJ’s Securities and Financial Fraud Unit.

Christopher W.H. Sullivan is of counsel in the Washington D.C. office and a member of the White Collar Defense and Investigations Practice Group. Mr. Sullivan has significant experience representing clients in government investigations and compliance monitorships. He has represented clients in a variety of areas, including False Claims Act, Foreign Corrupt Practices Act, and OFAC matters, before the Department of Justice, Securities and Exchange Commission, and other enforcement authorities.

Many UK regulated firms will be currently (re-)assessing staff as fit and proper and training staff on the FCA’s (or the PRA’s) Conduct Rules. The FCA has recently banned three individuals from working in the financial services industry for non-financial misconduct outside the workplace. The enforcement actions are, therefore, a timely reminder for regulated firms that the FCA has indicated it will bring an increased focus on how firms deal with non-financial misconduct by employees, both within and outside of the workplace.

Although these three specific cases followed criminal prosecutions for serious sexual offences, regulated firms are faced with particular challenges in determining how to deal with staff issues where the activities are not of the same degree of seriousness, take place outside of the workplace and are unconnected to any regulated activity undertaken by an individual.

Firms should consider what types of employee behaviour within and outside the workplace might be considered non-financial misconduct rendering an individual no longer “fit and proper” or alternatively constitute a breach of the FCA’s (or PRA’s) Conduct Rules reportable to the relevant regulator. Firms would be advised to appropriately document this assessment and consider how this is communicated to staff.

What enforcement action has the FCA taken ?

These individuals committed the offences whilst they were FCA approved persons. The FCA found that all three were not fit and proper and lacked the necessary integrity and reputation required to work in the regulated financial services sector. |

What are the FCA’s expectations as to how firms address non-financial misconduct?

In response to the recent Final Notices, Mark Steward, FCA Executive Director of Enforcement and Market Oversight, stated that: “The FCA expects high standards of character, probity and fitness and properness from those who operate in the financial services industry and will take action to ensure these standards are maintained.”[4] This indicates that the regulatory direction of travel is an increased focus on how firms address instances of non-financial misconduct. This is supported by other important FCA announcements on this topic.

In September 2018, Megan Butler, FCA Executive Director sent a letter to House of Commons’ Women and Equalities Committee.[5] The letter addressed the important issue of sexual harassment and noted that the FCA regarded it as misconduct that falls within the scope of the FCA’s regulatory framework. Tolerance of this sort of misconduct would be a clear example of a driver of poor culture. Megan Butler noted that sexual harassment and other forms of non-financial misconduct can amount to a breach of the FCA’s Conduct Rules and the Senior Managers and Certification Regime (“SMCR”) imposes requirements on firms to notify the FCA of Conduct Rule breaches. The letter was followed by a speech in December 2018 by Christopher Woolard, FCA Executive Director of Strategy and Competition.[6] Mr Woolard noted that “the way firms handle non-financial misconduct, including allegations of sexual misconduct, is potentially relevant to our assessment of that firm, in the same way that their handling of insider dealing, market manipulation or any other misconduct is.”

In January 2020 a “Dear CEO” letter[7] from Jonathan Davidson, FCA Executive Director of Supervision, Retail and Authorisations, was published regarding non-financial misconduct. Although the letter was addressed to the wholesale general insurance sector, it is indicative of the FCA’s approach to non-financial misconduct across the regulated sector. In particular, Mr Davidson noted that non-financial misconduct and an unhealthy culture is a key root cause of harm. How a firm handles non-financial misconduct throughout the organisation, including discrimination, harassment, victimisation and bullying, is regarded as being indicative of a firm’s culture. The FCA expects firms, and senior managers to embed healthy cultures by identifying and modifying the key drivers of their culture. Mr Davidson highlighted that the FCA’s Approach to Supervision document flags the 4 key drivers of culture. These drivers are: leadership; purpose; approach to rewarding and managing people; and governance, systems and controls.

What challenges do firms face relating to non-financial misconduct?

Where the actions of individuals result in convictions and custodial sentences the decision on the fit and proper test is often (but not always) straightforward and the enforcement actions above, together with the various FCA pronouncements also identified, make clear the FCA’s view in this area.

However, regulated firms can be faced with a number of challenges when assessing non-financial misconduct, particularly when it occurs outside of the workplace.

(1) Identifying non-financial misconduct

It is often difficult for firms to identify non-financial misconduct, particularly if it occurs outside of the office. This may be a result of employees incorrectly understanding a firm’s policies and procedures around what must be brought to the firm’s attention or a reluctance of staff to reveal such matters to the firm.

Firms are expected to be able to demonstrate to the FCA that they have that the right processes in place to handle and escalate such cases appropriately. At a time when many employees are working from home the challenge for firms is greater. Firms should ensure that:

- staff are trained and have an understanding of their obligations to inform the firm of relevant matters;

- guidance for staff is clear on the types of matters about which firms would expect to be notified; and

- such guidance should include examples of non-financial misconduct, and the guidance and training should be appropriately documented.

(2) Determining which matters need (immediate) escalation to the FCA

Principle 11 of the FCA’s Principles for Business requires a firm to maintain an open and cooperative relationship with regulators, as well as disclosing appropriately anything relating to the firm of which the FCA would reasonably expect to be notified. Senior Managers are also subject to a Senior Manager Conduct Rule and must disclose appropriately any information of which the FCA or PRA would reasonably expect notice.

Not all instances of misconduct would, however, require an immediate notification – firms will have a challenge in determining whether a matter is sufficiently material to warrant disclosure to a regulator. Factors to consider include:

- seniority or significance of the individual to the firm; and

- seriousness of conduct, potentially as represented by outcome.

(3) Undertaking “fit and proper” assessments

The recent enforcement actions all involved an assessment of the individual concerned under the FCA’s Fit and Proper Test for Employees and Senior Personnel. The most important considerations when assessing the fitness and propriety of a person are the person’s: (1) honesty, integrity and reputation; (2) competence and capability; and (3) financial soundness. Conviction for a serious sexual offence will clearly cause an individual to fail the test. The challenge for firms comes when the scenario is less clear cut. The concepts of “honesty” and “integrity” are inherently subjective and result in a regulated firm often having to make a difficult judgement in a given scenario.

(4) Interplay with the SMCR

The introduction of the SMCR marked a regulatory shift from collective responsibility to individual accountability. For staff subject to the FCA’s Conduct Rules, in addition to the fit and proper test, firms must also make an assessment as to whether any misconduct constitutes a breach of the Conduct Rules. The Conduct Rules are drafted to cover the activities of in-scope staff in both the regulated and unregulated parts of a business. The difficultly arises for firms in assessing when non-financial misconduct, particularly outside of the workplace, also amounts to a breach of the Conduct Rules.

This is important as firms are required to report any disciplinary action taken against an individual for a breach of the Conduct Rules. Firms are also required to include Conduct Rule breaches in regulatory references from new employers once staff have left the firm. It is, therefore, important that firms have a robust process in place for determining what types of employee behaviour within and outside the workplace might be considered a breach of the Conduct Rules and that all such decisions are clearly documented.

What practical steps can firms take to meet regulatory expectations?

It is clear that there is increasing regulatory focus on how regulated firms deal with non-financial misconduct and that failure to tackle such issues appropriately can be taken by the FCA as an indicator of poor culture. Firms would be advised to undertake an assessment as to how they in practice deal, or would deal, with instances of non-financial misconduct by staff.

The following practical steps are examples of matters that firms should consider to ensure that they meet regulatory expectations in this area.

- Fitness and propriety assessments of incoming and existing staff should consider a broad spectrum of indicators, including data around financial and non-financial conduct, inside and outside the workplace.

- Firms should proactively consider the types of non-financial misconduct that would trigger a fitness and propriety re-assessment and, as applicable, a review of whether a Conduct Rule has been breached.

- Appropriate escalation procedures, including whistleblowing, should be in place so that the firm can identify and appropriately investigate allegations of non-financial misconduct by employees both within and outside of the workplace.

- Staff must be appropriately trained on the importance of their behaviour within and outside of the workplace and when matters should be raised and to whom. Firms should also consider whether those to whom such matters may be raised also require training in handling what may be sensitive personal matters.

- Non-financial, as well as financial, metrics should be included in performance assessments.

- Sufficient management information regarding non-financial misconduct should be presented to management for management to receive a complete picture of risk, performance and conduct in the areas for which they are responsible.

_______________________

[1] https://www.fca.org.uk/publication/final-notices/russell-david-jameson-2020.pdf

[2] https://www.fca.org.uk/publication/final-notices/mark-horsey-2020.pdf

[3] https://www.fca.org.uk/publication/final-notices/frank-cochran-2020.pdf

[4] https://www.fca.org.uk/news/press-releases/fca-bans-three-individuals-working-financial-services-industry-non-financial-misconduct

[5] https://www.fca.org.uk/publication/correspondence/wec-letter.pdf

[6] https://www.fca.org.uk/news/speeches/opening-and-speaking-out-diversity-financial-services-and-challenge-to-be-met

[7] https://www.fca.org.uk/publication/correspondence/dear-ceo-letter-non-financial-misconduct-wholesale-general-insurance-firms.pdf

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work in the firm’s Financial Institutions practice group, or the following authors in London:

Matthew Nunan (+44 (0) 20 7071 4201, [email protected])

Martin Coombes (+44 (0) 20 7071 4258, [email protected])

© 2020 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Our distinguished panelists discuss the challenging interplay between internal audit and white collar investigations. We discuss strategies to ensure that internal audit complements the compliance function and how best to deal with legal problems identified by internal audit activities. Our panelists will go over recent FCPA enforcement actions that leverage internal audit findings to support alleged violations.