Four Years of Evolving Form 10-K Human Capital Disclosures

Client Alert | December 16, 2024

A Survey of Disclosures from the S&P 100 During the Four Years Following Adoption of the Securities and Exchange Commission Rule.

Human capital resource disclosures by public companies have continued to be a focus since the U.S. Securities and Exchange Commission (the “Commission”) adopted the new rules in 2020, not only for companies making the disclosures, but employees, investors, and other stakeholders reading them. This alert updates the alert we issued in November 2023, “Form 10-K Human Capital Disclosures Continue to Evolve,” available here, and reviews disclosure trends among S&P 100 companies categorized into 28 topic areas. Each of these companies has now included human capital disclosure in their past four annual reports on Form 10-K. This alert also provides practical considerations for companies as we head into 2025.

Overall, our findings indicate that companies are generally making only minor changes to their disclosures year over year, and these minor changes generally included shortening of company disclosures, maintaining or decreasing the number of topics covered, and including slightly less quantitative information in some areas.[1] Specifically, we identified the following trends regarding the S&P 100 companies’ human capital disclosures compared to the previous year:

- Length of disclosure. Fifty-seven percent of surveyed companies decreased the length of their disclosures, 34% increased the length of their disclosures, and the length of the remaining 9% remained the same.

- Number of topics covered. Forty-one percent of surveyed companies decreased the number of topics covered, 13% increased the number of topics covered, and the remaining 46% covered the same number of topics.

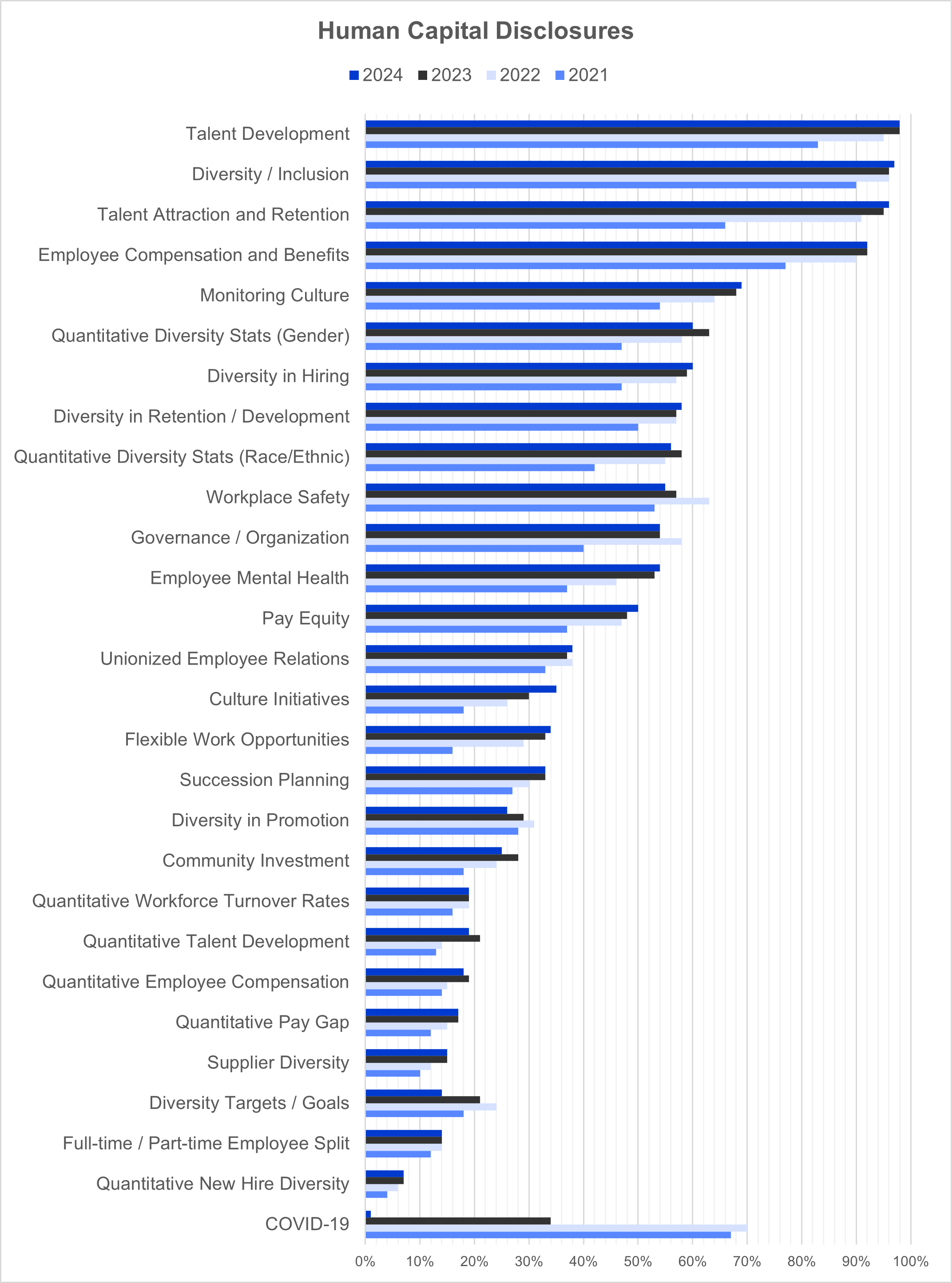

- Breadth of topics covered. Across all companies, the prevalence of 10 topics increased, nine topics decreased, and nine topics remained the same.

- The most significant year-over-year increases in frequency involved Culture Initiatives (30% to 35%) and Pay Equity (48% to 50%) disclosures.

- The most significant year-over-year decrease involved COVID-19 disclosures, which declined in frequency from 34% to 1%. Other year-over-year decreases related to disclosures addressing Diversity Targets and Goals (21% to 14%), Diversity in Promotion (29% to 26%), Quantitative Diversity Statistics regarding Gender (63% to 60%), and Community Investment (28% to 25%).

- Most common topics covered. This year, the topics most commonly discussed generally remained consistent with the previous two years. For example, Talent Development, Diversity and Inclusion, Talent Attraction and Retention, Employee Compensation and Benefits, and Monitoring Culture remained the five most frequently discussed topics. The topics least discussed this most recent year, however, changed slightly from that of the previous year as COVID-19 disclosures, and Diversity Targets and Goals dropped into the five least frequently covered topics.

- Industry trends. Within the technology and finance industries, the trends that we saw in the previous year regarding the frequency of topics disclosed generally remained the same.

I. Background on the Requirements

As we previously discussed in our client alert titled “Discussing Human Capital: A Survey of the S&P 500’s Compliance with the New SEC Disclosure Requirement One Year After Adoption,” available here, on August 26, 2020, the Commission voted three-to-two to approve amendments to Items 101, 103, and 105 of Regulation S-K, including the principles-based requirement to discuss a registrant’s human capital resources to the extent material to an understanding of the registrant’s business taken as a whole.[2] Specifically, public companies’ human capital disclosure must include “the number of persons employed by the registrant, and any human capital measures or objectives that the registrant focuses on in managing the business (such as, depending on the nature of the registrant’s business and workforce, measures or objectives that address the development, attraction, and retention of personnel).”

Notably, since 2021 the Commission’s agenda list has included new human capital disclosure rules that were expected to be more prescriptive than the current rules,[3] in part, because one of the main criticisms of the existing human capital rules is lack of comparability across companies. The future of these rules is even less clear now as Chair Gensler who pushed for these rules (along with other rules, such as climate change) announced that he will be leaving the SEC in January 2025 in light of the new incoming administration. In the meantime, as our survey demonstrates, while company human capital disclosures vary—which is expected under the principles-based regime—comparability across the disclosures exists. The next four sections show the relevant data from our survey.[4]

II. Disclosure Topics

Our survey classifies human capital disclosures into 28 topics, each of which is listed in the following chart, along with the number of companies that discussed the topic in each of 2021, 2022, 2023, and 2024. Each topic is described more fully in the sections following the chart.

|

A. Workforce Composition

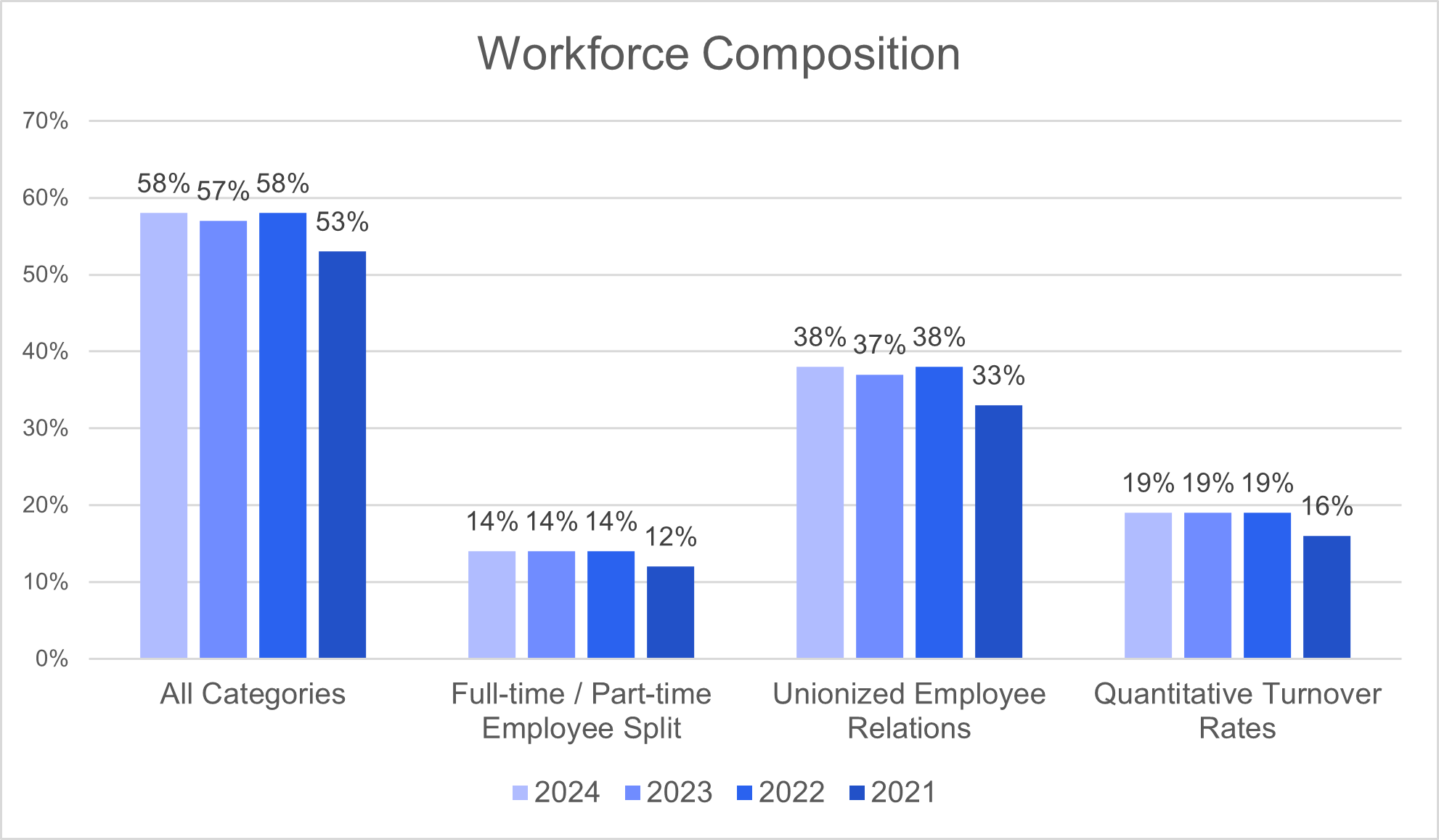

Among S&P 100 companies, 58% included disclosures relating to workforce composition in one or more of the following categories:

- Full-time/part-time employee split. While most companies provided the total number of full-time employees, only 14% of the companies surveyed included a quantitative breakdown of the number of full-time versus part-time employees or salaried versus hourly employees, consistent with the previous two years. Similarly, 66% of companies provided statistics on the number of seasonal employees and/or independent contractors or a breakdown of employees by business segment, job function, or geographical location, the same as the previous year, and up from and 60% in 2021.

- Unionized employee relations. Of the companies surveyed, 38% stated that some portion of their workforce was part of a union, works council, or similar collective bargaining agreement.[5] These disclosures generally included a statement providing the company’s opinion on the quality of labor relations, and in many cases, disclosed the number of unionized employees.

- Quantitative workforce turnover rates. Although a majority of companies discussed employee turnover and the related topics of talent attraction and retention in a qualitative way (as discussed in Section II.B. below), only 19% of companies surveyed provided specific employee turnover rates (whether voluntary or involuntary), consistent with the previous two years.

|

B. Diversity

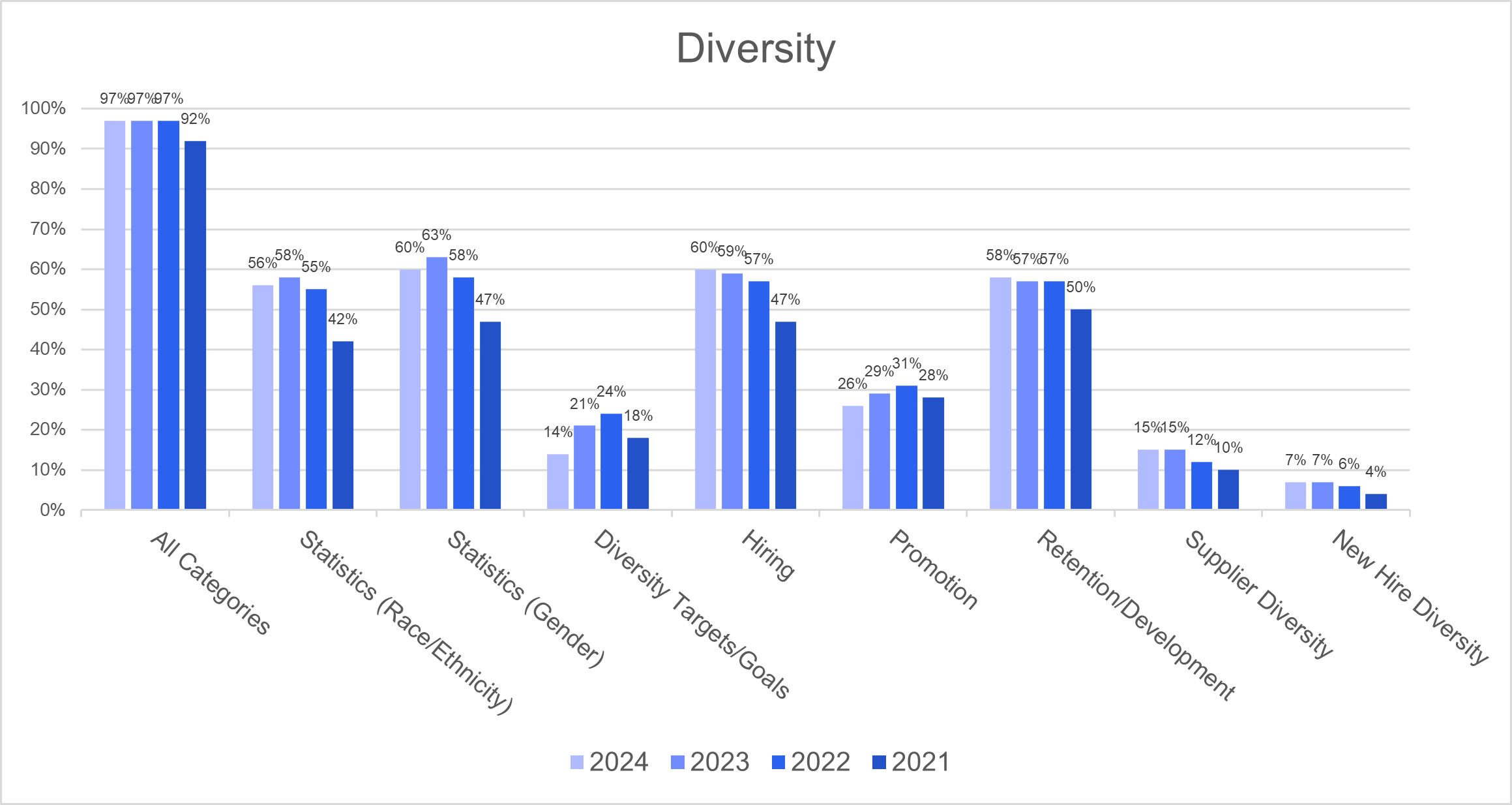

Among S&P 100 companies, 97% included disclosures relating to diversity in one or more of the following categories:

- Diversity and inclusion. This was the most common diversity-related disclosure topic, with 97% of companies including a qualitative discussion regarding the company’s commitment to diversity, equity, and inclusion (“DEI”), consistent with the previous two years and up slightly from 91% in 2021. The depth of these disclosures varied, ranging from generic statements expressing the company’s support of diversity in the workforce to detailed examples of actions taken to recruit and support underrepresented groups and increase the diversity of the company’s workforce.

- Priorities within diversity. Companies disclosed different areas of focus for diversity efforts and programming within the organization. The most common disclosure was diversity in the company’s hiring practices (60% of companies in 2024, up dramatically from 47% in 2021), followed by diversity in the retention or development of the company’s current workforce (58% of companies in 2024, up slightly from 50% in 2021), diversity in the company’s promotion practices (26% of companies in 2024, down from a high of 31% in 2022), and finally diversity in the company’s suppliers (15% of companies in 2024, up slightly from 10% in 2021). A decreasing minority of companies also discussed, in qualitative or quantitative terms, the companies’ commitments to aspirational diversity goals or targets (14% of companies in 2024, down from a high of 24% of companies in 2022), with such decrease likely due to the heightened legal risk associated with DEI programs following the June 2023 United States Supreme Court decision in Students for Fair Admissions v. Harvard.

- Quantitative diversity statistics. Many companies also included a quantitative breakdown of the gender or racial representation of the company’s workforce: 60% included statistics on gender and 56% included statistics on race or ethnicity (down slightly compared to 2023, but up significantly from 47% and 42%, respectively, in 2021). Companies generally provided gender statistics on both a global and U.S. basis, whereas nearly all companies provided race or ethnicity statistics for their U.S. workforce only. Most companies provided these statistics in relation to their workforce generally, regardless of position; however, an increased subset (40% in 2024, compared to 25% in 2021) included separate statistics for different classes of employees (e.g., managerial, vice president and above, etc.). Similarly, 12% of companies also provided separate statistics for their boards of directors (compared to 10% in each of 2023 and 2022 and 4% in 2021). Some companies also included numerical goals for gender or racial representation, either in terms of overall representation, promotions, or hiring—11% of companies included these diversity goals or targets (compared to 15% in 2023, 18% in 2022, and 14% in 2021).

|

C. Recruiting, Training, Succession

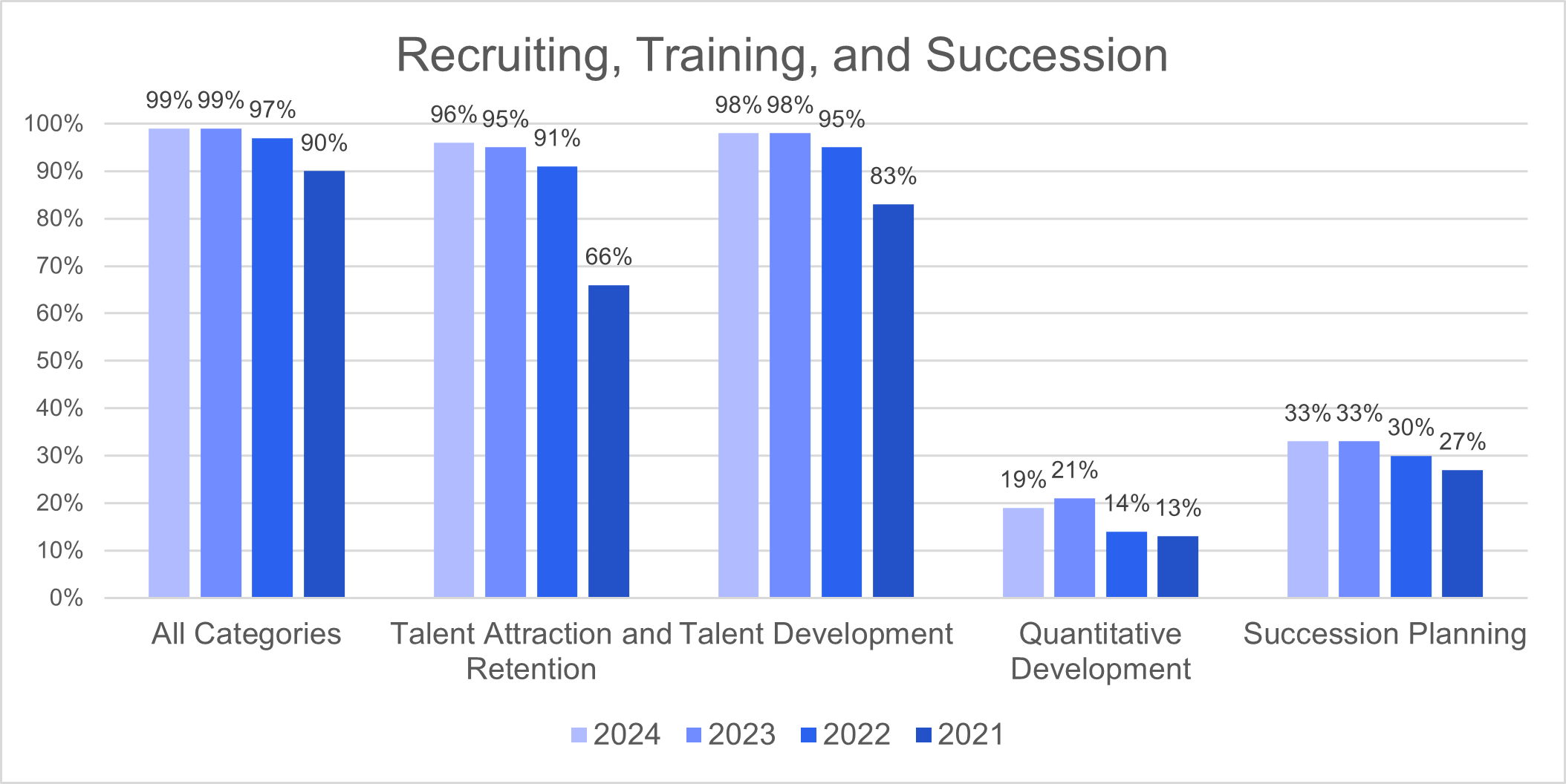

Among S&P 100 companies, 99% included disclosures relating to talent and succession planning in one or more of the following categories:

- Talent attraction and retention. These disclosures were generally qualitative and focused on efforts to recruit and retain qualified individuals. While general statements regarding recruiting and retaining talent were very common, with 96% of companies including this type of disclosure (relatively flat in the prior two years, but up significantly from 66% in 2021), quantitative measures of retention, like workforce turnover rate, were uncommon, with only 19% of companies disclosing such statistics (as noted above).

- Talent development. Disclosures related to talent development were the most common category, with 98% of companies including a qualitative discussion regarding employee training, learning, and development opportunities, up from 83% in 2021. This disclosure tended to focus on the workforce as a whole rather than specifically on senior management. Companies generally discussed training programs such as in-person and online courses, leadership development programs, mentoring opportunities, tuition assistance, and conferences. Some companies discussed quantitative figures related to talent development, such as the number of hours employees spent on learning and development or the company’s investment in development resources, with 19% of companies including this type of disclosure.

- Succession planning. Only 33% of companies surveyed addressed their succession planning efforts, which may be a function of succession being a focus area primarily for executives rather than the human capital resources of a company more broadly. However, this is up from 27% of companies who discussed succession planning in 2021.

|

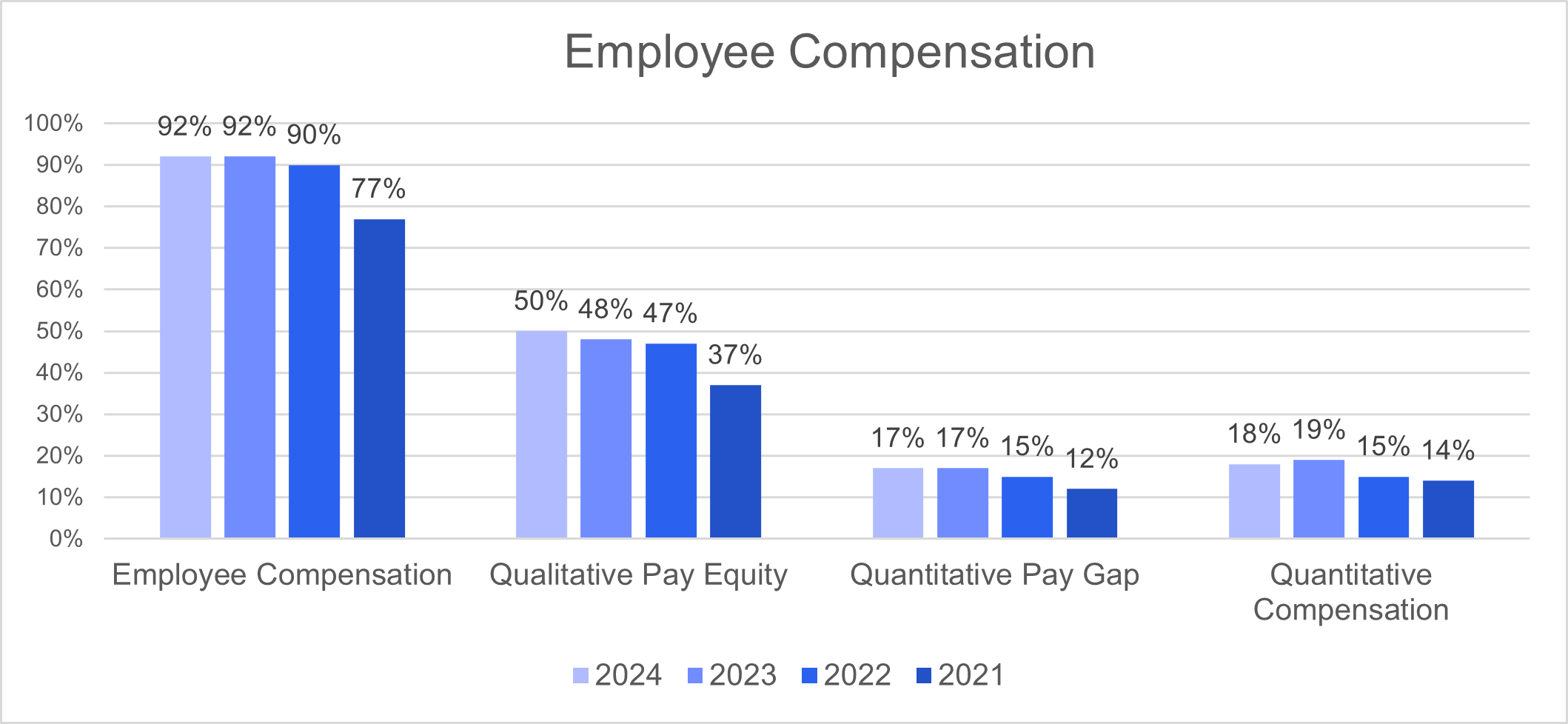

D. Employee Compensation[6]

Among S&P 100 companies, 92% included disclosures relating to employee compensation, up from 77% in 2021. All of those companies included a qualitative description of the compensation and/or benefits program offered to employees, with a small minority providing quantitative measures such as minimum or average wages or investment in benefits (17% of companies surveyed in 2024, up from 12% in 2021). Of the companies surveyed, 50% addressed pay equity practices or assessments (up from 37% in 2021), and substantially fewer companies included quantitative measures of the pay gap between racially or ethnically diverse and nondiverse employees or male and female employees (17% of companies surveyed in 2024, up from 12% in 2021).

|

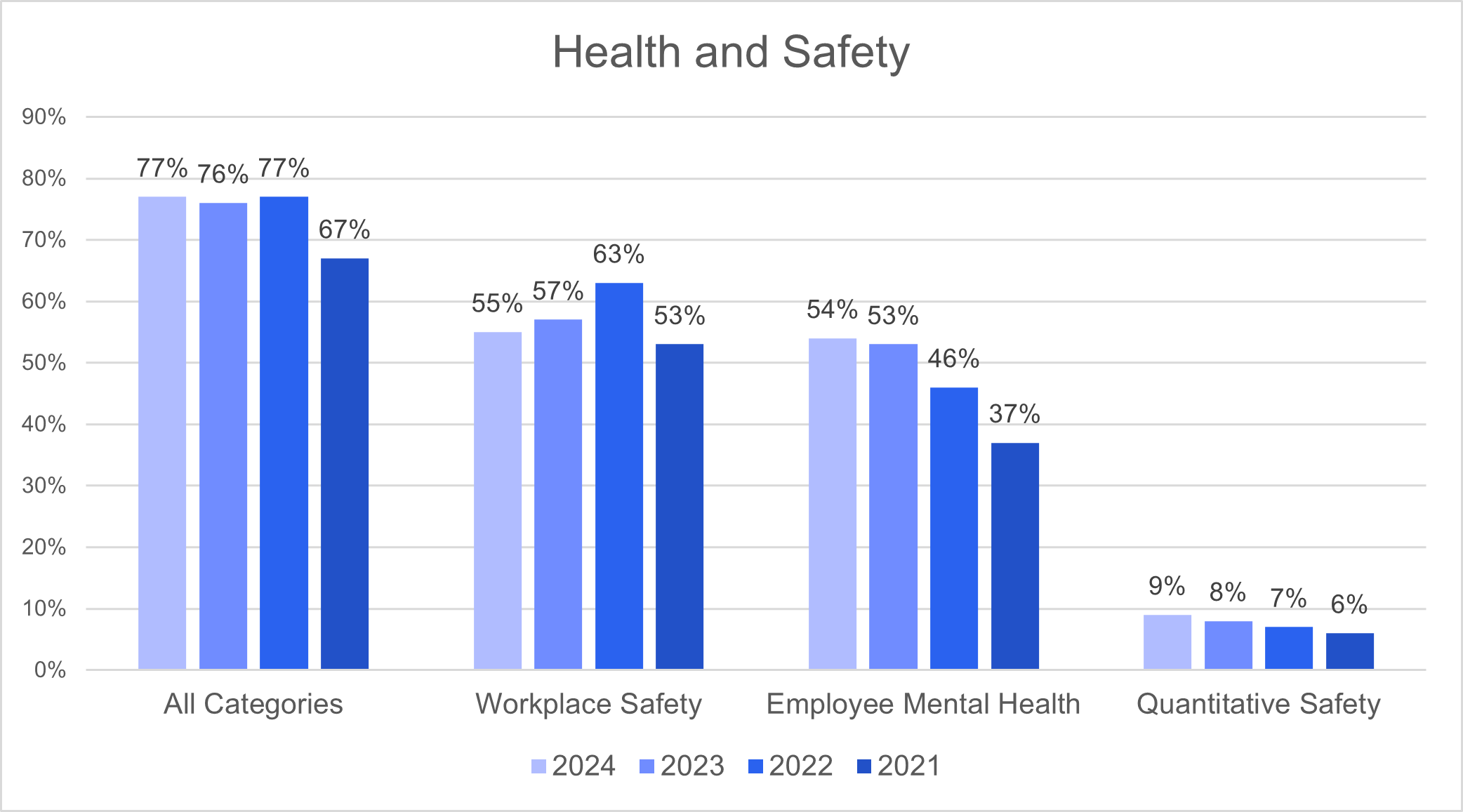

E. Health and Safety

Among S&P 100 companies, 77% included disclosures relating to health and safety in one or both of the following categories:

- Workplace safety. Of the companies surveyed, 55% included qualitative disclosures relating to workplace health and safety, down from 63% in 2022, typically consisting of statements about the company’s commitment to safety in the workplace generally and compliance with applicable regulatory and legal requirements. However, 9% of companies surveyed provided quantitative disclosures in this category, generally focusing on historical and/or target incident or safety rates or investments in safety programs. These quantitative disclosures tended to be more prevalent among industrial, energy, and manufacturing companies.

- Employee mental health. In connection with disclosures about benefits provided to employees, including benefits intended to support employees’ general wellness or wellbeing, 54% of companies disclosed initiatives taken to support employees’ mental or emotional health and wellbeing, up from 37% in 2021.

|

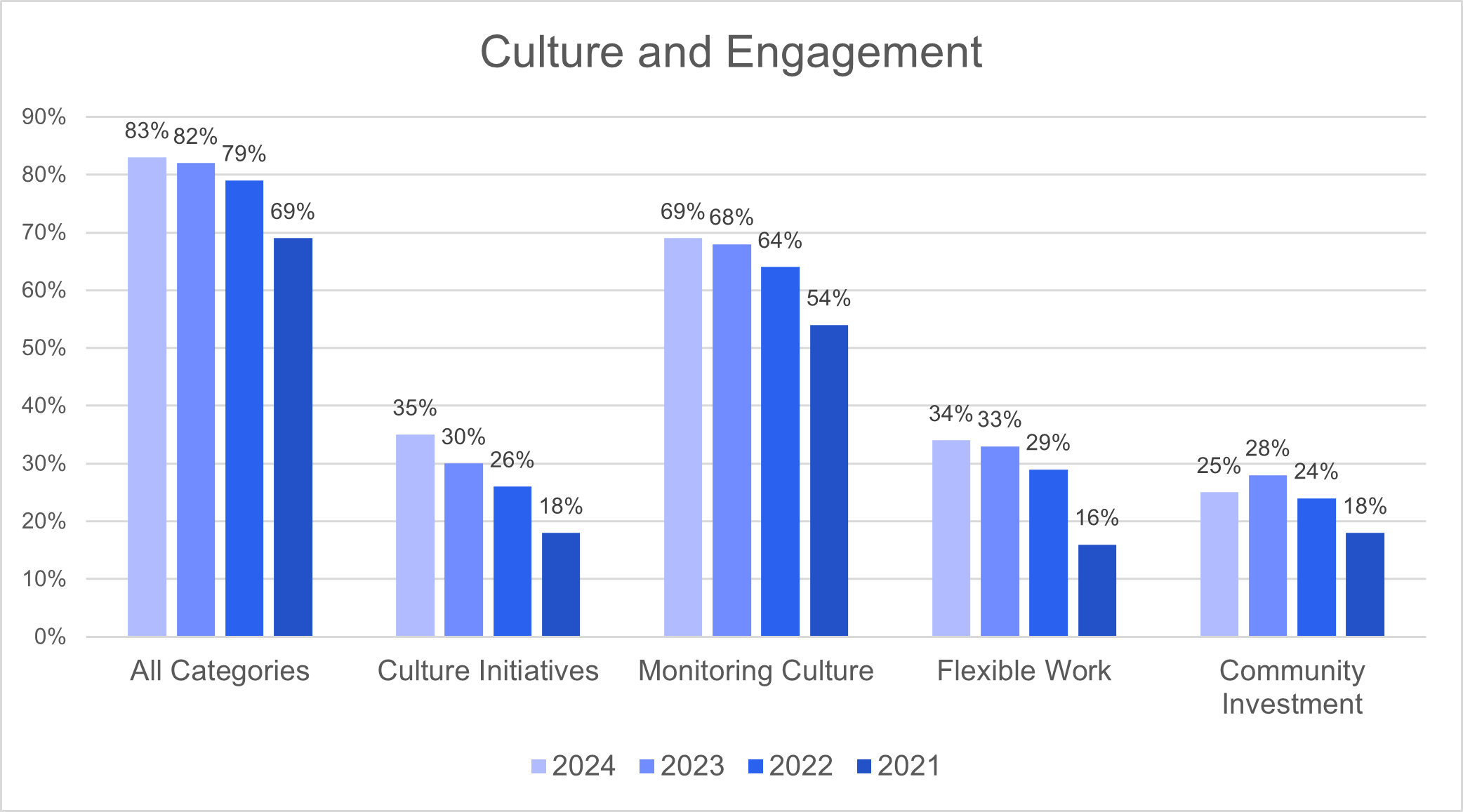

F. Culture and Engagement

In addition to the many instances where companies included general descriptions of their commitment to company culture and values, 83% of S&P 100 companies discussed specific initiatives they were taking related to culture and engagement in one or more of the following categories:

- Culture and engagement initiatives. Specific disclosures relating to practices and initiatives undertaken to build and maintain their culture and values have increased steadily each year, with 35% of the companies surveyed providing such disclosure, up from 18% in 2021. These companies most commonly discussed efforts to communicate with employees (e.g., through town halls, CEO outreach, trainings, or conferences and presentations) and to recognize employee contributions (e.g., awards programs and individualized feedback). Many companies also discussed culture in the context of diversity-related initiatives designed to help foster an inclusive culture.

- Monitoring culture. Of the companies surveyed 69% provided disclosures about the ways that companies monitor culture and employee engagement, up from 54% in 2021. Companies generally disclosed the frequency of employee surveys used to track employee engagement and satisfaction, with some reporting on the results of these surveys, sometimes measured against prior year results or industry benchmarks, and ways in which company management or the board utilized survey results.

- Flexible Work Opportunities. About one-third of S&P 100 companies describe flexible working arrangements, including remote or hybrid work or scheduling adjustments to accommodate different ways of working, with 34% of companies provided such disclosure in 2024, compared to 16% in 2021. Although many of these companies discussed this topic in previous years, past mentions of measures related to flexible work environments were generally in connection with COVID-related safety concerns, whereas recent discussions are increasingly related to talent acquisition and retention.

- Community investment. Some companies disclosed information about community investment, partnerships, donations, or volunteer programs sponsored by the company, with 25% of companies surveyed providing such disclosure in 2024, compared to 28% in 2023 and 18% in 2021. Many companies discussed their community investment efforts as offshoots of or in conjunction with their diversity, equity, and inclusion efforts.

|

G. COVID-19

The number of S&P 100 companies that included information regarding COVID-19 and its impact on company policies and procedures or on employees dropped to only one companies making such disclosure, compared to 34% in 2023 and 70% in 2022. This sharp decline in COVID-19 disclosures is consistent with a more general trend of companies discussing COVID-19 less frequently as a result of its decreasing significance and illustrates the expected evolution of disclosure resulting from a principles-based framework.

H. Human Capital Management Governance and Organizational Practices

Just over half of S&P 100 companies (54% of those surveyed, compared to 40% in 2021) addressed their governance and organizational practices (such as oversight by the board of directors or a committee and the organization of the human resources function).

III. Industry Trends

One of the main rationales underlying the adoption of principles-based—rather than prescriptive—requirements for human capital disclosures is that the relative significance of various human capital measures and objectives varies by industry. This is reflected in the following industry trends that we observed:[7]

- Technology Industries (E-Commerce, Internet Media & Services, Hardware, Software & IT Services, and Semiconductors). For the 22 companies in the Technology Industries, at least 63% discussed each of talent development and training opportunities, talent attraction, recruitment and retention, employee compensation, employee mental health, and diversity. Compared to the S&P 100 as a whole, relatively uncommon disclosures among this group included part-time and full-time employee statistics (5%), succession planning (9%), supplier diversity (5%), diversity in retention and development (41%), quantitative diversity statistics regarding race/ethnicity and gender (41% and 45%, respectively), and unionized employee relations (18%). However, these industries continued to see increased rates of disclosure compared to the S&P 100 for quantitative turnover rates (41%), flexible work opportunities (45%), culture initiatives (45%), and qualitative pay equity (59%).

- Finance Industries (Asset Management & Custody Activities, Consumer Finance, Commercial Banks, and Investment Banking & Brokerage). For the 13 companies in the Finance Industries, a large majority continued to include quantitative diversity statistics regarding race (85%) and gender (92%) (matching that of the last two years) and qualitative disclosures regarding employee compensation (92%), and, compared to other industries, a relatively higher number discussed diversity in hiring (85%), employee mental health (77%), flexible work opportunities (69%), pay equity (69%), and quantified their pay gap (46%). Relatively uncommon disclosures among this group included part-time and full-time employee statistics, unionized employee relations, quantitative workforce turnover rates, diversity targets and goals, quantitative new hire diversity, supplier diversity, and workplace safety (in each case less than 16%).

- Pharmaceutical Industries (Biotechnology & Pharmaceuticals). For the eight companies in the Pharmaceutical Industries, at least 87% discussed each of diversity, workplace safety, monitoring culture, talent attraction and retention, talent development, and employee compensation. Compared to the S&P 100 as a whole, relatively uncommon disclosures among this group included succession planning (13%), quantitative pay gap (0%), and diversity targets and goals (0%). However, these industries continued to see increased rates of disclosure compared to the S&P 100 for supplier diversity (38%), workplace safety (88%), culture initiatives (50%), and flexible work opportunities (75%).

IV. Disclosure Format

The format of human capital disclosures in S&P 100 companies’ annual reports on Form 10‑K continued to vary greatly.

Word Count. The length of the disclosures ranged from 106 to 1,809 words, with the following statistical trends in the past four years:

| 2024 | 2023 | 2022 | 2021 | |

| Minimum word count | 106 | 106 | 109 | 105 |

| Maximum word count | 1,809 | 2,094 | 1,995 | 1,931 |

| Median | 913 | 1,035 | 959 | 818 |

| Mean | 946 | 1,002 | 976 | 825 |

Metrics. The disclosure requirement specifically asks for a description of “any human capital measures or objectives that the registrant focuses on in managing the business” (emphasis added). Our survey revealed that companies are increasingly providing quantitative metrics, with 84% of companies providing disclosure in at least one of the quantitative categories we discuss above (compared to 87% in 2023, 80% in 2022, and 67% in 2021) and only 8% electing not to include any type of quantitative metrics beyond headcount numbers (compared to 7% in 2023, 10% in 2022 and 14% in 2021).

Graphics. Although the minority practice, 26% of companies surveyed also included tables, charts, graphics or similar formatting used to draw attention to particular elements, compared to 26% in 2023, 24% in 2022 21% in 2021, which were generally used to present statistical data, such as diversity statistics or breakdowns of the number of employees by geographic location.

Categories. Most companies organized their disclosures by categories similar to those discussed above and included headings to define the types of disclosures presented.

V. Upcoming Rulemaking and Investor Advisory Committee Recommendations

At its meeting on September 21, 2023, the Commission’s Investor Advisory Committee (“IAC”) approved subcommittee recommendations (the “IAC Recommendations”) to expand required human capital management disclosures.[8] The IAC Recommendations contain prescriptive disclosure requirements—many of which have been previously considered as part of the 2020 rulemaking—for various quantitative metrics in the business description of Form 10-K under Item 101(c) of Regulation S-K (including headcount, turnover, compensation, and demographic data) as well as narrative disclosure in Management Discussion and Analysis. For details regarding the IAC Recommendations, please refer to “Form 10-K Human Capital Disclosures Continue to Evolve,” available here.

According to the most recent Regulatory Flexibility agenda, a human capital management rule proposal that was originally slated for October 2021 was expected to be issued in October 2024.[9] However, no rule was ever proposed, and many expect regulatory priorities to change with the upcoming shift in the administration, including SEC Chair Gary Gensler’s upcoming departure on January 20, 2025. We therefore do not expect that the Commission will be adopting IAC’s recommendations in the near term as Republican commissions have in the past generally favored principles-based disclosure over prescriptive disclosure requirements.

VI. Comment Letter Correspondence

Comment letter correspondence from the staff of the Division of Corporation Finance (the “Staff”), which often helps put a finer point on principles-based disclosure requirements like this one, has shed relatively little light on how the Staff believes the new requirements should be interpreted. Consistent with what we found at this time in the prior three years, the comment letters, all of which involved reviews of registration statements, were generally issued to companies whose disclosures about employees were limited to the bare-bones items companies have discussed historically, such as the number of persons employed and the quality of employee relations. From these companies, the Staff simply sought a more detailed discussion of the company’s human capital resources, including any human capital measures or objectives upon which the company focuses in managing its business. There were also a few comment letters where the Staff asked companies to clarify statements in their human capital disclosures or expand their human capital disclosures based on related risks identified in their risk factors.[10] Based on our review of the responses to those comment letters, we have not seen a company take the position that a discussion of human capital resources was immaterial and therefore unnecessary.

VIII. Conclusion

Based on our survey, companies continue to be thoughtful about their human capital disclosures—expanding their disclosures in some areas (e.g., culture initiatives and pay equity) and reducing them in others (e.g., COVID-19, diversity targets and goals, diversity in promotion, and community investment)—in response to ever-changing circumstances. That is precisely what principles-based disclosure rules are designed to elicit.

To that end, as companies prepare for the upcoming Form 10-K reporting season, they should consider the following:

- Confirm (or reconfirm) that the company’s disclosure controls and procedures support the statements made in human capital disclosures knowing that controls in the HR department may not be as rigorous as accounting controls. These disclosures create legal liability risks and should be treated accordingly.

- Companies may want to compare their own disclosures against what their industry peers did these past four years, including specifically any notable changes to disclosures made in the past year.

- Remind stakeholders internally that these disclosures likely will continue to evolve. This is especially true with the change in administration that could result in companies focusing on fewer or different issues. The types of measures and objectives that a company focuses on in managing its business and that are material to each company may also change in response to current events, as was shown by essentially the complete removal of COVID-19 related disclosures from 10-K filings the past two years and the decrease in disclosures relating to diversity targets and goals over the same period.

- If you continue to disclose targets, expect the SEC staff to ask you to disclose the progress that management has made. You may wish to reconsider the utility in disclosing specific targets.

- Addressing in the upcoming disclosure, if not already disclosed, the progress that management has made with respect to any significant objectives it has set regarding its human capital resources as investors are likely to focus on year-over-year changes and the company’s performance versus stated goals.

- Addressing significant areas of focus highlighted in engagement meetings with investors and other stakeholders. In a 2024 survey, human capital management was one of the top five issues (aside from financial performance) most important to investors when evaluating companies.[11]

- Revalidating the methodology for calculating quantitative metrics and assessing consistency with the prior year. Former Chairman Clayton commented that he would expect companies to “maintain metric definitions constant from period to period or to disclose prominently any changes to the metrics.”

[1] Data provided is as of November 10, 2024 and is based on the companies currently included within the S&P 500, so some statistics are slightly different than they were in the prior surveys. The categorization data necessarily involves subjective assessment and should be considered approximate.

[2] See 17 C.F.R. § 229.101(c)(2)(ii).

[3] Agency Rule List – Spring 2024 Securities and Exchange Commission, Office of Information and Regulatory Affairs (2024), available here.

[4] Note that companies often include additional human capital management-related disclosures in their ESG/sustainability/social responsibility reports, on their websites, and in their proxy statements, but these disclosures are outside the scope of the survey, which is focused on disclosures included in Part I, Item 1 of annual reports on Form 10-K.

[5] While never expressly required by Regulation S-K, as a result of disclosure review comments issued by the Division of Corporation Finance over the years and a decades-old and since-deleted requirement in Form 1-A, it has been a relatively common practice to discuss collective bargaining and employee relations in the Form 10-K or in an IPO Form S-1, particularly since the threat of a workforce strike could be material.

[6] Our survey reviewed the employee compensation disclosures contained in Part I, Item 1 of each company’s Form 10-K and did not separately review any employee compensation information included in companies’ financial statements or the notes thereto.

[7] For purposes of our survey, we grouped companies in similar industries based on both their four-digit Standard Industrial Classification code and their designated industry within the Sustainable Industry Classification System. The industry groups discussed in this section cover 43% of the companies included in our survey.

[8] Available at https://www.sec.gov/files/spotlight/iac/20230921-recommendation-regarding-hcm.pdf.

[9] Agency Rule List – Spring 2024 Securities and Exchange Commission, Office of Information and Regulatory Affairs (2024), available here.

[10] See, e.g., comments issued to Concentra Group Holdings Parent, Inc. (available at https://www.sec.gov/Archives/edgar/data/2014596/000000000024003738/filename1.pdf) and PACS Group, Inc. (available at https://www.sec.gov/Archives/edgar/data/2001184/000000000024000134/filename1.pdf).

[11] See PwC’s Global Investor Survey 2024, available at https://www.pwc.com/gx/en/issues/c-suite-insights/global-investor-survey.html.

Gibson Dunn’s lawyers are available to assist with any questions you may have regarding these developments. To learn more about these issues, please contact the Gibson Dunn lawyer with whom you usually work in the firm’s Securities Regulation and Corporate Governance or Labor and Employment practice groups, or any of the following practice leaders and members:

Securities Regulation and Corporate Governance:

Elizabeth Ising – Co-Chair, Washington, D.C. (+1 202.955.8287, eising@gibsondunn.com)

James J. Moloney – Co-Chair, Orange County (+1 949.451.4343, jmoloney@gibsondunn.com)

Lori Zyskowski – Co-Chair, New York (+1 212.351.2309, lzyskowski@gibsondunn.com)

Aaron Briggs – San Francisco (+1 415.393.8297, abriggs@gibsondunn.com)

Thomas J. Kim – Washington, D.C. (+1 202.887.3550, tkim@gibsondunn.com)

Brian J. Lane – Washington, D.C. (+1 202.887.3646, blane@gibsondunn.com)

Julia Lapitskaya – New York (+1 212.351.2354, jlapitskaya@gibsondunn.com)

Ronald O. Mueller – Washington, D.C. (+1 202.955.8671, rmueller@gibsondunn.com)

Michael Scanlon – Washington, D.C.(+1 202.887.3668, mscanlon@gibsondunn.com)

Michael A. Titera – Orange County (+1 949.451.4365, mtitera@gibsondunn.com)

Labor and Employment:

Jason C. Schwartz – Co-Chair, Washington, D.C. (+1 202.955.8242, jschwartz@gibsondunn.com)

Katherine V.A. Smith – Co-Chair, Los Angeles (+1 213.229.7107, ksmith@gibsondunn.com)

© 2024 Gibson, Dunn & Crutcher LLP. All rights reserved. For contact and other information, please visit us at www.gibsondunn.com.

Attorney Advertising: These materials were prepared for general informational purposes only based on information available at the time of publication and are not intended as, do not constitute, and should not be relied upon as, legal advice or a legal opinion on any specific facts or circumstances. Gibson Dunn (and its affiliates, attorneys, and employees) shall not have any liability in connection with any use of these materials. The sharing of these materials does not establish an attorney-client relationship with the recipient and should not be relied upon as an alternative for advice from qualified counsel. Please note that facts and circumstances may vary, and prior results do not guarantee a similar outcome.